If you own a free standing home in Cliftleigh, NSW 2321, you're likely curious about whether your home insurance premium stacks up against what your neighbours are paying — and what the rest of the country looks like. In this article, we break down a real home and contents insurance quote for a four-bedroom, two-bathroom brick veneer home in Cliftleigh, compare it against suburb, state, and national benchmarks, and share practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $970 per year (or roughly $94 per month) for combined home and contents insurance, covering a building sum insured of $557,000 and contents valued at $50,000. The building excess is $3,000 and the contents excess is $1,000.

Our price rating for this quote is FAIR — Around Average.

So what does that actually mean? Based on data collected from quotes in the Cliftleigh area, the suburb average sits at $1,215 per year, with a median of $1,117. This quote lands just above the 25th percentile ($965), meaning it's more affordable than roughly 75% of quotes seen in the suburb. That's a genuinely competitive result — not rock-bottom, but meaningfully below the local average.

For a relatively new home built in 2021 with standard fittings, this pricing makes sense. Newer builds tend to attract lower premiums because modern construction standards reduce the likelihood of structural claims, and insurers price that reduced risk accordingly.

---

How Cliftleigh Compares

To put this quote in broader context, it helps to zoom out and look at what homeowners are paying across New South Wales and nationally.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Cliftleigh (suburb) | $1,215/yr | $1,117/yr |

| Port Stephens LGA | $3,116/yr | — |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

(Note: State and national averages are heavily influenced by high-risk coastal, flood, and cyclone-prone areas, which skews averages significantly above medians.)

At first glance, the NSW state average of $9,528 looks alarming — but that figure is dragged upward by properties in high-risk zones across the state. The NSW median of $3,770 is a more grounded comparison point, and even against that benchmark, the $970 quote for this Cliftleigh property looks very competitive.

Compared to the broader Port Stephens LGA average of $3,116, this quote is substantially lower, suggesting that Cliftleigh specifically benefits from relatively favourable risk conditions within the local government area.

You can explore local pricing trends in more detail on the Cliftleigh suburb stats page, or compare how NSW tracks against other states on the NSW insurance stats page. For a full national picture, visit the national home insurance stats page.

---

Property Features That Affect Your Premium

Several characteristics of this particular home work in the owner's favour when it comes to pricing:

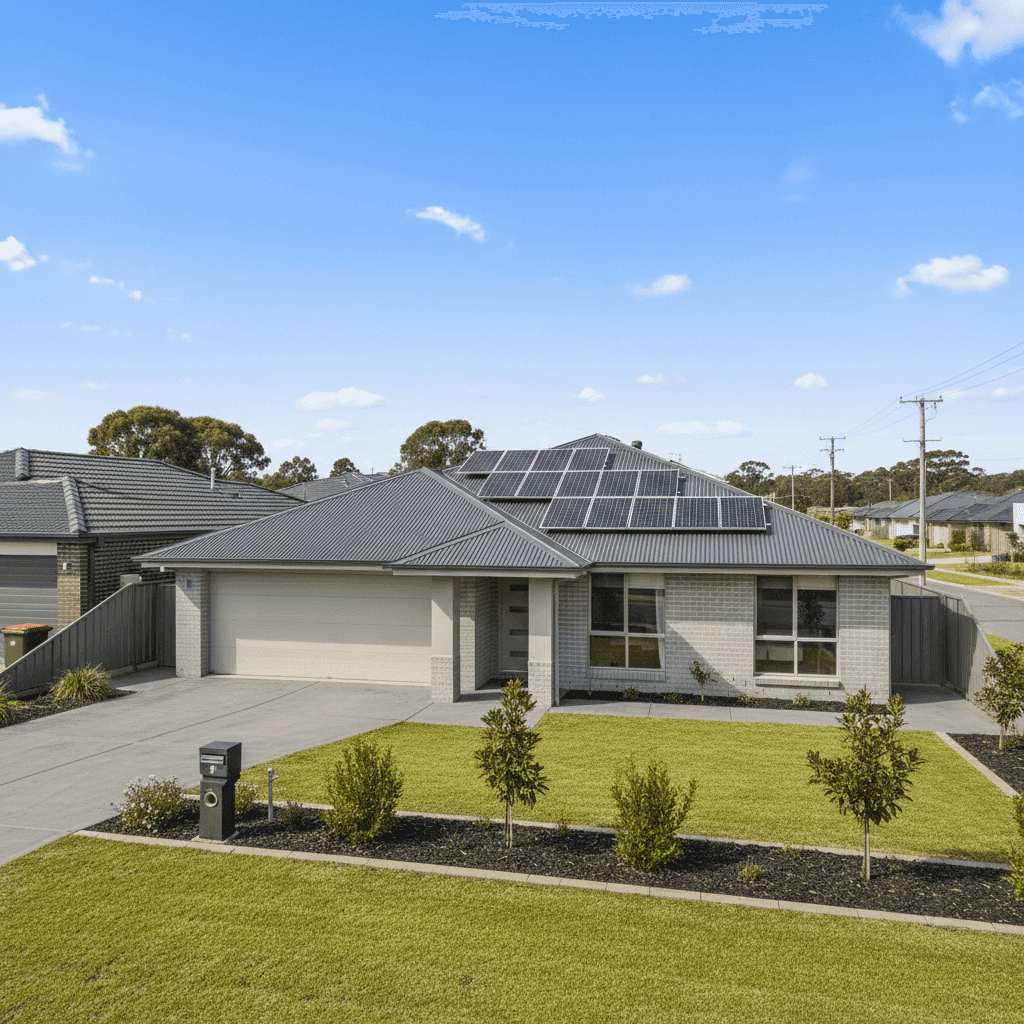

Modern Construction (2021) Homes built in recent years are constructed to stricter building codes, which generally means better resistance to weather events, fire, and structural issues. Insurers reward this with lower base premiums compared to older homes that may have ageing wiring, plumbing, or roofing.

Brick Veneer Walls Brick veneer is one of the most common and well-regarded external wall materials in Australia. It offers solid fire resistance and durability, which insurers view positively. Compared to timber-clad or fibrous cement homes, brick veneer properties often attract more competitive rates.

Steel / Colorbond Roof Colorbond roofing is highly regarded by insurers for its longevity, resistance to fire, and low maintenance requirements. It's far less susceptible to the kind of storm damage that can plague older terracotta or concrete tile roofs, making it a premium-friendly feature.

Slab Foundation Concrete slab foundations are considered low-risk by insurers — there's no subfloor space to harbour moisture, pests, or structural decay. This contributes to a clean risk profile.

Solar Panels This property has solar panels installed. It's worth confirming with your insurer that the panels are explicitly covered under your building sum insured, as some policies treat them as a standard inclusion while others may require them to be listed separately. Given the replacement cost of a modern solar system, this is an important detail to clarify.

No Pool, No Cyclone Risk Zone The absence of a swimming pool removes a common source of liability and accidental damage claims. And while Cliftleigh sits within the Hunter region, it falls outside designated cyclone risk areas — another factor that keeps premiums more manageable.

Timber / Laminate Flooring Flooring type can influence contents and internal damage claims. Timber and laminate floors are durable but can be susceptible to water damage, so it's worth ensuring your policy covers internal water ingress adequately.

---

Tips for Homeowners in Cliftleigh

1. Review your building sum insured regularly Construction costs have risen significantly in recent years. A sum insured of $557,000 for a 214 sqm home built to modern standards may be appropriate today, but it's worth reassessing annually. Underinsurance is one of the most common — and costly — mistakes homeowners make. Use a building cost calculator or speak with a quantity surveyor if you're unsure.

2. Confirm solar panel coverage explicitly Don't assume your solar panels are automatically included. Contact your insurer and ask specifically whether the panels, inverter, and associated wiring are covered under the building policy and to what value. If they're not listed, request an endorsement.

3. Consider your excess carefully This quote carries a $3,000 building excess, which is on the higher end. A higher excess typically lowers your premium, but it means you'll need to cover more out of pocket when making a claim. Think about whether that trade-off suits your financial situation — particularly for smaller claims like storm damage repairs.

4. Compare quotes at renewal time Even a "fair" quote can be improved upon. Insurance markets shift year to year, and loyalty doesn't always pay. Before your policy renews, take 10 minutes to compare quotes on CoverClub to make sure you're still getting a competitive deal.

---

Ready to Compare?

Whether you're a first-time buyer in Cliftleigh or a long-term homeowner reviewing your cover, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see what multiple insurers would charge for your specific property — get a quote today and find out if you can do better than average.