If you own a home in Clinton, QLD 4680, you're probably wondering whether you're paying a fair price for your home insurance — or leaving money on the table. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Clinton, examining how it stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $2,845 per year (or $269 per month), covering both building and contents. The building is insured for $738,000 and contents for $200,000, with a building excess of $2,000 and a contents excess of $600.

Our pricing engine rates this quote as FAIR — Around Average, which is a solid result for a mid-sized Queensland home. It's not the cheapest on the market, but it's well within a reasonable range given the property's characteristics and location. Homeowners who see a "Fair" rating can generally feel confident they aren't being significantly overcharged, though there's always room to explore whether a better deal exists elsewhere.

---

How Clinton Compares

To put this quote in proper context, let's look at how it measures up across three levels — suburb, state, and nation.

| Benchmark | Average | Median |

|---|---|---|

| Clinton (4680) | $3,097/yr | $3,153/yr |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

At $2,845/yr, this quote sits below the Clinton suburb average of $3,097 and well below the Queensland state average of $4,547. It's also slightly below the national average of $2,965, which is a positive sign.

The suburb data (based on 17 quotes in Clinton) shows a 25th percentile of $2,322 and a 75th percentile of $3,744 — meaning this quote lands comfortably in the middle of the pack for the area. Homeowners paying above $3,744 in Clinton may want to reassess whether their current policy is still competitive.

Queensland as a whole tends to attract higher premiums than the national average, largely due to elevated weather risks across much of the state. You can explore Queensland insurance trends or national home insurance data to see how your own property compares.

---

Property Features That Affect Your Premium

Several characteristics of this Clinton property influence how insurers price the risk — and in this case, a number of factors work in the homeowner's favour.

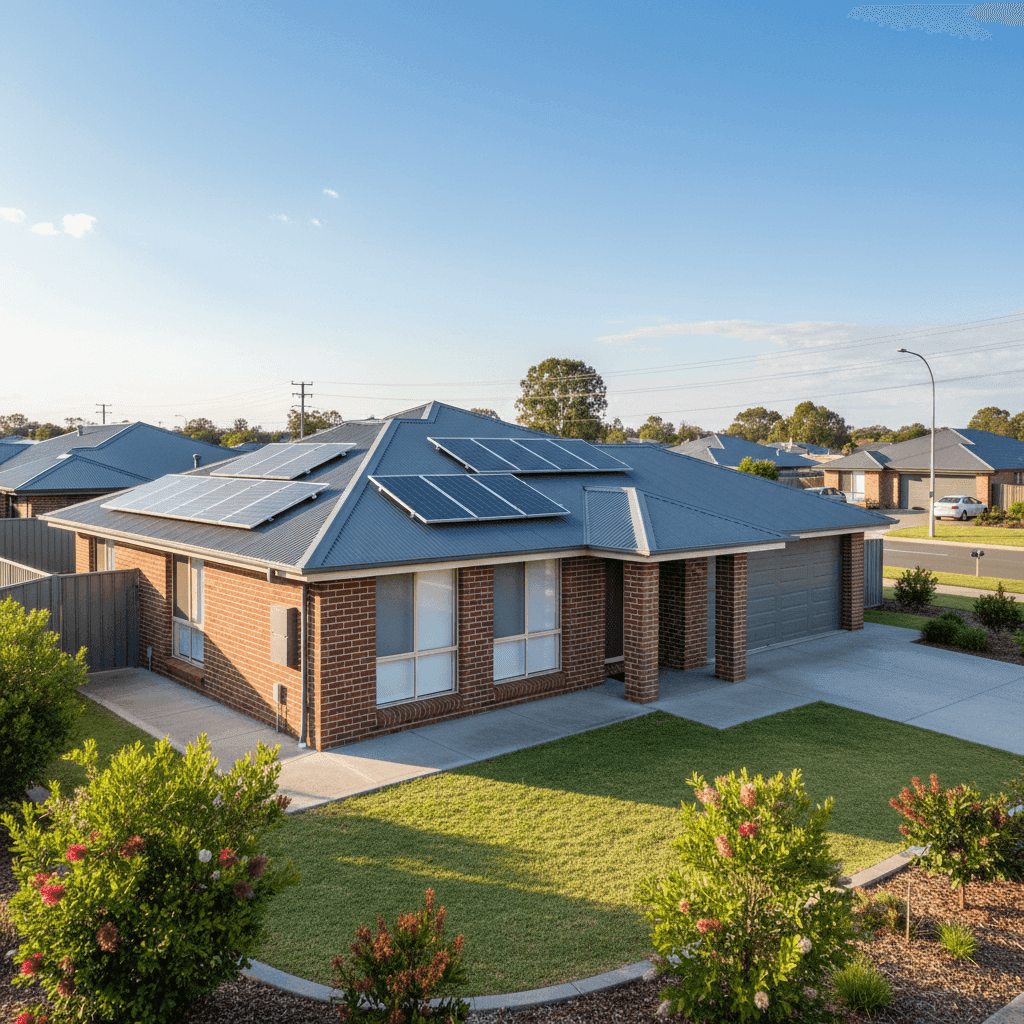

Brick Veneer Walls & Colorbond Roof

Brick veneer construction is well-regarded by insurers for its durability and fire resistance. Combined with a steel Colorbond roof, this home presents a relatively low structural risk profile. Colorbond roofing is particularly valued in Queensland for its resilience to heat, wind, and rain — all common weather events in the Gladstone region.

Concrete Slab Foundation

A slab-on-ground foundation is generally considered low risk from an insurance perspective. It's less susceptible to subsidence, pest damage, and moisture-related issues compared to suspended timber floors, which can contribute to lower premiums.

Tile Flooring

Tiled flooring throughout the home is a practical choice in Queensland's climate and is typically viewed favourably by insurers. Tiles are durable, water-resistant, and less prone to damage from humidity or minor flooding events.

Solar Panels

This property includes solar panels, which are worth noting from an insurance standpoint. Solar panels are generally covered under home and contents policies, but homeowners should confirm with their insurer that the panels are explicitly included in the building sum insured. Panels can be costly to replace, so it's worth ensuring the $738,000 building cover is adequate to include them.

No Pool, No Ducted Climate Control

The absence of a swimming pool removes a common liability risk, which can contribute to slightly lower premiums. No ducted air conditioning also means fewer mechanical systems that could fail or cause water damage — another modest positive for insurers.

1995 Build

At around 30 years old, this home sits in a middle ground — old enough that some components (roofing, plumbing, electrical) may be approaching the end of their serviceable life, but not so old that insurers apply significant age-related loading. Regular maintenance is key for homes of this vintage.

Standard Fittings

With standard-quality fittings, the contents and internal fixtures are priced at a reasonable level. Homes with high-end or luxury fittings often attract higher premiums due to the increased cost of replacement.

---

Tips for Homeowners in Clinton

Whether you're renewing your policy or shopping around for the first time, here are four practical steps to help Clinton homeowners get the most from their home insurance.

- Review your sum insured annually. Building costs have risen significantly in recent years. Make sure your $738,000 building cover still reflects what it would actually cost to rebuild your home from scratch — not just its market value. Underinsurance is one of the most common — and costly — mistakes homeowners make.

- Check that your solar panels are covered. Confirm with your insurer that your solar system is explicitly included under your building policy and that the sum insured accounts for their replacement value. Some policies treat panels as an optional add-on or have specific sub-limits.

- Consider your excess settings carefully. This policy carries a $2,000 building excess and $600 contents excess. A higher excess typically reduces your premium, but make sure you could comfortably cover that amount out of pocket in the event of a claim. If cash flow is a concern, a lower excess might be worth the extra cost.

- Compare quotes before your renewal date. The Clinton suburb data shows a wide spread of premiums — from $2,322 at the 25th percentile to $3,744 at the 75th. That's a $1,400+ difference for what could be a very similar property. Shopping around can make a real difference.

---

Ready to Find a Better Deal?

Whether this quote matches your own situation or you're simply curious about what you should be paying, CoverClub makes it easy to compare home insurance options across Australia. Get a personalised quote in minutes and see how your premium stacks up against real data from your suburb and state.

👉 Compare home insurance quotes at CoverClub — it's free, fast, and built for Australian homeowners.