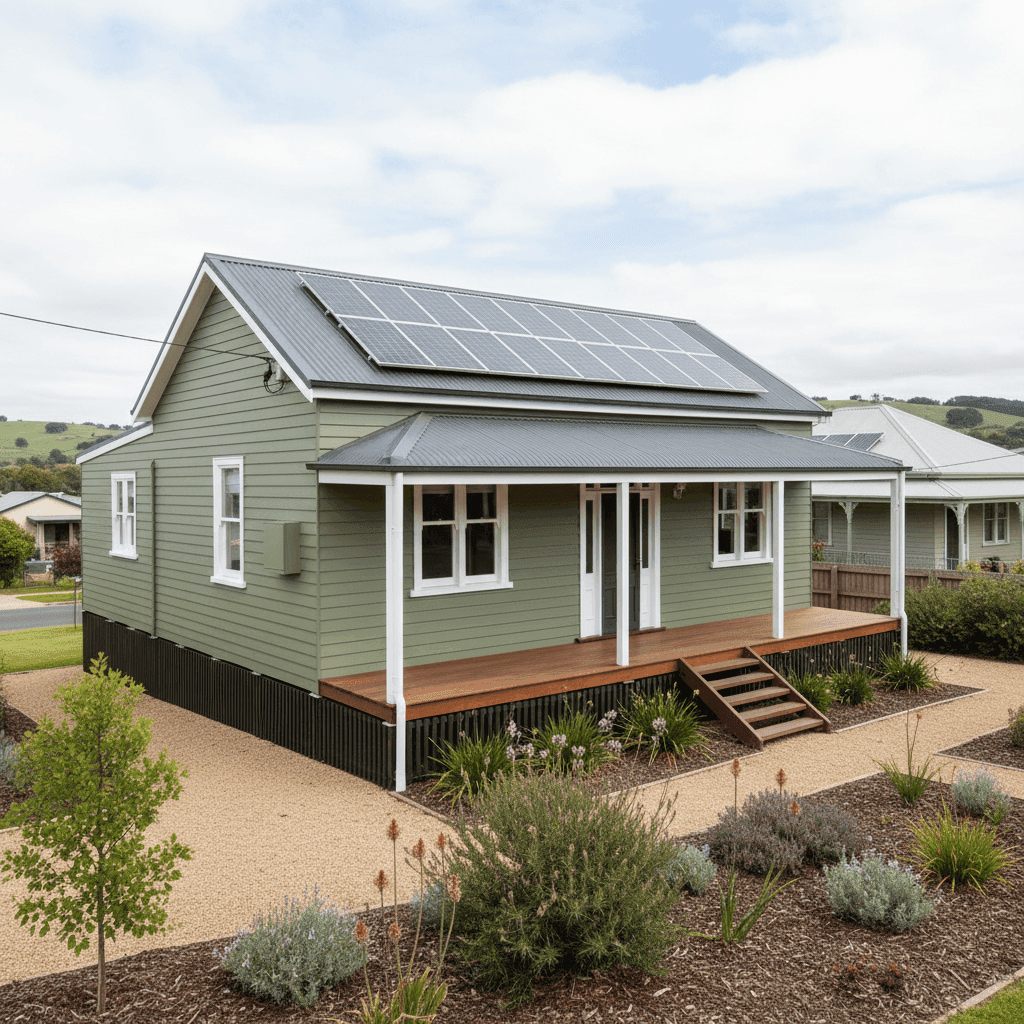

Cobden is a quiet rural township in Victoria's South West, nestled within the Colac Otway local government area. Known for its dairy farming heritage and relaxed lifestyle, it's the kind of place where homes have character — and often, a few decades of history behind them. This article takes a close look at a real home and contents insurance quote for a three-bedroom, free-standing weatherboard home in Cobden (postcode 3266), breaking down whether the price stacks up and what local homeowners should know before renewing or switching their cover.

---

Is This Quote Fair?

The quote in question comes in at $1,291 per year (or $134/month) for combined home and contents insurance, covering a building sum insured of $500,000 and $40,000 worth of contents. The building excess is $3,000 and the contents excess is $500.

CoverClub has rated this quote as FAIR — Around Average, and the data backs that up. Within Cobden itself, the suburb median premium sits at $1,312/yr — meaning this quote lands just below the midpoint of what locals are typically paying. It also falls comfortably within the interquartile range of $1,050 to $1,760, which is where the bulk of comparable quotes cluster.

In other words, this isn't a bargain-basement price, but it's also not overpriced. For a 1940s weatherboard home on stumps with solar panels, sitting just under the suburb median is a reasonable outcome — and one worth understanding in context.

---

How Cobden Compares

To appreciate how this quote sits in the broader landscape, it helps to zoom out.

| Benchmark | Premium |

|---|---|

| This quote | $1,291/yr |

| Cobden suburb median | $1,312/yr |

| Cobden suburb average | $1,802/yr |

| Colac Otway LGA average | $2,576/yr |

| VIC state median | $2,718/yr |

| VIC state average | $3,000/yr |

| National median | $2,764/yr |

| National average | $5,347/yr |

The numbers tell an encouraging story for Cobden residents. Premiums in this postcode are substantially lower than both the Victorian state average and the national average — the latter being more than four times the cost of this particular quote. Even compared to the broader Colac Otway LGA average of $2,576/yr, Cobden comes out well ahead.

It's worth noting that the suburb average ($1,802) is notably higher than the median ($1,312), which suggests a small number of higher-cost quotes are pulling the average up. With only 14 quotes in the Cobden suburb sample, this is a relatively small dataset — so individual property characteristics can have an outsized effect on the figures.

---

Property Features That Affect Your Premium

Every insurer weighs up a combination of property-specific and location-based risk factors when calculating a premium. Here's how the key features of this home likely influence its pricing:

Weatherboard Timber Construction

Weatherboard homes are among the most common dwelling types in regional Victoria, but they do carry a higher fire risk than brick veneer or full brick construction. Timber walls can be more susceptible to ember attack and are generally more expensive to repair or replace. Insurers typically price this risk into the premium — so it's somewhat impressive that this quote remains competitive.

Steel/Colorbond Roof

On the upside, a Colorbond steel roof is generally viewed favourably by insurers. It's durable, low-maintenance, and performs well in high-wind events and heavy rain. Compared to older terracotta tile or corrugated iron roofing, Colorbond tends to attract a more modest premium loading.

Stump Foundation (Elevated Less Than 1m)

The home sits on stumps and is elevated by less than one metre. This style of foundation is very common in older Victorian homes and can offer some flood resilience, though it also introduces vulnerability to underfloor moisture and pest damage. From an insurance perspective, the low elevation means it doesn't attract the same flood-risk loading as more significantly elevated or low-lying properties.

Timber/Laminate Flooring

Timber and laminate floors are a standard feature in homes of this era and generally don't push premiums significantly in either direction. However, they can be costly to replace if water damage occurs — something worth keeping in mind when reviewing your contents and building cover limits.

Solar Panels

The presence of solar panels adds a modest layer of complexity to a home insurance policy. Panels are typically covered under the building sum insured, but it's worth confirming with your insurer that they're explicitly included — particularly for damage caused by storms, hail, or fire. Given the age of this home, ensuring the solar installation is compliant and professionally fitted will also support any future claims.

1940s Construction

Homes built in or around 1940 can present higher rebuild costs due to the use of older materials and construction techniques that may no longer be standard. This makes accurate sum insured calculation especially important — underinsurance is a real risk for older homes.

---

Tips for Homeowners in Cobden

1. Review Your Sum Insured Regularly

With a building sum insured of $500,000 on a 205 sqm home, it's important to ensure this figure reflects the true cost of rebuilding — not the market value. Construction costs have risen significantly in recent years, and older weatherboard homes can be particularly expensive to rebuild due to non-standard materials. Use a building cost calculator or speak to a local builder to sense-check your coverage.

2. Confirm Solar Panels Are Covered

Not all policies automatically extend to solar panel systems as part of the building cover. Check your Product Disclosure Statement (PDS) carefully, and ask your insurer directly whether storm, hail, and fire damage to panels is included — and whether there are any limits on the value covered.

3. Consider Your Excess Trade-Off

This quote carries a $3,000 building excess, which is on the higher end. A higher excess generally reduces your annual premium, but it means you'll need to cover more out of pocket in the event of a claim. If cash flow is a concern, it may be worth requesting a quote with a lower excess to compare the overall cost difference.

4. Shop Around at Renewal Time

Even though this quote rates as fair, the insurance market changes regularly — and so do individual circumstances. Making a habit of comparing quotes annually (rather than auto-renewing) can surface meaningful savings. CoverClub makes it easy to benchmark your current premium against the market before you commit.

---

Ready to Compare?

Whether you're a first-time buyer in Cobden or a long-term homeowner looking to make sure you're not overpaying, comparing quotes is one of the simplest ways to protect both your home and your budget. Get a home insurance quote at CoverClub and see how your current premium stacks up against real data from your suburb and beyond.