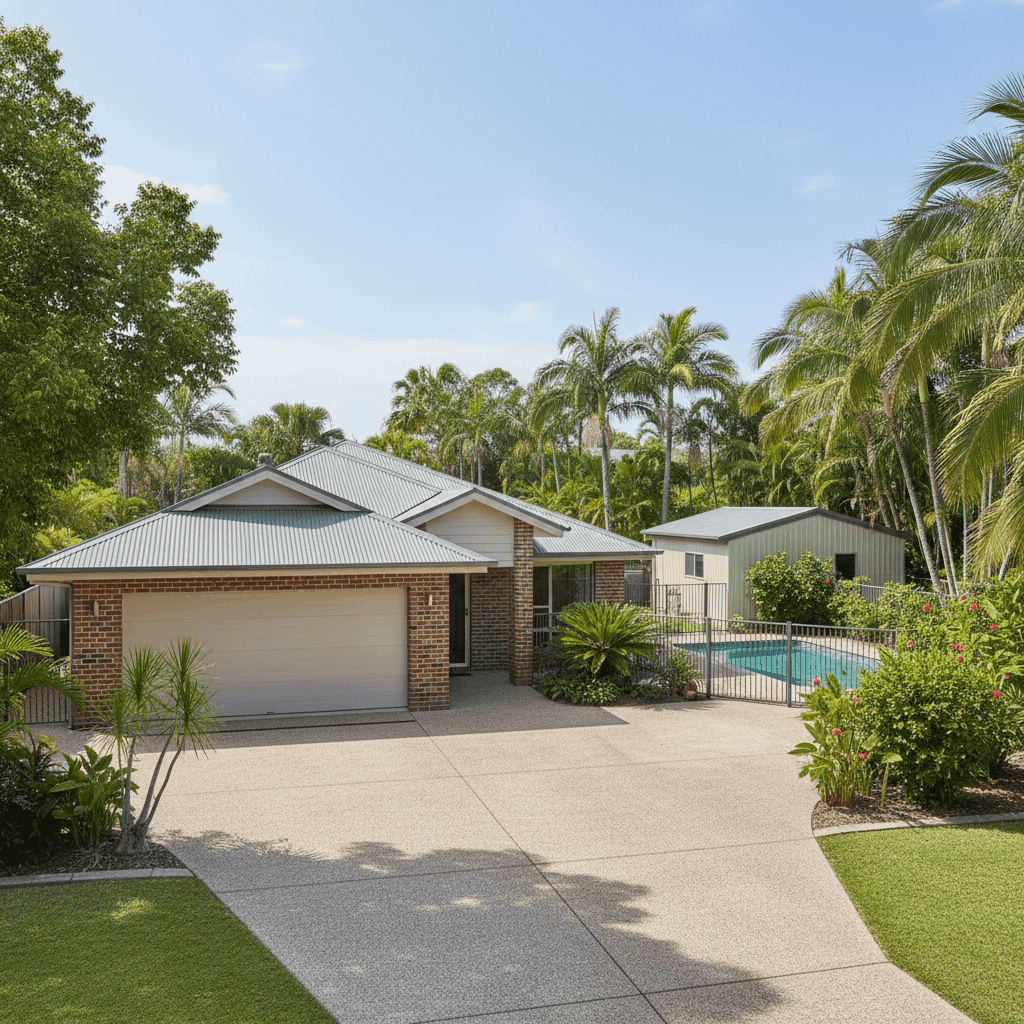

If you own a free standing home in Coconut Grove, NT 0810, you already know that insuring a property in Darwin's northern suburbs comes with its own set of considerations — from tropical weather to cyclone season. This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom brick veneer home in Coconut Grove, and puts it in context against local, state, and national benchmarks so you can judge whether you're getting a fair deal.

---

Is This Quote Fair?

The quote in question comes in at $5,057 per year (or $478/month) for combined home and contents cover, with a building sum insured of $1,200,000 and contents valued at $120,000. Both the building and contents excess are set at $1,000.

Based on our pricing data, this quote is rated CHEAP — below the suburb average. That's a meaningful result for a Darwin-area property, where premiums can climb steeply due to cyclone exposure and the elevated cost of rebuilding in a remote capital city.

Compared to the suburb average of $6,010/year and the suburb median of $5,991/year, this quote sits roughly $953 below average — a saving of around 16%. It also falls below the 25th percentile for the suburb ($5,556/year), meaning it's among the most competitively priced quotes recorded in the area. For homeowners in Coconut Grove, that's worth paying attention to.

---

How Coconut Grove Compares

Understanding how your suburb fits into the broader insurance landscape helps you gauge whether local pricing is genuinely competitive or simply the norm in a high-risk region.

| Benchmark | Average Premium |

|---|---|

| Coconut Grove (suburb avg) | $6,010/yr |

| Darwin LGA average | $15,687/yr |

| NT state average | $10,773/yr |

| National average | $5,347/yr |

A few things stand out here. First, the Darwin LGA average of $15,687/year is extraordinarily high — more than three times the national average. This reflects the significant cyclone, storm surge, and flooding risks across greater Darwin. Coconut Grove, however, tracks considerably lower than the broader LGA average, suggesting the suburb carries a somewhat more favourable risk profile within the Darwin context.

The NT state average of $10,773/year is also well above the national figure, though the state median of $3,402/year tells a different story — indicating that a large proportion of NT properties attract lower premiums, with a smaller cohort of very high-risk properties pulling the average upward.

At the national level, the average sits at $5,347/year and the median at $2,764/year. The quoted premium of $5,057 is actually below the national average, which is a strong result for a cyclone-rated property in the Northern Territory.

Explore more data on Coconut Grove insurance premiums, NT state-wide statistics, or national home insurance benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a direct bearing on what insurers charge — and understanding them helps you make sense of the final figure.

Cyclone Risk Area

This is arguably the single biggest factor. Coconut Grove falls within a designated cyclone risk zone, which means insurers apply a cyclone-specific excess and factor in the potential for wind, rain, and storm surge damage. Cyclone cover is typically included in standard home insurance policies in the NT, but the risk loading can be substantial.

Age and Construction (1973, Brick Veneer, Colorbond Roof)

Built in 1973, this home is over 50 years old — a factor that can increase premiums due to the potential for ageing plumbing, wiring, and structural components. That said, brick veneer walls are generally well-regarded by insurers for their resilience, and a steel Colorbond roof is considered one of the more durable roofing options in cyclone-prone regions, potentially moderating the premium impact.

Pool and Granny Flat

The presence of a swimming pool adds liability exposure and increases the overall replacement cost of the property. Similarly, a granny flat on the premises represents additional insurable structure, which contributes to the higher building sum insured of $1.2 million. Both features are reflected in the premium.

Ducted Climate Control

Ducted air conditioning is a significant fixed asset in any Darwin home — virtually a necessity given the climate — and its inclusion in the building sum insured adds to the overall replacement value.

Slab Foundation and Tile Flooring

A concrete slab foundation is standard in the NT and generally viewed favourably by insurers for its stability. Tiled flooring throughout is both practical in a tropical climate and relatively straightforward to replace compared to timber or carpet, which can be a minor positive from an insurer's perspective.

---

Tips for Homeowners in Coconut Grove

1. Review Your Building Sum Insured Carefully

At $1,200,000, the building sum insured accounts for the granny flat, pool, and ducted systems — but it's worth having a quantity surveyor or using an online calculator to verify this figure periodically. Underinsurance is a serious risk, particularly in Darwin where construction costs are among the highest in the country.

2. Prepare Your Property Before Cyclone Season

Insurers may reduce claims — or in some cases dispute them — if a property hasn't been adequately maintained ahead of a cyclone event. Securing outdoor furniture, clearing gutters, trimming overhanging trees, and checking roof fixings each year can make a material difference to both your safety and your claims outcome.

3. Compare Quotes Annually

The fact that this quote came in below both the suburb average and the national average is a good outcome — but it's not guaranteed to repeat at renewal. Insurers regularly adjust their pricing models, and loyalty doesn't always translate to savings. Shopping around each year via a comparison platform is one of the simplest ways to stay ahead.

4. Check Your Contents Cover Reflects Reality

$120,000 in contents cover is a reasonable starting point for a 3-bedroom home, but it's easy for this figure to become outdated as you acquire new furniture, appliances, or electronics. A quick annual stocktake — particularly after major purchases — helps ensure you're not underinsured when it matters most.

---

Find a Better Deal with CoverClub

Whether you're renewing your current policy or shopping for the first time, comparing quotes is the fastest way to find cover that suits your property and your budget. CoverClub makes it easy to see how your premium stacks up against others in your suburb and across the country. Get a home insurance quote today and find out if you could be paying less.