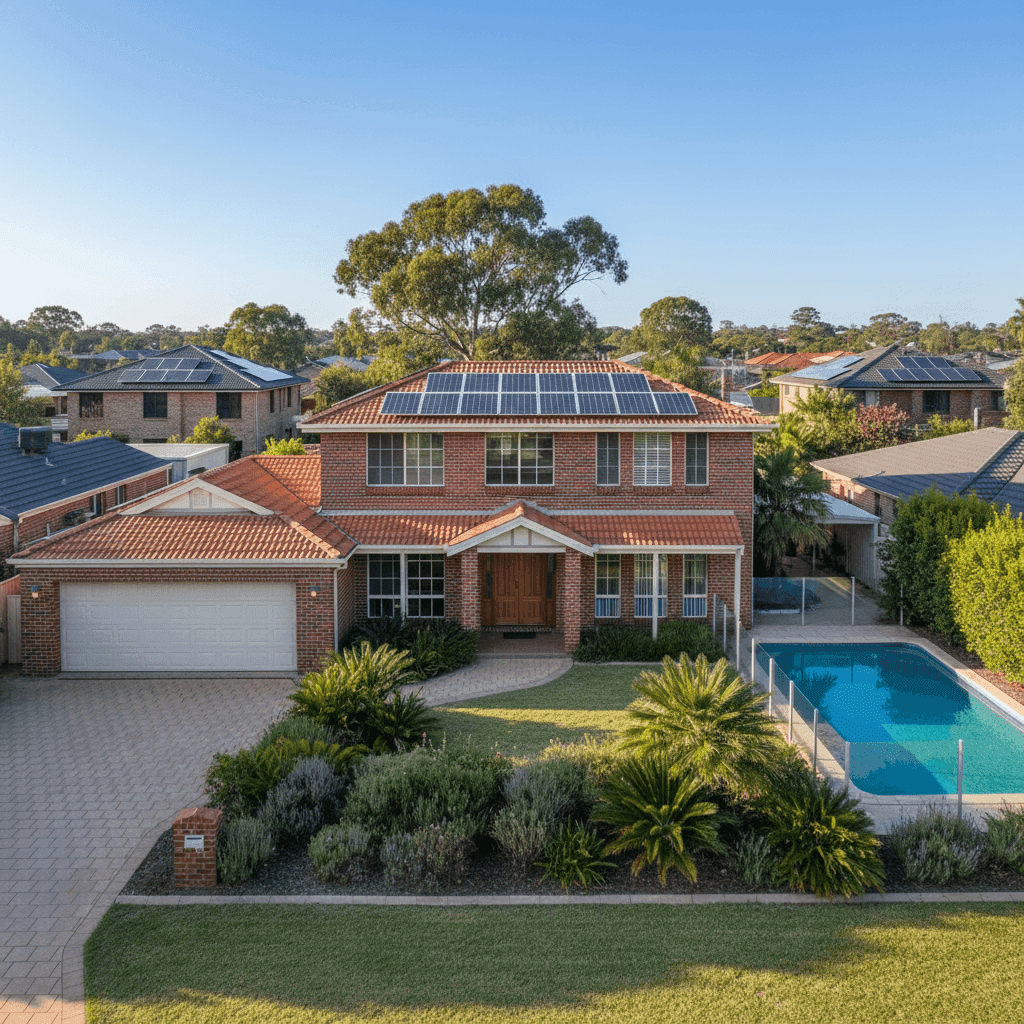

Connolly is a well-established residential suburb in Perth's northern corridor, sitting within the City of Wanneroo and offering the kind of quiet, family-friendly streets that make it a popular choice for owner-occupiers. If you own a free standing home here — particularly a larger double brick property built in the early 1990s — understanding what you should be paying for home and contents insurance is an important part of managing your household budget. This article breaks down a real quote for a 5-bedroom home in Connolly (postcode 6027) and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,647 per year (or $254 per month) for combined home and contents cover, with a building sum insured of $1,177,000 and contents valued at $143,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, which is an accurate reflection of where it sits in the data. It's not a standout bargain, but it's also not overpriced relative to what comparable homes in the area are attracting. For a property of this size and specification — 277 sqm, five bedrooms, two bathrooms, a pool, solar panels, and ducted climate control — a premium in this range is broadly reasonable.

The $1,000 excess on both building and contents is a standard configuration. Opting for a higher excess (say, $2,000 or $2,500) could bring the annual premium down meaningfully, which is worth exploring if you're comfortable absorbing a larger out-of-pocket cost in the event of a claim.

---

How Connolly Compares

To understand whether this quote is competitive, it helps to look at it against a few different benchmarks. You can explore the full data on the Connolly suburb stats page, the WA state overview, and national insurance statistics.

| Benchmark | Premium |

|---|---|

| This quote | $2,647/yr |

| Connolly suburb average | $2,466/yr |

| Connolly suburb median | $2,695/yr |

| Connolly 25th percentile | $2,187/yr |

| Connolly 75th percentile | $2,738/yr |

| WA state average | $2,811/yr |

| WA state median | $2,127/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| LGA (Wanneroo) average | $1,550/yr |

A few things stand out here. At $2,647, this quote sits above the suburb average ($2,466) but below the suburb median ($2,695) — meaning roughly half of comparable quotes in the area are actually more expensive. It also falls comfortably below the WA state average of $2,811, and well below the national average of $5,347 (which is heavily influenced by high-risk areas in Queensland and Northern Australia).

The LGA average for Wanneroo of $1,550 is notably lower, but this figure likely reflects a broader mix of property types and cover levels across the local government area — including smaller homes and lower sum-insured policies — so it's not necessarily a direct comparison for a 5-bedroom property with a pool and solar.

Overall, the pricing here is in a sensible range. There's room to potentially do better, but this quote wouldn't raise any red flags.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them can help you have more informed conversations when comparing policies.

Double Brick Construction Double brick is one of the most resilient wall types in Australian residential construction. Insurers generally view it favourably because it offers strong resistance to fire and structural damage. This can work in your favour when it comes to pricing.

Tiled Roof Terracotta or concrete tiles are a durable roofing choice and are typically rated well by insurers. They hold up well against Perth's hot summers and occasional severe weather events, and they're less susceptible to ember attack than some other materials.

Slab Foundation A concrete slab foundation is standard for homes of this era in WA and is generally considered low-risk from an underwriting perspective. There's no subfloor cavity, which reduces some moisture-related risks.

Swimming Pool A pool adds to the replacement value of the property and increases the overall sum insured required. It also introduces some liability considerations, which can nudge premiums upward slightly.

Solar Panels Solar panels are increasingly common on Perth homes, and most insurers now include them as part of the building structure. However, they do add to the insured value and can be costly to replace, so it's worth confirming your policy explicitly covers them — including for storm and hail damage.

Ducted Climate Control Ducted air conditioning is a significant fixed installation and contributes to the building's replacement cost. Ensuring your sum insured accounts for the full cost of reinstating this system is important.

Timber and Laminate Flooring These flooring types are susceptible to water damage, which is one of the more common home insurance claims. It's worth checking your policy's terms around escape of liquid and storm-related water ingress.

Construction Year: 1992 At over 30 years old, this home is well past its initial build but still within a period of solid construction. Older homes can sometimes attract slightly higher premiums due to the age of plumbing, electrical systems, and roofing, so keeping these maintained is both a safety and insurance consideration.

---

Tips for Homeowners in Connolly

1. Review your sum insured regularly Building costs in Perth have risen considerably in recent years. A sum insured of $1,177,000 for a 277 sqm home works out to roughly $4,250 per square metre — which is in a reasonable range for a double brick home with quality inclusions, but worth validating with a building cost estimator to avoid being underinsured.

2. Check your solar panel coverage Not all policies automatically cover solar panels, or they may cap the payout. Ask your insurer specifically whether your panels are covered as part of the building, and whether accidental damage and storm damage are included.

3. Consider your excess strategically Both the building and contents excess on this policy are set at $1,000. If you have the financial buffer to handle a larger excess, increasing it to $2,000 or more can reduce your annual premium — sometimes by several hundred dollars. Just make sure it's an amount you could comfortably pay at short notice.

4. Compare quotes at renewal time The insurance market in WA is competitive, and premiums can vary significantly between providers for the same property. Even if your current quote is rated as fair, running a comparison at renewal could reveal a better deal — especially if your circumstances or the market have changed.

---

Compare Home Insurance Quotes in Connolly

Whether you're reviewing an existing policy or shopping around for the first time, it pays to see what the broader market has to offer. CoverClub makes it easy to compare home and contents insurance quotes tailored to your property. Get a quote today and find out if you could be getting better value on your cover.