Coochiemudlo Island is a small, tightly-knit community nestled in Moreton Bay, just a short ferry ride from Victoria Point on Queensland's southeast coast. It's the kind of place where people trade city noise for birdsong and bay breezes — but island living comes with its own set of insurance considerations. This article breaks down a real home and contents insurance quote for a 3-bedroom free standing home on Coochiemudlo Island, and examines how it stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property comes in at $3,526 per year (or around $338 per month), covering a building sum insured of $565,000 and $50,000 in contents — both with a $1,000 excess.

Our price rating for this quote is CHEAP, meaning it sits below the average for comparable properties in the area. That's a genuinely positive result for the homeowner, particularly given the unique characteristics of island-based properties, which can attract higher risk loadings from some insurers.

To put it in perspective: the suburb average for Coochiemudlo Island sits at $3,939 per year, and the median is $3,858. This quote comes in roughly $413 below the suburb average — a meaningful saving over time. Even when compared to the suburb's 25th percentile (the cheapest quarter of quotes) at $3,712, this premium remains competitive.

It's worth noting that the sample size for this suburb is relatively small (6 quotes), so averages can shift as more data comes in. That said, the trend is clear: this quote is well-positioned within the local market.

---

How Coochiemudlo Island Compares

Understanding where your suburb sits relative to broader benchmarks helps put your premium in context. Here's how Coochiemudlo Island (postcode 4184) shapes up:

| Benchmark | Premium |

|---|---|

| This Quote | $3,526/yr |

| Suburb Average | $3,939/yr |

| Suburb Median | $3,858/yr |

| LGA (Redland) Average | $3,178/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, the QLD state average of $9,129 per year is dramatically higher than what's being quoted in Coochiemudlo Island — but this figure is heavily skewed by high-risk postcodes in Far North Queensland, cyclone-prone coastal areas, and flood-affected regions. The state median of $3,903 is a more representative figure, and this quote sits just below that mark.

Compared to the national average of $5,347, this quote looks even more attractive. The national median of $2,764 is lower, but that includes a wide range of lower-risk metropolitan properties that naturally attract cheaper premiums.

You can explore more localised data for Coochiemudlo Island directly on the CoverClub suburb stats page.

Interestingly, the Redland LGA average of $3,178 is actually lower than this quote — though LGA-level averages can include a broad mix of property types, sizes, and risk profiles that don't necessarily reflect island-specific conditions.

---

Property Features That Affect Your Premium

Every property is different, and insurers assess a range of characteristics when calculating your premium. Here's how the features of this particular home likely influence its pricing:

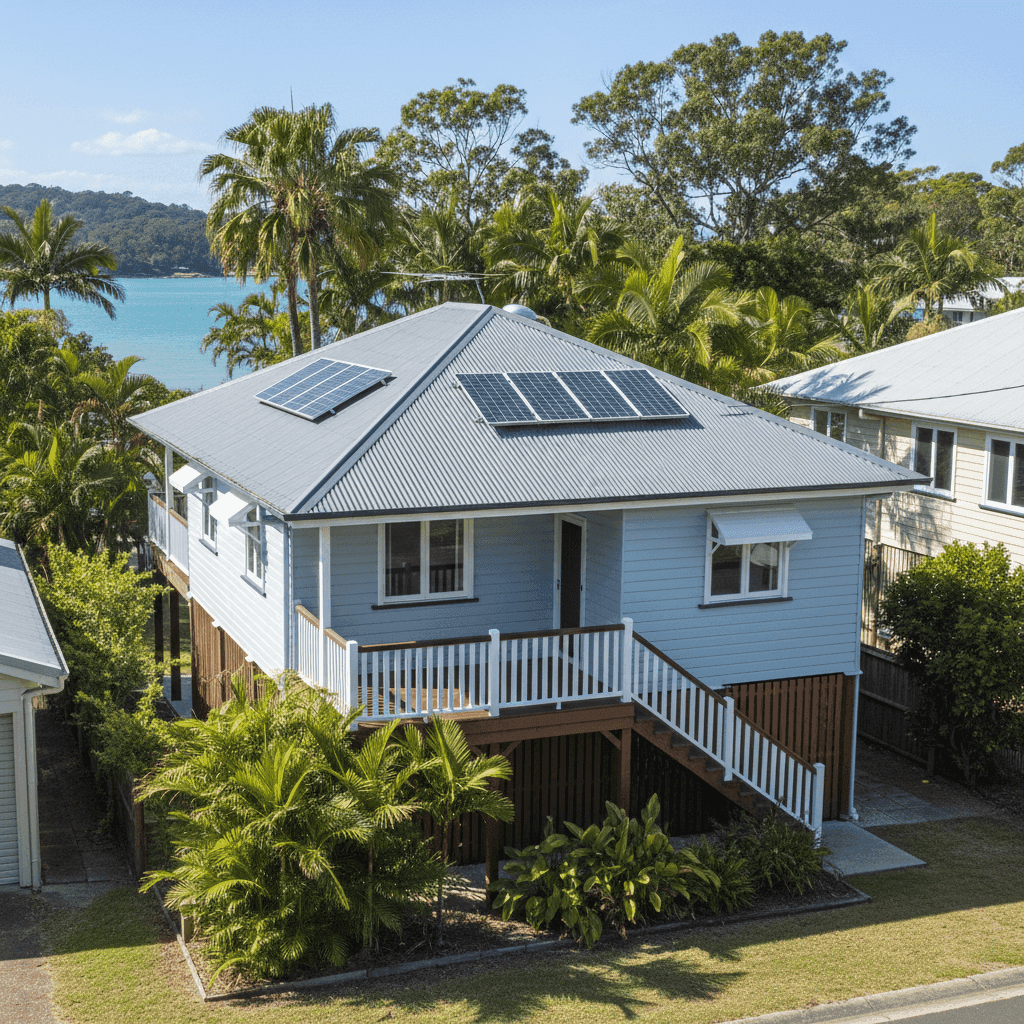

Weatherboard Timber Walls

Timber weatherboard is a classic Queensland construction material — attractive and well-suited to the climate, but considered higher risk by insurers than brick or concrete. Timber is more susceptible to fire spread, moisture damage, and pest damage (particularly termites), which can contribute to a higher base premium compared to masonry homes.

Steel / Colorbond Roof

On the upside, a Colorbond steel roof is viewed favourably by most insurers. It's durable, low-maintenance, and performs well in wet weather conditions — a significant plus for a property surrounded by water. It's also resistant to the kind of storm damage that can affect older tile roofs.

Elevated on Stumps (At Least 1 Metre)

This is a key factor for island properties. Being elevated by at least one metre on stumps significantly reduces the risk of inundation from storm surge, tidal flooding, or heavy rainfall events. Many insurers apply meaningful discounts for elevated homes in flood-adjacent areas, which likely contributes to this quote's competitive pricing.

Solar Panels

Solar panels are generally a neutral-to-positive feature for insurance purposes. They add value to the property and may need to be factored into the building sum insured, but they don't typically attract a premium loading. Ensuring your sum insured accounts for the replacement cost of the panels is important.

Ducted Climate Control

Ducted air conditioning adds to the rebuild cost of a home and may slightly increase the building sum insured required. At $565,000, the building coverage here appears appropriately calibrated for a 205 sqm home with these inclusions.

Timber / Laminate Flooring

Timber and laminate floors can be costly to replace after water or flood damage. For a home on stumps near the water, this is worth keeping in mind when reviewing contents and building coverage.

No Cyclone Risk

Coochiemudlo Island falls outside designated cyclone risk zones, which is a significant premium advantage compared to properties in North Queensland. Cyclone cover can add hundreds — sometimes thousands — of dollars to annual premiums in affected areas.

---

Tips for Homeowners in Coochiemudlo Island

Whether you're renewing your policy or shopping for the first time, here are some practical steps to make the most of your home insurance:

- Review your sum insured annually. Building costs have risen sharply in recent years. A home insured for $565,000 today may cost significantly more to rebuild in two or three years. Use a building cost calculator or speak to a local builder to sanity-check your coverage level.

- Don't underinsure your contents. $50,000 in contents cover is a reasonable starting point, but it's easy to underestimate the cumulative value of furniture, appliances, clothing, and electronics. Do a room-by-room inventory every year or two to keep your estimate current.

- Document island-specific risks. Properties on Coochiemudlo Island can be exposed to saltwater corrosion, moisture ingress, and occasional storm activity. Keep records of any maintenance, repairs, or upgrades — this can support a claim and demonstrate that the property has been well cared for.

- Compare quotes before renewing. Insurers adjust their pricing models regularly, and loyalty doesn't always pay. Even if your current premium looks competitive, it's worth running a comparison at renewal time to ensure you're still getting fair value.

---

Ready to Compare Your Options?

Whether you're a long-term Coochiemudlo Island resident or you've recently made the move to island life, making sure your home and contents are properly protected is essential. Get a home insurance quote through CoverClub to see how your current premium compares — it only takes a few minutes, and the savings could be well worth it.