If you own a free standing home in Cooma, NSW 2630, you've probably wondered whether your home insurance premium is reasonable — or whether you're quietly paying more than you need to. Cooma sits in the Snowy Monaro region, a picturesque part of New South Wales known for cold winters, alpine proximity, and a mix of older housing stock. All of these factors play a role in how insurers price your cover. In this article, we break down a real home and contents insurance quote for a four-bedroom weatherboard home in Cooma and put it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,548 per year (or $244/month) for combined home and contents cover, with a building sum insured of $859,000 and contents valued at $20,000. The building excess is $5,000 and the contents excess is $2,000.

Our pricing analysis rates this quote as Fair — Around Average. That's a reasonable outcome, but it's worth understanding what "average" actually means in this context.

The suburb average for Cooma (2630) sits at $2,162/year, with a median of $2,061/year. This quote is roughly $386 above the suburb average and $487 above the median — placing it in the upper half of the local market, though still well within the suburb's 75th percentile of $2,720/year. In other words, around a quarter of Cooma homeowners are paying more than this quote, and three-quarters are paying less.

The higher-than-median premium is likely driven by the relatively high building sum insured ($859,000), which is a significant coverage amount for this region. A larger insured value naturally increases the premium, even if the underlying risk profile of the property is unremarkable.

---

How Cooma Compares

To truly appreciate this quote, it helps to zoom out and look at the broader picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Cooma (2630) | $2,162/yr | $2,061/yr |

| Cooma LGA (Snowy Monaro) | — | — |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The NSW state average of $9,528/year is extraordinarily high — heavily skewed by expensive coastal and flood-prone areas like parts of Sydney, the Northern Rivers, and other high-risk zones. The NSW median of $3,770/year is a far more representative figure, and Cooma sits comfortably below it.

Compared to the national average of $5,347/year (median: $2,764/year), Cooma also fares well. The national median is actually slightly higher than Cooma's median, suggesting that homeowners in this part of the Snowy Mountains are, on balance, paying less than the typical Australian homeowner.

The LGA-level data (Snowy Monaro) shows an average of $3,100/year, which is above the Cooma suburb average — indicating that some surrounding areas within the LGA carry higher risk ratings or higher insured values.

For this particular quote at $2,548/year, you're paying above the Cooma median but below the LGA and state averages. That's a broadly reasonable position given the property's characteristics.

---

Property Features That Affect Your Premium

Several aspects of this property are worth examining through the lens of insurance risk.

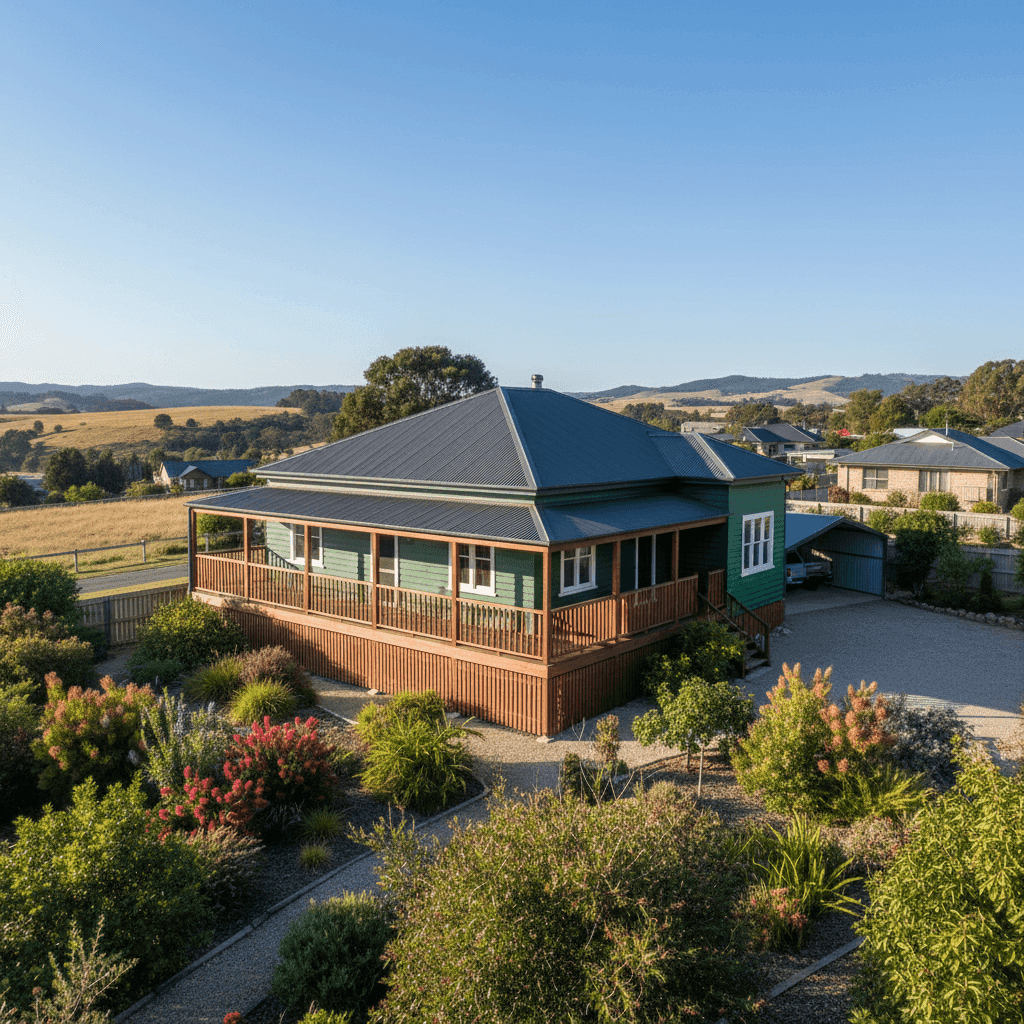

Weatherboard timber construction is one of the most significant factors. Older weatherboard homes are more susceptible to fire, moisture ingress, and general wear — all of which increase insurer risk. Combined with a construction year of 1955, this property is over 70 years old. Older homes often have ageing electrical wiring, plumbing, and structural elements that can be more costly to repair or replace. Insurers typically price this in.

The steel/Colorbond roof is actually a positive from an insurance perspective. Colorbond roofing is durable, low-maintenance, and performs well in extreme weather — including the heavy snowfall and freezing conditions Cooma can experience in winter. It's less prone to storm damage than older tile or corrugated iron roofing.

Stump foundations (also known as pier-and-beam) mean the home is slightly elevated, which can be beneficial in areas with ground movement or moisture — both relevant in the Snowy Monaro region. The elevation here is listed as less than 1 metre, so it's a modest raise rather than a full Queenslander-style lift.

Ducted climate control adds to the contents and fittings value, and is a common inclusion in Cooma homes given the cold winters. This system would be covered under the building sum insured and is factored into the overall rebuild cost.

Standard fittings quality and carpet flooring suggest a straightforward, mid-range interior — no high-end finishes that would push the rebuild cost significantly higher. The building size of 205 sqm is a reasonable footprint for a four-bedroom home, and at $859,000 sum insured, the implied rebuild rate is approximately $4,190/sqm — on the higher end, though potentially justified given the age and construction type.

---

Tips for Homeowners in Cooma

1. Review your sum insured carefully. At $859,000, the building sum insured is the single biggest driver of this premium. It's worth getting an independent building replacement cost estimate to confirm this figure is accurate — neither underinsured (which leaves you exposed) nor overinsured (which inflates your premium unnecessarily). Tools like Cordell Sum Sure can help.

2. Consider raising your excess to reduce your premium. The building excess on this policy is $5,000. If you're comfortable absorbing a higher out-of-pocket cost in a claim, some insurers will offer a meaningful premium reduction in exchange for a higher voluntary excess. This can be a smart trade-off for homeowners with emergency savings.

3. Keep your weatherboard cladding well-maintained. Insurers may scrutinise claims more closely — or apply exclusions — if a home has been poorly maintained. Repainting weatherboards regularly, sealing gaps, and keeping gutters clear of debris (especially important in Cooma's leaf-heavy autumn) reduces the risk of moisture damage and demonstrates good upkeep.

4. Compare quotes annually. The home insurance market is competitive, and premiums can shift significantly from year to year. With 36 quotes sampled in the Cooma area, there's a meaningful spread between the 25th percentile ($1,452/year) and the 75th percentile ($2,720/year). Shopping around at renewal time — even if you stick with your current insurer — is one of the easiest ways to avoid paying more than you need to.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for cover on a new property, CoverClub makes it easy to compare home insurance options tailored to your address and property type. Get a quote today and see how your premium stacks up against others in Cooma and across NSW.

For more local data, explore the Cooma suburb insurance stats or browse NSW-wide benchmarks to understand the full picture.