Nestled along the picturesque Myall Lakes region, Coomba Park is a quiet lakeside community on the Mid-Coast of New South Wales. It's the kind of place where weekenders and permanent residents alike enjoy a relaxed pace of life — but that doesn't mean home insurance should be an afterthought. This article breaks down a real home insurance quote for a 2-bedroom free standing home in Coomba Park (NSW 2428), examines how it stacks up against state and national benchmarks, and offers practical tips to help local homeowners get the best possible cover.

---

Is This Quote Fair?

The short answer: yes — and then some. This property received a Home and Contents quote of just $1,321 per year (or $129/month), covering a building sum insured of $539,000 and contents valued at $100,000. Our pricing engine rates this as CHEAP — meaning it sits meaningfully below the average for comparable properties.

To put that in perspective, the NSW state average for home insurance sits at $3,801 per year, with a median of $3,410. At the national level, the average is $2,965 and the median is $2,716. This quote comes in at roughly 65% below the national average — a significant saving for a policy that includes both building and contents cover.

Even more striking is the comparison with the local government area. The Mid-Coast LGA average premium is $4,441 per year, which reflects the elevated risk profile of coastal and semi-rural properties in this region. Against that benchmark, this quote represents a saving of over $3,100 annually.

In short, this is an excellent result — and understanding why it's priced this way can help other Coomba Park homeowners know what to look for.

---

How Coomba Park Compares

Coomba Park sits within the Mid-Coast LGA, a broad council area that spans everything from coastal holiday towns to rural hinterland. Insurance premiums across this LGA tend to run high — the $4,441 LGA average is well above both the NSW state average and the national figure, reflecting the mix of flood-prone, bushfire-adjacent, and coastal properties in the region.

Here's a quick snapshot of how this quote compares across different benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,321 |

| NSW State Average | $3,801 |

| NSW State Median | $3,410 |

| National Average | $2,965 |

| National Median | $2,716 |

| Mid-Coast LGA Average | $4,441 |

The fact that this property achieved a premium so far below every benchmark is a reflection of several favourable property characteristics — which we'll explore in the next section.

It's worth noting that suburb-level data for Coomba Park isn't yet available in our database, so we're relying on LGA and state-level comparisons. As more quotes flow through for this postcode, we'll be able to provide more granular local benchmarks. In the meantime, the NSW stats page offers a useful broader reference point.

---

Property Features That Affect Your Premium

Several characteristics of this particular home work in its favour from an insurance pricing perspective. Here's what stands out:

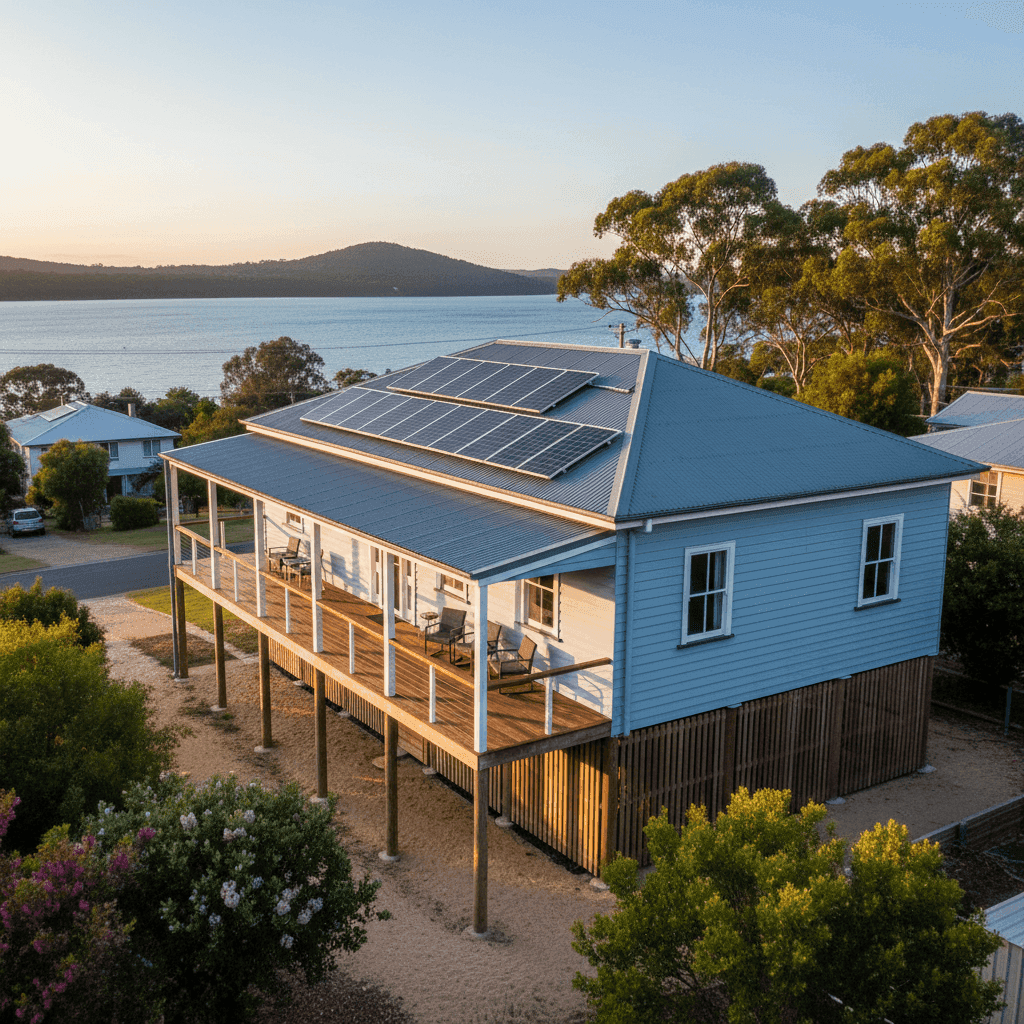

Weatherboard Timber Walls

Weatherboard wood is a classic Australian building material and one that insurers are very familiar with. While timber can carry some additional fire risk compared to brick veneer, modern weatherboard homes built after 2000 are generally well-regarded. This home, constructed in 2003, benefits from being built to more contemporary standards.

Steel/Colorbond Roof

Colorbond steel roofing is widely considered one of the better roofing choices for Australian conditions. It's durable, fire-resistant, and performs well in high-wind events. Insurers tend to view it favourably, and it can contribute to a lower premium compared to older materials like terracotta tiles or fibrous cement sheeting.

Elevated on Stumps (At Least 1 Metre)

This is likely one of the most significant premium-reducing factors for this property. Being elevated by at least one metre on stumps provides meaningful protection against flood and surface water inundation — a real concern in low-lying areas near Myall Lakes. Many insurers reward this elevation with lower flood-related loadings, which can dramatically reduce the overall premium.

Timber/Laminate Flooring

Flooring type can affect both the cost to replace and the susceptibility to water damage. Timber and laminate floors in an elevated home are less likely to suffer from groundwater-related damage, which aligns well with the flood-resilient design of this property.

Solar Panels

The presence of solar panels adds a modest layer of complexity to a home insurance policy — panels need to be covered against storm damage, hail, and theft. However, at standard fittings quality, this is a well-understood risk for insurers and typically doesn't result in significant premium increases.

No Pool, No Cyclone Risk Zone

The absence of a swimming pool removes a liability and replacement cost consideration. And while Coomba Park is on the NSW coast, it falls outside designated cyclone risk zones, which keeps wind-event loadings lower than they would be for properties further north.

---

Tips for Homeowners in Coomba Park

Whether you're a permanent resident or use your Coomba Park property as a holiday home, here are some practical steps to make sure you're getting the right cover at the right price.

1. Don't Underinsure Your Building

$539,000 may seem like a lot for a 2-bedroom, 105 sqm home, but building costs in regional NSW have risen sharply in recent years. Make sure your sum insured reflects the full cost to rebuild — not the market value of the property. These two figures can differ significantly, especially in coastal areas where trades and materials can cost more to source.

2. Review Your Contents Cover Annually

A contents value of $100,000 is a solid starting point, but it's easy for this figure to become outdated as you accumulate furniture, electronics, and appliances. Do a quick audit each year — especially after major purchases — to make sure you're not underinsured.

3. Ask About Flood Cover Specifically

Given the proximity to Myall Lakes and the broader waterway network in this area, it's essential to confirm that your policy includes flood cover — and to understand exactly how your insurer defines "flood" versus "storm surge" or "rainwater runoff." These distinctions matter when it comes to claim time.

4. Compare Quotes Before Renewing

One of the most common mistakes homeowners make is simply accepting their renewal notice each year without shopping around. The fact that this property achieved a premium well below the LGA average shows that significant savings are possible. Use a comparison tool like CoverClub to benchmark your renewal quote against the broader market before committing.

---

Ready to Compare Your Own Quote?

Whether you own a holiday retreat or a permanent residence in Coomba Park, getting the right home insurance at a fair price is easier than you might think. At CoverClub, we help Australian homeowners compare quotes quickly and transparently — so you can see exactly how your premium stacks up against local and national benchmarks. Start comparing today and find out if you're paying too much.