If you own a free standing home in Coomba Park, NSW 2428, you're likely no stranger to the charm — and the insurance considerations — that come with living on the Mid-Coast. Nestled beside Wallis Lake and surrounded by natural bushland, Coomba Park is a peaceful lakeside community, but its location and older housing stock mean that getting the right home insurance at a fair price genuinely matters. This article breaks down a real home and contents insurance quote for a four-bedroom property in the area, compares it against state and national benchmarks, and offers practical tips to help you make the most of your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,326 per year (or $228/month) for combined home and contents insurance, covering a building sum insured of $802,000 and contents valued at $102,000. The building excess is $2,000 and the contents excess is $1,000.

Our price rating for this quote is CHEAP — below average — which is genuinely good news for the homeowner. To put that in perspective:

- The NSW state average premium sits at $3,801/year, with a median of $3,410/year

- The national average is $2,965/year, with a median of $2,716/year

- The Mid-Coast LGA average is a notably high $4,463/year

This quote undercuts every one of those benchmarks — sitting well below the NSW average, beneath the national average, and dramatically lower than what many Mid-Coast homeowners are paying. That's a meaningful saving, particularly given the relatively high sum insured on the building.

It's worth noting that the $2,000 building excess is on the higher side, which does contribute to bringing the premium down. Higher excesses reduce the insurer's risk exposure, so they pass some of that saving on through a lower annual cost. Whether that trade-off suits you depends on your financial position — if a $2,000 out-of-pocket cost in a claims scenario is manageable, this structure can work well.

---

How Coomba Park Compares

While no suburb-level data is currently available for Coomba Park specifically, the broader regional picture tells an interesting story. You can explore Coomba Park insurance statistics as more data becomes available.

Looking at NSW-wide insurance data, premiums across the state average $3,801/year — reflecting the diversity of risks from flood-prone western plains to bushfire-exposed hinterlands and coastal storm zones. The Mid-Coast LGA average of $4,463/year is notably higher than the state figure, suggesting that insurers price this region with elevated caution — likely due to flood risk, storm exposure, and the prevalence of older dwellings.

Against the national average of $2,965/year, this quote still comes in cheaper, which is somewhat surprising given the regional risk profile. It suggests the specific property characteristics — or the insurer's own pricing model — have worked in this homeowner's favour.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,326 |

| National Average | $2,965 |

| National Median | $2,716 |

| NSW Average | $3,801 |

| NSW Median | $3,410 |

| Mid-Coast LGA Average | $4,463 |

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on how insurers price the risk. Here's what stands out:

Fibro / Asbestos External Walls

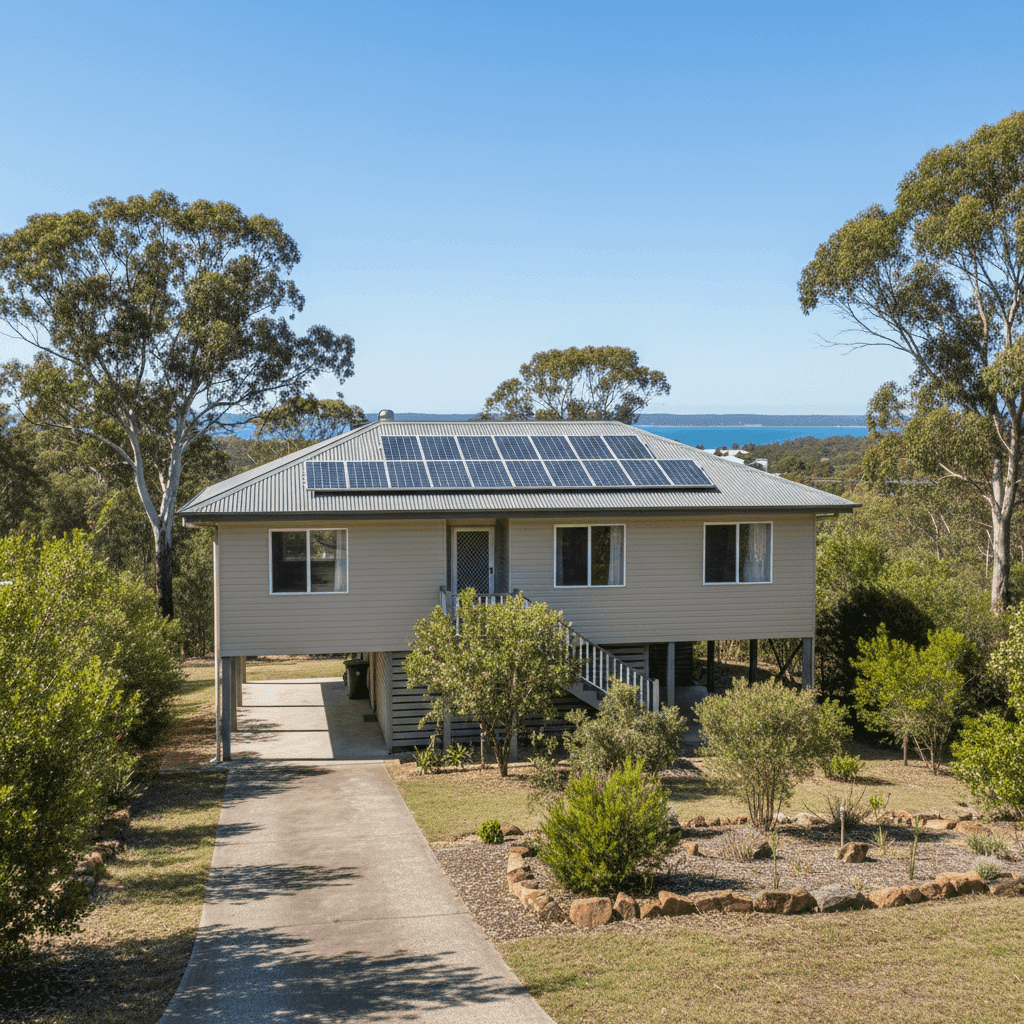

This is one of the most significant rating factors. Homes built with fibro asbestos cladding — common in properties constructed before the mid-1980s, as this one was (1985) — attract higher scrutiny from insurers. Asbestos-containing materials require specialist remediation if damaged, which dramatically increases repair costs. Some insurers apply loadings or exclusions for these properties, so finding a competitive quote is a real win.

Steel / Colorbond Roof

On the positive side, a steel Colorbond roof is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well in storms compared to older tile or corrugated iron options. This likely helps offset some of the risk associated with the wall construction.

Elevated Foundation (At Least 1 Metre)

The property being elevated by at least one metre is a meaningful factor in flood and inundation risk. In a lakeside location like Coomba Park — where storm surges, high tides, and heavy rainfall can raise water levels — elevation provides a degree of physical protection that insurers recognise. It may well be contributing to the competitive premium here.

1985 Construction

Older homes generally cost more to insure due to the age of electrical wiring, plumbing, and structural materials. A 1985 build is approaching 40 years old, which places it in a bracket where insurers may apply age-related loadings. The $802,000 sum insured reflects the true replacement cost of rebuilding to current standards — a critical figure to get right.

Solar Panels

The presence of solar panels adds a modest layer of complexity to the risk profile. Panels need to be covered for storm damage, hail, and electrical faults. Most home insurance policies include solar panels as part of the building cover, but it's worth confirming this with your insurer and ensuring the replacement value is factored into your sum insured.

Slab Foundation

A concrete slab foundation is standard and generally unproblematic for insurers, though it can be more costly to repair than stumped or suspended floors if subsidence or cracking occurs.

---

Tips for Homeowners in Coomba Park

1. Review Your Building Sum Insured Annually

Construction costs have risen sharply in recent years across regional NSW. A sum insured of $802,000 on a 235 sqm home is substantial, but it's important to verify this figure reflects current rebuild costs — not just the market value of the land and structure. Use an independent building calculator or speak with a local builder to sense-check the number each year.

2. Understand Your Asbestos Cover

If your home has fibro asbestos cladding, read your policy's fine print carefully. Some policies limit cover for asbestos-related removal and disposal, or require you to use approved contractors. Knowing this before you need to make a claim can save significant stress and expense.

3. Check Your Flood and Storm Surge Definitions

Coomba Park's proximity to Wallis Lake means flood and storm surge risk is real. Insurers define "flood" in different ways — some policies cover riverine flooding, others only cover storm surge or rainwater runoff. Make sure your policy clearly covers the specific water-related risks relevant to your location.

4. Don't Let Your Contents Cover Fall Behind

With $102,000 in contents cover, it's worth doing a room-by-room audit every couple of years. The cost of replacing appliances, furniture, clothing, and electronics adds up quickly — and many homeowners find they're underinsured when they actually tally it up. Don't forget to include outdoor furniture, garden equipment, and any items in storage.

---

Compare Your Own Quote

Whether you're a first-time buyer in Coomba Park or a long-time local looking to see if you're overpaying, it pays to compare. The difference between the cheapest and most expensive quotes for similar properties in NSW can run to thousands of dollars per year. Get a home insurance quote at CoverClub and see how your current premium stacks up — it only takes a few minutes and could save you significantly.