Coombabah is a quiet, well-established suburb on Queensland's Gold Coast, sitting between the Coombabah Lake Conservation Area and the broader urban spread of the northern Gold Coast corridor. It's a popular choice for families drawn to its leafy streets, proximity to schools, and easy access to the M1. For homeowners here, understanding what a fair home insurance premium looks like — and what drives the cost — can make a real difference at renewal time.

This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Coombabah, comparing it against local, state, and national benchmarks to help you make sense of what you're paying.

---

Is This Quote Fair?

The quote in question comes in at $2,387 per year (or $229/month) for a combined home and contents policy. The building is insured for $646,000 and contents for $24,000, with a $2,000 excess applying to both building and contents claims.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Within Coombabah itself, the suburb average sits at $2,858/year and the median at $2,513/year. This quote lands below both figures, placing it comfortably in the lower half of the local pricing range. In fact, it's closer to the 25th percentile of $2,173/year than to the 75th percentile of $3,366/year — meaning roughly three-quarters of comparable quotes in the area are more expensive.

That said, "fair" doesn't necessarily mean "the best available." There's still meaningful room between this quote and the cheapest end of the market, so it's always worth comparing before you commit.

---

How Coombabah Compares

To put this quote in proper context, it helps to zoom out and look at the broader insurance landscape — and the numbers are quite telling.

| Benchmark | Premium |

|---|---|

| This quote | $2,387/yr |

| Coombabah suburb average | $2,858/yr |

| Coombabah suburb median | $2,513/yr |

| Gold Coast LGA average | $8,161/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

The contrast between Coombabah's local figures and the broader Queensland averages is striking. The QLD state average of $9,129/year is more than three times this quote — a reflection of just how dramatically insurance costs vary across the state. Far North Queensland, coastal flood zones, and cyclone-prone regions all pull that state average upward significantly.

Compared to national figures, this quote also fares well. The national average of $5,347/year is more than double the premium here, while even the national median of $2,764/year sits above this quote. For a Gold Coast suburb that isn't in a cyclone risk zone, Coombabah appears to represent genuinely reasonable insurance territory.

You can explore more localised data for this suburb at the Coombabah insurance stats page. Note that the suburb sample size for this analysis is 16 quotes, so while directionally useful, the local averages should be treated as indicative rather than definitive.

---

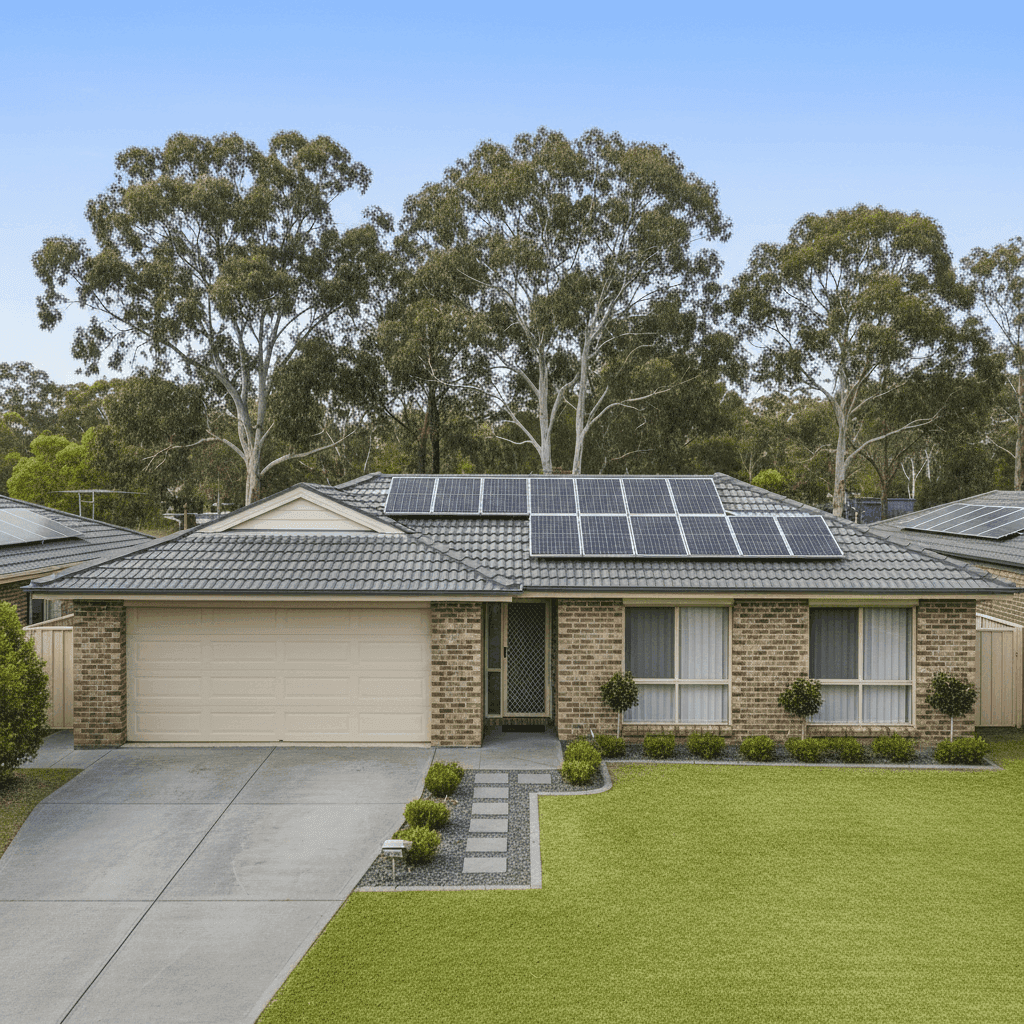

Property Features That Affect Your Premium

Several characteristics of this particular property work in the homeowner's favour from an insurance pricing perspective.

Brick Veneer Construction Brick veneer is one of the more insurer-friendly wall materials in Australia. It offers solid fire resistance and structural durability, which typically translates to lower rebuild risk compared to timber-framed or weatherboard homes. Combined with a tiled roof — another robust and fire-resistant material — this home presents a relatively low-risk profile from a construction standpoint.

Slab Foundation A concrete slab foundation is standard for Queensland homes of this era and is generally viewed positively by insurers. It reduces the risk of subfloor moisture damage and pest-related structural issues that can affect homes on stumps or piers.

Solar Panels This property has solar panels installed, which is worth flagging. Solar panels are considered a fixture of the building and are typically covered under the building sum insured — but only if they're adequately accounted for in that figure. Homeowners should confirm with their insurer that the $646,000 building sum insured includes the replacement cost of the solar system, particularly as panel and inverter costs can add several thousand dollars to a full rebuild estimate.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and, like solar panels, forms part of the building's insured value. It's one of the features that justifies a higher building sum insured relative to a home without it.

Standard Fittings and No Pool Standard-quality fittings keep the rebuild cost estimate grounded, and the absence of a pool removes a source of both liability exposure and maintenance-related claims. Both factors contribute to keeping the premium in a reasonable range.

Construction Year: 1995 At around 30 years old, this home is mature but not aged. Homes from this era were built to solid standards and are generally well-regarded by insurers, provided they've been maintained. It's worth ensuring that any significant upgrades — such as kitchen or bathroom renovations — are reflected in the building sum insured.

---

Tips for Homeowners in Coombabah

1. Review your building sum insured annually Construction costs have risen sharply in recent years across Queensland. A sum insured set even two or three years ago may no longer reflect the true cost of rebuilding your home. Use a building cost calculator or speak to a quantity surveyor to ensure you're not underinsured — especially with solar panels and ducted air conditioning adding to your replacement value.

2. Check your solar panel coverage explicitly Don't assume your solar system is covered. Ask your insurer directly whether it's included in the building sum insured, whether there are any exclusions for storm or hail damage to panels, and whether the inverter is covered as well. This is a detail that catches many homeowners off guard at claim time.

3. Compare quotes before renewing A "fair" rating means this quote is competitive, but the insurance market changes constantly. Spending 10–15 minutes comparing quotes at renewal could save you hundreds of dollars — particularly given the spread between the 25th and 75th percentile in Coombabah is nearly $1,200/year.

4. Consider your excess level strategically This policy carries a $2,000 excess on both building and contents. A higher excess generally lowers your premium, but make sure it's an amount you can genuinely access in an emergency. If $2,000 would be a stretch, it may be worth paying a slightly higher premium for a lower excess — particularly for contents claims, which tend to be smaller and more frequent.

---

Ready to Compare?

Whether you're renewing your current policy or buying cover for the first time, it pays to shop around. CoverClub makes it easy to compare home and contents insurance quotes tailored to your property in Coombabah and across Australia. Get a quote today and see how your premium stacks up.