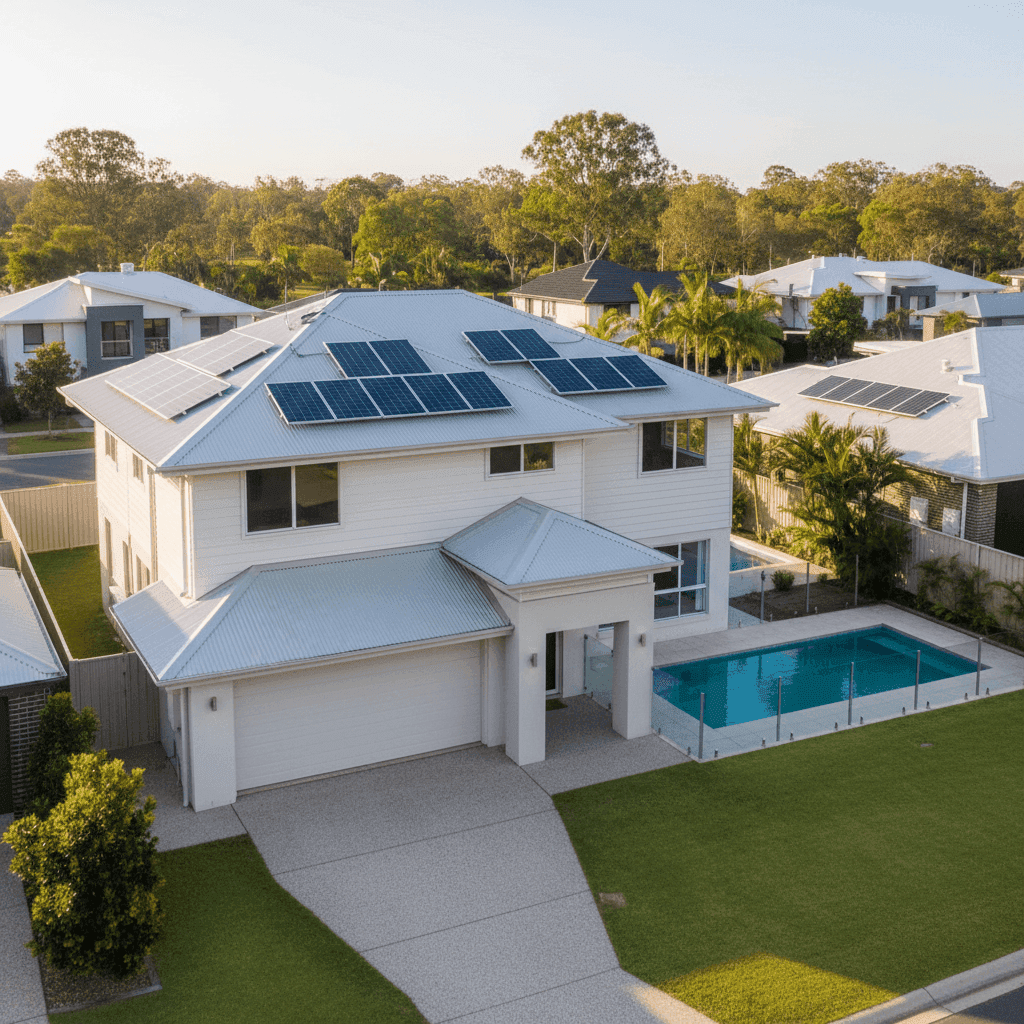

If you own a four-bedroom free standing home in Coomera, QLD 4209, you've probably noticed that home insurance isn't cheap — and a recent quote analysed through CoverClub puts that into sharp relief. This article breaks down a home and contents insurance quote for a property in this Gold Coast suburb, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $6,472 per year (or $612/month) for combined home and contents insurance, covering a building sum insured of $1,195,000 and contents valued at $98,000, each with a $1,000 excess.

Our price rating for this quote is EXPENSIVE — above average for the area.

To put that in perspective, the average home and contents premium across Coomera sits at just $1,795 per year, with a median of $1,581. Even at the 75th percentile — meaning three-quarters of quotes in the suburb are cheaper — the figure is only $2,245. This quote is nearly three times the suburb's 75th percentile, which is a significant gap worth understanding.

That said, context matters. The building sum insured of $1,195,000 is likely well above the suburb average for comparable properties, which will have a major bearing on the premium. Higher replacement values mean higher risk exposure for the insurer, and premiums scale accordingly. Still, even accounting for that, this quote warrants scrutiny — and shopping around is strongly advisable.

---

How Coomera Compares

To understand where Coomera sits in the broader insurance landscape, it helps to look at the numbers side by side.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Coomera (4209) | $1,795/yr | $1,581/yr |

| Gold Coast LGA | $8,161/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Coomera's suburb-level averages are remarkably low compared to both the Gold Coast LGA average ($8,161) and the Queensland state average ($9,129). This suggests that many properties in the 4209 postcode are insured for relatively modest sums, or that the local risk profile — flood, storm, and other hazards — is more favourable than other parts of the Gold Coast.

Second, the quote of $6,472 actually sits below both the Gold Coast LGA average and the Queensland state average, which provides some reassurance. It's also above the national average of $5,347, but not dramatically so given the high building sum insured.

You can explore suburb-level data for Coomera at the CoverClub Coomera stats page, compare it against all of Queensland, or see how it stacks up on the national insurance stats page.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct influence on what insurers charge. Here's how each one plays into the premium calculation:

Building Size & Sum Insured

At 268 sqm, this is a substantial home. The building sum insured of $1,195,000 reflects the cost to fully rebuild — not the market value — and is the single biggest driver of the premium. Larger homes with high-quality finishes cost more to reconstruct, and insurers price accordingly.

Hardiplank/Hardiflex External Walls

Fibre cement cladding like Hardiplank and Hardiflex is generally viewed favourably by insurers. It's non-combustible, resistant to rot and termites, and holds up well in Queensland's humid subtropical climate. This material is unlikely to be inflating the premium.

Steel/Colorbond Roof

Colorbond roofing is one of the most insurer-friendly roof types in Australia. It's durable, fire-resistant, and performs well in high-wind events — a real advantage in South East Queensland where storm activity is common. This should be a neutral-to-positive factor for your premium.

Concrete Slab Foundation

A slab foundation is standard for homes of this era in Queensland and is considered low-risk by most insurers. It provides stability and reduces the likelihood of subsidence or movement claims.

Swimming Pool

A pool adds to the insurable value of the property and can increase the contents or liability component of your cover. It's a feature that many Gold Coast homes share, but it does contribute to the overall premium.

Solar Panels

Solar panels are an increasingly common inclusion in Queensland homes, and most insurers now include them under building cover as a fixed fixture. However, they do add to the replacement cost of the building, which flows through to a higher sum insured and, in turn, a higher premium.

Ducted Climate Control

Ducted air conditioning is a significant fixed asset and forms part of the building's insurable value. In Queensland's climate, it's essentially a necessity — but it does add to the cost of rebuilding, which insurers factor in.

No Cyclone Risk

Coomera falls outside designated cyclone risk zones, which is a meaningful advantage. Properties in North Queensland can face dramatically higher premiums due to cyclone exposure. Being in South East Queensland without that loading keeps costs more manageable.

---

Tips for Homeowners in Coomera

Whether you're reviewing an existing policy or shopping for new cover, here are four practical steps to make sure you're getting the right protection at a fair price.

1. Verify your sum insured is accurate — but not inflated The building sum insured of $1,195,000 is the foundation of this premium. Use a reputable building cost calculator (many insurers offer one) to confirm this figure reflects realistic rebuild costs for your home's size, materials, and fittings. Over-insuring drives up premiums unnecessarily; under-insuring leaves you exposed.

2. Compare at least three quotes before renewing With only 28 quotes in the CoverClub dataset for this suburb, the market here is relatively thin. That makes it even more important to actively compare. Insurers price risk differently, and the spread between the cheapest and most expensive quotes in Coomera is wide. Get a quote through CoverClub to see what's available for your specific property.

3. Review your contents valuation annually At $98,000, the contents sum insured needs to genuinely reflect the cost of replacing everything in your home — furniture, appliances, clothing, electronics, and more. Many homeowners underestimate this figure. Do a room-by-room assessment each year, especially after major purchases.

4. Ask about discounts for security and safety features Some insurers offer premium reductions for homes with monitored alarms, deadbolts, or other security measures. It's worth asking your insurer directly — the savings can be meaningful, and the improvements benefit you beyond just the insurance discount.

---

Ready to Compare?

If this quote has you wondering whether you're paying too much, you're not alone. Home insurance premiums vary significantly between providers, even for identical properties. CoverClub makes it easy to compare home and contents insurance options tailored to your address and property details. Start a quote today at CoverClub and see what the market looks like for your Coomera home.