Nestled in the Noosa hinterland, Cooroibah is a peaceful, leafy suburb in Queensland's postcode 4565 — popular with families who want space, nature, and proximity to the Noosa region without the beachside price tag. If you own a free standing home here, you'll know that home insurance is a significant annual expense. This article breaks down a real home and contents insurance quote for a four-bedroom property in Cooroibah, analyses whether it's a fair deal, and shares practical tips to help you get better value.

---

Is This Quote Fair?

The quote in question comes in at $4,048 per year (or $395/month) for a combined home and contents policy. The building is insured for $1,057,000 and contents for $75,000, with a $1,000 excess on each.

Based on our pricing data, this quote has been rated FAIR — Around Average. That's not a bad result, but it's also not a standout deal. It sits comfortably within the typical range for the suburb, meaning you're not being overcharged, but there's likely room to find a more competitive price if you shop around.

To put it in perspective: the suburb average for Cooroibah sits at $3,933/year, meaning this quote is only about $115 above what most locals are paying on average. The suburb median, however, is notably lower at $2,996/year — which suggests that while some properties attract high premiums (pulling the average up), many homeowners in the area are securing cover for considerably less.

Explore the full Cooroibah suburb insurance statistics to see how other properties in your postcode are priced.

---

How Cooroibah Compares

One of the most striking things about this quote is how favourable it looks once you zoom out to the broader Queensland and national picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Cooroibah (suburb) | $3,933/yr | $2,996/yr |

| Queensland (state) | $9,129/yr | $3,903/yr |

| Australia (national) | $5,347/yr | $2,764/yr |

| Noosa LGA | $18,770/yr | — |

The Queensland state average of $9,129/year is more than double this quote — largely driven by high-risk coastal and cyclone-prone areas across the state. Cooroibah, notably, is not classified as a cyclone risk area, which is a meaningful factor in keeping premiums more manageable.

The national average of $5,347/year also sits well above this quote, reinforcing that Cooroibah homeowners are in a relatively favourable position compared to many Australians.

Perhaps most striking is the Noosa LGA average of $18,770/year — a figure heavily influenced by high-value beachside and flood-prone properties elsewhere in the local government area. Cooroibah's inland location and lower flood exposure help insulate homeowners from those extreme premiums.

---

Property Features That Affect Your Premium

Every home is unique, and insurers weigh up a range of physical characteristics when calculating your premium. Here's how the features of this particular property are likely influencing the cost:

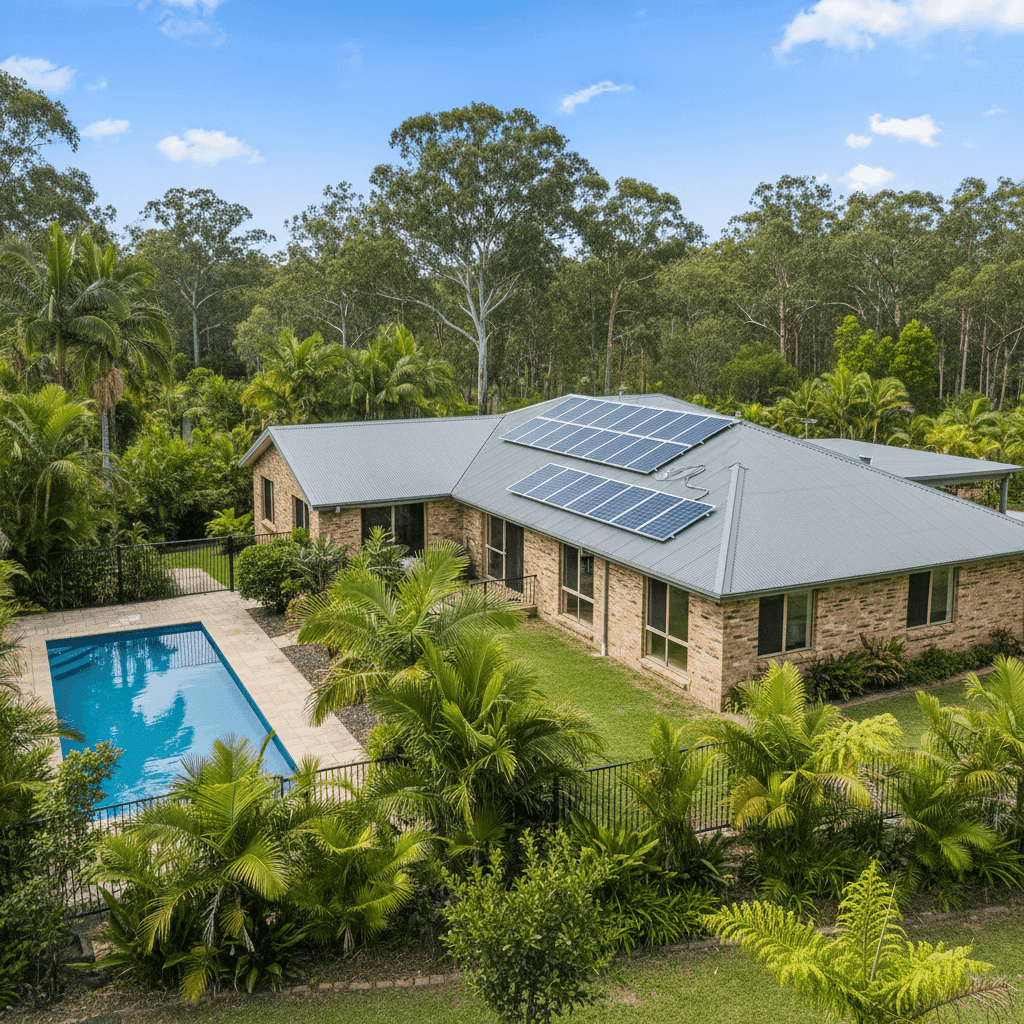

Brick Veneer Walls Brick veneer is generally viewed favourably by insurers. It offers solid fire resistance and durability, which can help moderate your premium compared to timber-clad or weatherboard homes.

Steel/Colorbond Roof Colorbond roofing is one of the most insurer-friendly roof types available. It's resistant to fire, rot, and pests, and performs well in storms — all factors that reduce the likelihood of a claim.

Slab Foundation A concrete slab foundation is low-maintenance and less susceptible to issues like subsidence or termite damage compared to older stumped homes. Insurers generally consider this a lower-risk foundation type.

Construction Year: 1987 At nearly 40 years old, this home is not brand new — but it's also not ancient. Homes from this era are typically well-constructed and meet reasonable building standards. Some insurers may factor in the age of plumbing, electrical, and roofing when pricing risk.

Above Average Fittings The above-average quality of internal fittings — think quality cabinetry, fixtures, and finishes — contributes to a higher building sum insured of $1,057,000. This is appropriate for a well-appointed 205 sqm home, but it does push the premium higher than a more modestly finished property.

Swimming Pool Pools add liability exposure and can increase your premium slightly. They also need to be accurately disclosed to ensure your policy responds correctly in the event of damage or a third-party incident.

Solar Panels Solar panels are a valuable asset that need to be covered. Many policies include them under the building sum insured, but it's worth confirming this with your insurer — particularly given the cost of modern solar systems.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and contribute to the overall replacement cost of the home. Their inclusion is one reason a higher building sum insured is appropriate here.

---

Tips for Homeowners in Cooroibah

1. Check your sum insured regularly Building costs in Queensland have risen substantially in recent years. A sum insured of $1,057,000 for a 205 sqm home with above-average fittings seems reasonable, but it's worth reviewing annually — or after any renovations — to make sure you're not underinsured. Use a building cost calculator or ask your insurer for guidance.

2. Shop the market at renewal time A "fair" rating means you're not being gouged, but you could still save hundreds by comparing quotes. With a suburb median of $2,996/year, there are clearly more competitive options available in this postcode. Get a new quote at CoverClub to see what's available for your property.

3. Confirm solar panels and pool are correctly covered Make sure your policy explicitly covers your solar panel system and that your pool and associated equipment (pump, filter, fencing) are included. Gaps in coverage for these items are a common oversight that only becomes apparent at claim time.

4. Consider your excess carefully This policy carries a $1,000 excess on both building and contents. A higher excess typically lowers your premium — but only makes sense if you can comfortably afford that outlay in the event of a claim. If cash flow allows, consider whether a $2,000 excess might reduce your annual cost meaningfully.

---

Ready to Compare?

Whether you're renewing your current policy or buying insurance for the first time, it pays to compare. CoverClub makes it easy to see real quotes for your specific property in Cooroibah — not just generic estimates. Start your comparison now at CoverClub and find out if you could be paying less for the same level of cover.