Cooroy is a charming hinterland town nestled in the Noosa Shire, about 25 kilometres inland from the Sunshine Coast. It's the kind of place where older Queenslander-style homes sit beneath tall gum trees on generous blocks — and where the character of the housing stock plays a significant role in what homeowners pay for insurance. This article takes a close look at a real home and contents insurance quote for a 3-bedroom free standing home in Cooroy (postcode 4563), unpacking whether the price stacks up and what's driving the cost.

---

Is This Quote Fair?

The quote in question comes in at $3,216 per year (or $308 per month) for a combined home and contents policy. It covers a building sum insured of $609,000 and contents valued at $71,000, with a $2,000 building excess and a $1,000 contents excess.

Our price rating for this quote is Expensive — Above Average.

To put that in context, the suburb average premium for Cooroy sits at $2,328 per year, and the median is $2,652 per year. This quote is notably above both of those benchmarks — sitting closer to the 75th percentile of $3,012 per year, and actually exceeding it. That means the vast majority of comparable quotes in this suburb come in lower.

That said, "expensive" doesn't always mean "wrong." A higher sum insured, older construction, and specific building materials can all legitimately push a premium upward. The key question is whether this particular property's characteristics justify the gap — and in this case, there are several factors that do.

---

How Cooroy Compares

It's worth zooming out to understand where Cooroy sits in the broader insurance landscape. You can explore the full data on our Cooroy suburb stats page.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,216 |

| Cooroy Suburb Average | $2,328 |

| Cooroy Suburb Median | $2,652 |

| Cooroy 75th Percentile | $3,012 |

| Gympie LGA Average | $5,581 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

The numbers tell an interesting story. While this quote looks steep compared to the Cooroy suburb median, it is actually well below the Queensland state average of $9,129 and also below the QLD state median of $3,903. Queensland homeowners — particularly those in cyclone-prone or flood-affected areas — often face some of the highest premiums in the country, which skews state-level averages significantly upward.

Compared to national figures, this quote sits below the national average of $5,347 but modestly above the national median of $2,764. For a property with the characteristics described below, that's a broadly reasonable position — though there is still room to potentially do better with the right insurer.

---

Property Features That Affect Your Premium

Several characteristics of this Cooroy home have a meaningful impact on what insurers charge. Understanding them helps explain why the premium lands where it does.

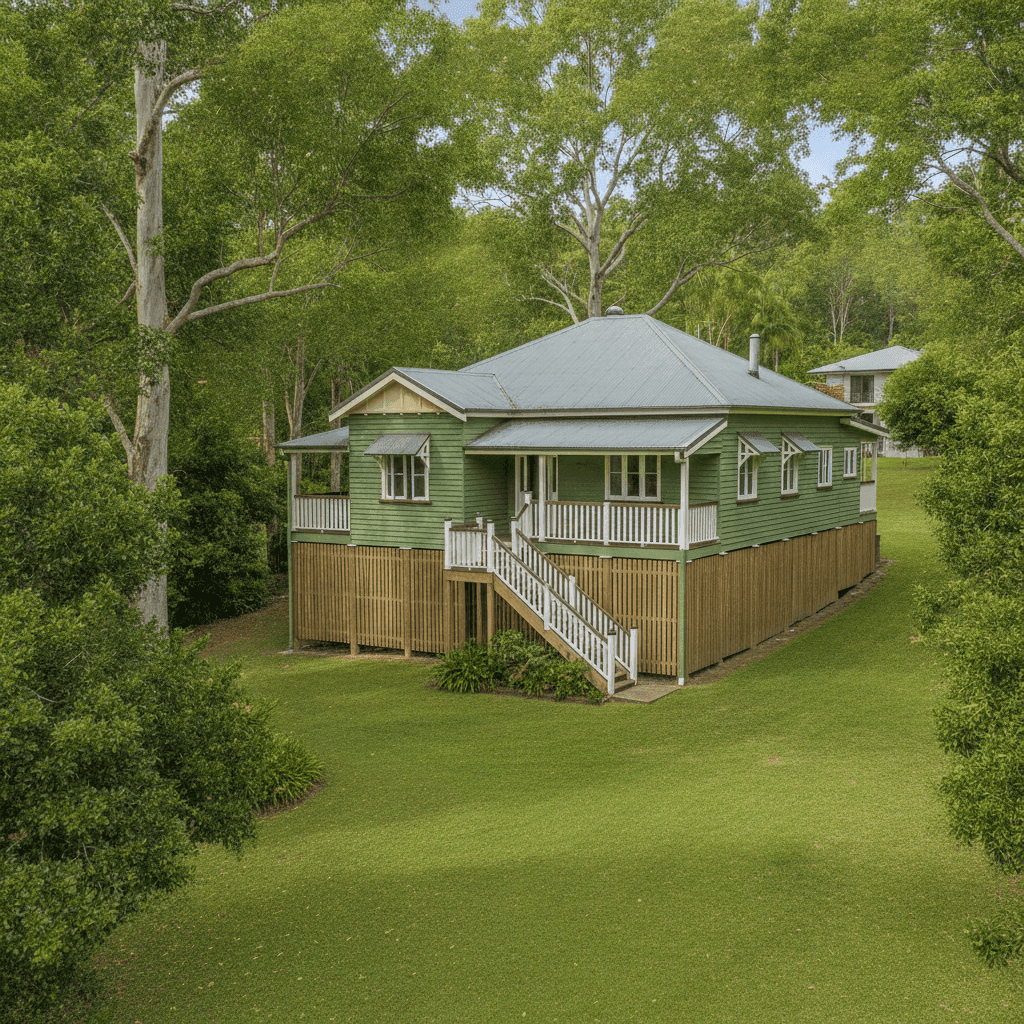

Age and Construction: Weatherboard on Stumps

Built in 1950, this home is over 70 years old. Insurers view older homes as higher risk due to ageing wiring, plumbing, and structural components that may not meet modern building standards. The weatherboard timber exterior walls add further complexity — while charming and common in older Queensland homes, timber is more susceptible to rot, termite damage, and fire than brick or fibre cement, which can push premiums higher.

The stump foundation (elevated by at least 1 metre) is a classic feature of Queenslander-era construction. On the positive side, elevation can reduce flood risk to the living areas of the home, which insurers may factor favourably. However, the underfloor space also introduces risks around subfloor maintenance and structural integrity over time.

Roof: Steel/Colorbond

The Colorbond steel roof is actually a point in this property's favour. Modern steel roofing is durable, fire-resistant, and performs well in high-wind events. Insurers generally view it more favourably than older materials like terracotta tiles or corrugated iron in poor condition.

Flooring: Timber and Laminate

Timber flooring in older homes can be a double-edged sword. Original hardwood floors are often irreplaceable and expensive to restore after water or fire damage — which can increase the cost of a claim and, by extension, the premium.

Ducted Climate Control

The presence of ducted climate control adds to the replacement value of the home's fixtures and fittings. This is a relatively significant asset that insurers account for when pricing a policy, particularly in the context of a standard-fittings property where it represents a meaningful upgrade.

Sum Insured

At $609,000, the building sum insured is substantial for a 130 sqm home. This likely reflects the cost of rebuilding an older, character-filled home with period-appropriate materials and craftsmanship — which is genuinely more expensive than constructing a modern equivalent. Ensuring your sum insured accurately reflects rebuild costs (not market value) is critical, and this figure appears to be set conservatively but responsibly.

---

Tips for Homeowners in Cooroy

1. Shop Around — Seriously

With a sample of 21 quotes in the Cooroy area showing a suburb average of $2,328, there's clear evidence that other insurers are pricing this risk lower. Use a comparison service like CoverClub to run multiple quotes side by side and see what's available for your specific property.

2. Review Your Sum Insured Carefully

Over-insuring is a common mistake. If your building sum insured is set higher than your actual rebuild cost, you're paying a premium on cover you'd never be able to claim. Consider getting a professional building valuation — many insurers offer tools to help calculate this accurately.

3. Consider Raising Your Excess

This policy carries a $2,000 building excess and $1,000 contents excess. Opting for a higher excess (where you're financially comfortable to do so) can meaningfully reduce your annual premium. Just make sure the excess level is one you could realistically afford to pay in the event of a claim.

4. Maintain the Property Proactively

For older weatherboard homes on stumps, regular maintenance is both a safety measure and an insurance consideration. Keeping the subfloor well-ventilated, addressing any timber rot promptly, and ensuring the roof is in good condition can help you avoid claims — and may support a better renewal premium over time.

---

Ready to Compare?

If you're a homeowner in Cooroy or the surrounding Noosa hinterland, it pays to regularly review your policy — especially as rebuild costs and insurer pricing shift from year to year. CoverClub makes it easy to compare home and contents quotes from multiple insurers in one place, so you can be confident you're getting the right cover at a fair price.

Get a quote today at CoverClub and see how your current premium stacks up.