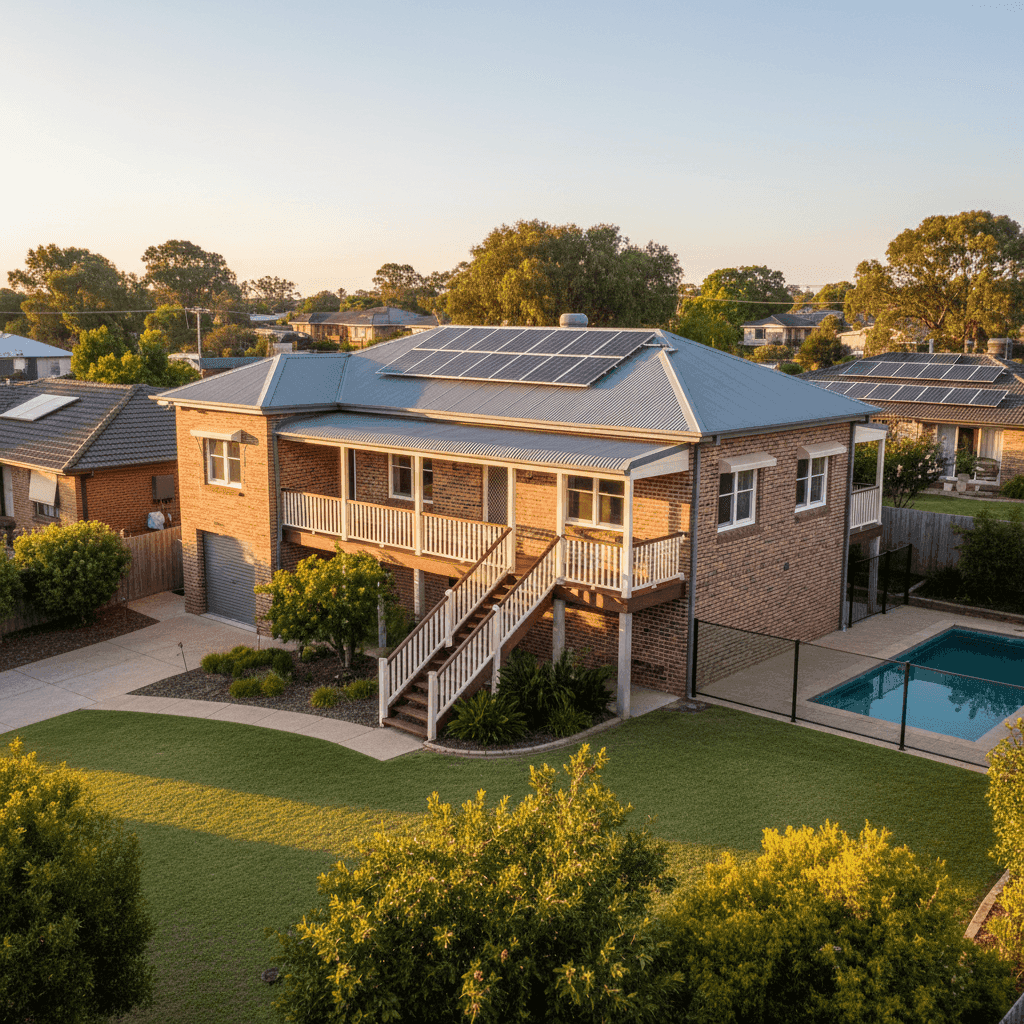

Cootamundra is a well-established regional town in the South West Slopes of New South Wales, best known as the birthplace of cricketing legend Sir Donald Bradman. It's also home to a solid mix of classic Australian residential properties — including older brick veneer homes on stumps that reflect the town's heritage character. If you own a free standing home in Cootamundra and you're wondering whether your home and contents insurance is fairly priced, this analysis breaks down a real quote and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes to $1,958 per year (or $195/month) for a combined home and contents policy — covering a building sum insured of $762,000 and $50,000 in contents. The building excess is $3,000, and the contents excess is $1,000.

Our price rating for this quote is FAIR — Around Average.

At first glance, $1,958/yr sits comfortably below the suburb average of $2,970/yr and well under the NSW state average of $3,801/yr. That's a meaningful saving — roughly $1,000 less per year than what many Cootamundra homeowners are paying. However, "fair" rather than "great" reflects the fact that this quote is still above the suburb's 25th percentile of $1,925/yr, meaning roughly a quarter of comparable quotes in the area come in even cheaper. There is room to do better, but this is by no means an overpriced policy.

It's also worth noting that the building sum insured of $762,000 is substantial for a regional property. A higher insured value naturally pushes premiums upward, so the fact that this quote remains below average is a positive sign.

---

How Cootamundra Compares

Understanding where your premium sits within the broader market is key to knowing whether you're getting value. Here's how this quote stacks up:

| Benchmark | Premium |

|---|---|

| This Quote | $1,958/yr |

| Cootamundra Suburb Average | $2,970/yr |

| Cootamundra Suburb Median | $3,035/yr |

| Cootamundra 25th Percentile | $1,925/yr |

| Cootamundra 75th Percentile | $4,020/yr |

| Junee LGA Average | $4,234/yr |

| NSW State Average | $3,801/yr |

| NSW State Median | $3,410/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

A few things stand out here. First, Cootamundra's local averages are notably lower than the NSW state average of $3,801/yr — suggesting that the postcode is generally considered lower risk by insurers compared to many other parts of the state. Coastal and flood-prone areas of NSW tend to attract significantly higher premiums, which pulls the state average upward.

Second, the Junee LGA average of $4,234/yr is considerably higher than the Cootamundra suburb figures, which may reflect a broader mix of rural and agricultural properties across the LGA that carry different risk profiles.

Compared to the national average of $2,965/yr, this quote is well below the mark — a reassuring result for Cootamundra homeowners. The wide spread between the 25th percentile ($1,925/yr) and 75th percentile ($4,020/yr) also signals that shopping around can make a significant difference in what you ultimately pay.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers assess and price the risk. Here's what's most relevant:

Age and Construction (Built 1953) At over 70 years old, this home pre-dates modern building codes. Older homes can attract higher premiums due to the increased likelihood of maintenance issues, outdated wiring, or plumbing that may not meet current standards. Brick veneer construction, however, is generally viewed favourably — it's durable, fire-resistant, and widely understood by Australian insurers.

Elevated on Stumps Being elevated by at least one metre on stumps is a double-edged sword. On the positive side, elevation can reduce flood and water damage risk — a major factor in premium calculations. On the other hand, stump foundations can be more susceptible to subsidence, pest damage (particularly termites), and structural movement over time, which some insurers factor into their pricing.

Steel/Colorbond Roof A Colorbond roof is considered a low-risk roofing material. It's lightweight, durable, resistant to fire and corrosion, and performs well in most Australian weather conditions. This likely has a neutral-to-positive effect on the premium.

Swimming Pool Pools add to the replacement cost of a property and introduce liability considerations, both of which can nudge premiums upward. Ensuring the pool is included in your building sum insured calculation is essential to avoid being underinsured.

Solar Panels Solar panels are increasingly common on Australian rooftops, but they add to the insured value of the building. It's important to confirm with your insurer that your panels are covered under the building policy — not all standard policies include them automatically, or they may be subject to specific sub-limits.

Ducted Climate Control Ducted systems are a significant fixed asset and should be factored into your building sum insured. At standard fittings quality, the overall replacement cost remains moderate, but ducted systems can be expensive to repair or replace if damaged.

---

Tips for Homeowners in Cootamundra

1. Review Your Building Sum Insured Regularly With a sum insured of $762,000, it's important to ensure this figure accurately reflects the cost to rebuild — not the market value of the property. Construction costs have risen significantly in regional NSW in recent years. Underinsurance is a common and costly mistake; many Australian homeowners are insured for far less than what a rebuild would actually cost.

2. Consider Raising Your Excess to Lower Your Premium This policy carries a $3,000 building excess, which is on the higher side. If you're comfortable self-funding smaller claims, a higher excess is a legitimate way to reduce your annual premium. Conversely, if cash flow is a concern, weigh up whether the savings justify the out-of-pocket exposure.

3. Protect Your Stumps and Sub-Floor Older homes on stumps in regional NSW can be vulnerable to termite damage and moisture-related issues. While this is primarily a maintenance concern, some insurers exclude damage caused by pests or gradual deterioration. Review your policy's exclusions carefully and invest in regular pest inspections to protect both the property and your claim eligibility.

4. Shop Around at Renewal The wide premium range in Cootamundra — from $1,925/yr at the 25th percentile to $4,020/yr at the 75th — demonstrates that insurers price this postcode very differently. Loyalty doesn't always pay in home insurance; comparing quotes at renewal can uncover meaningful savings without sacrificing cover quality.

---

Ready to Compare Home Insurance in Cootamundra?

Whether you're reviewing an existing policy or taking out cover for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see how your premium stacks up and find competitive options tailored to your property. Get a home insurance quote today and take the guesswork out of protecting one of your most valuable assets.