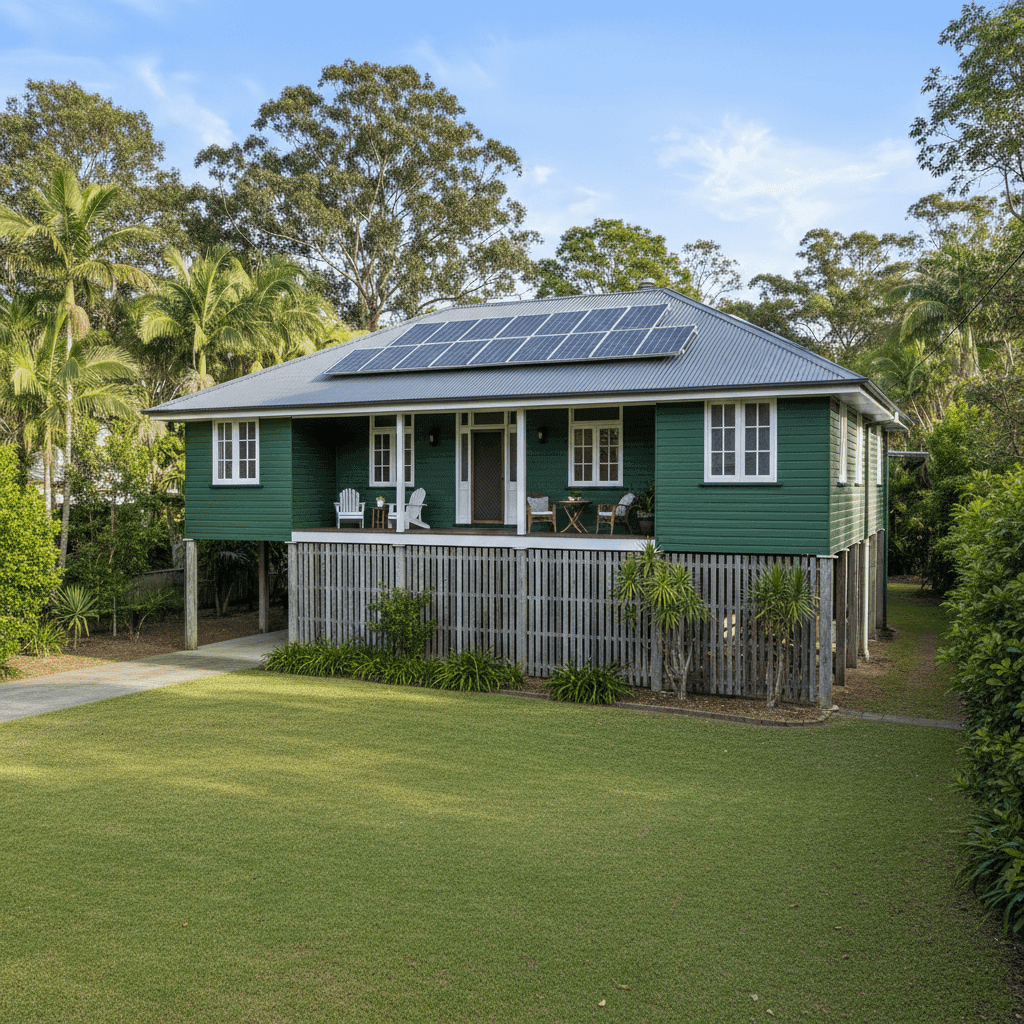

Coraki is a small riverside town in the Northern Rivers region of New South Wales, sitting at the confluence of the Richmond and Wilson rivers. It's a community with deep character — and for homeowners here, understanding the true cost of insuring a property is more important than ever. This article breaks down a real home and contents insurance quote for a four-bedroom, free-standing weatherboard home in Coraki (postcode 2471), and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $13,991 per year (or $1,259/month) for combined home and contents cover, with a building sum insured of $770,000 and contents valued at $50,000. The building excess is $2,000 and the contents excess is $1,000.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up when you look at the numbers. Based on 27 quotes collected for the Coraki area, the suburb average premium sits at $13,715/yr and the median is $12,856/yr. This quote lands just above both of those figures, which puts it squarely in the middle of the pack — not a bargain, but certainly not an outlier either.

The 25th percentile for Coraki premiums is $11,959/yr, meaning roughly a quarter of comparable properties are insured for less. The 75th percentile jumps to $17,250/yr, so there's meaningful upside risk if this property were rated more harshly by an insurer. All things considered, a premium near the suburb average is a reasonable outcome for a property with this profile.

---

How Coraki Compares

The numbers look very different once you zoom out beyond the suburb.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Coraki (2471) | $13,715/yr | $12,856/yr |

| NSW (State) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| LGA (Lismore) | $18,453/yr | — |

Coraki premiums are significantly higher than both the NSW state average of $9,528/yr and the national average of $5,347/yr. The gap between the Coraki median ($12,856) and the national median ($2,764) is particularly striking — local homeowners are paying roughly 4.6 times what the typical Australian pays to insure their home.

It's also worth noting that Coraki sits within the Lismore LGA, where the average premium is a steep $18,453/yr. That context is important: while this quote is above the Coraki suburb average, it's actually well below the broader LGA average. The Northern Rivers region has experienced significant flood events in recent years, and insurers have repriced risk in the area accordingly. Coraki itself has a well-documented flood history, which is a primary driver of elevated premiums across the postcode.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a direct bearing on how insurers assess and price the risk.

Weatherboard Timber Construction

The external walls are weatherboard wood — a construction type common in older Australian homes, particularly in regional NSW. Timber-framed and clad homes are generally considered higher risk than brick veneer or double-brick construction, as they are more susceptible to fire spread and can be costlier to repair or replace. This contributes to a higher base premium.

Age of the Home (Built 1956)

A home built in 1956 is now approaching 70 years old. Older homes often carry higher premiums because ageing plumbing, electrical wiring, and structural components present greater risk of damage or failure. Insurers factor this in when calculating replacement costs and likelihood of claims.

Elevated Foundation (Stumps, at Least 1 Metre)

The home sits on stumps and is elevated by at least one metre. In a flood-prone region like the Northern Rivers, elevation is one of the most meaningful risk mitigants a property can have. Homes raised above typical flood levels are less likely to sustain inundation damage, and this should work in the homeowner's favour when insurers assess flood risk.

Steel/Colorbond Roof

Colorbond roofing is a durable, low-maintenance option that performs well in Australian conditions. It is generally viewed favourably by insurers compared to older materials like terracotta tiles or corrugated iron, as it offers good resistance to wind and weather events.

Solar Panels

The presence of solar panels adds to the replacement value of the home, which is reflected in the building sum insured. Solar systems can also introduce specific risks — such as electrical faults or damage during storms — that insurers account for in their pricing.

Timber and Laminate Flooring

Timber and laminate floors can be expensive to repair or replace following a water or flood event, which is relevant given the flood history of the region. This is a factor that can nudge premiums upward.

---

Tips for Homeowners in Coraki

1. Review your sum insured carefully. At $770,000, the building sum insured needs to genuinely reflect the full cost of rebuilding — not the market value of the land and property. Underinsurance is a serious risk, particularly for older homes where materials and labour costs have risen sharply. Use a building cost calculator and revisit this figure annually.

2. Document your flood mitigation measures. If your home is elevated on stumps and you've taken additional steps to reduce flood risk (such as flood-rated materials, drainage improvements, or flood barriers), make sure your insurer is aware. Some insurers will adjust premiums to reflect documented mitigation, and it's worth asking the question explicitly when comparing quotes.

3. Shop around — the range is wide. The difference between the 25th and 75th percentile premiums in Coraki is more than $5,000 per year. That's a significant spread, and it means different insurers are pricing this risk very differently. Comparing multiple quotes is one of the most effective ways to ensure you're not overpaying.

4. Consider your excess settings. A $2,000 building excess and $1,000 contents excess are fairly standard, but adjusting your excess is one lever you can pull to influence your premium. Increasing your excess can reduce your annual cost — just make sure you're comfortable covering that amount out of pocket in the event of a claim.

---

Compare Home Insurance Quotes in Coraki

Whether you're a first-time buyer or a long-term Coraki resident, it pays to compare your options. Premiums in the Northern Rivers vary considerably between insurers, and a few minutes of research could save you thousands each year. Get a home insurance quote at CoverClub and see how your property stacks up — or explore the full insurance stats for Coraki and the 2471 postcode to understand what your neighbours are paying.