Crestmead is a well-established residential suburb in Logan City, sitting about 25 kilometres south of Brisbane's CBD. Known for its mix of older homes and growing family appeal, it's the kind of suburb where home insurance deserves careful attention — particularly given Queensland's reputation for severe weather events. This article analyses a recent home and contents insurance quote for a three-bedroom, two-bathroom free-standing home in Crestmead (postcode 4132), and unpacks what's driving the premium, how it compares to broader benchmarks, and what local homeowners can do to get the best value.

---

Is This Quote Fair?

The short answer: yes — and then some.

This quote came in at $1,451 per year (or $142/month) for combined home and contents cover, with a building sum insured of $454,000 and contents valued at $50,000. Our pricing engine rates this as CHEAP — below average for the area, which is a strong result for any Queensland homeowner.

To put that in perspective, the Queensland state average premium sits at $4,547 per year, with a median of $3,931. That means this quote is coming in at roughly 32% of the state average — a remarkable saving of over $3,000 annually compared to what many QLD homeowners are paying.

Even against the national average of $2,965 and the national median of $2,716, this premium is well below par in the best possible way. For a Queensland property — a state that typically attracts some of the highest insurance premiums in the country due to flood, storm, and cyclone exposure — landing a quote this competitive is genuinely noteworthy.

---

How Crestmead Compares

While suburb-level data for Crestmead isn't available in isolation, we can benchmark this quote against the Logan LGA and broader state figures. You can explore available Crestmead suburb stats here.

| Benchmark | Annual Premium |

|---|---|

| This quote | $1,451 |

| Logan LGA average | $3,411 |

| QLD state average | $4,547 |

| QLD state median | $3,931 |

| National average | $2,965 |

| National median | $2,716 |

The Logan LGA average of $3,411 is itself a useful reference point. Logan City encompasses a wide range of suburbs with varying flood and storm risk profiles, and the LGA average reflects that complexity. At $1,451, this quote is less than half the Logan LGA average — a gap that speaks to how significantly individual property characteristics can influence what you actually pay.

---

Property Features That Affect Your Premium

Several features of this particular property work together to produce a competitive premium. Here's what matters most:

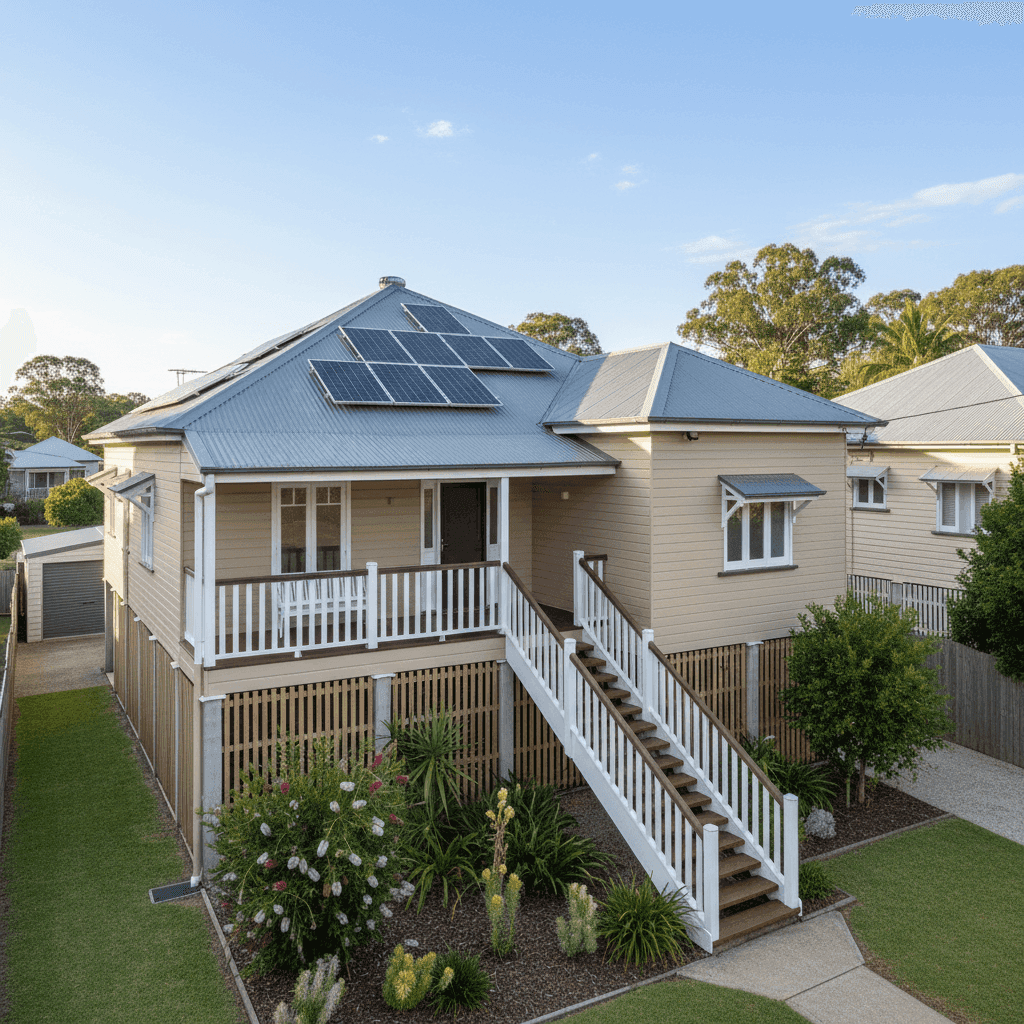

Weatherboard Timber Walls

Weatherboard construction is common in older Queensland homes, and while timber can be more susceptible to fire and moisture damage than brick veneer, insurers have well-established pricing models for it. The 1978 construction year places this home in a bracket where maintenance history and building condition can influence risk assessments.

Steel / Colorbond Roof

Colorbond roofing is generally viewed favourably by insurers. It's durable, resistant to corrosion, and performs well in high-wind events — a relevant consideration in south-east Queensland's storm season. Compared to older tile roofs, Colorbond can attract more competitive premiums.

Elevated Foundation (At Least 1 Metre)

This is likely one of the most impactful features for this property's pricing. Being elevated by at least one metre significantly reduces flood inundation risk — a major driver of insurance costs across Logan and broader south-east Queensland. Elevated homes are less likely to sustain serious damage in a flood event, which translates directly into lower premiums.

Slab Foundation with Timber/Laminate Flooring

A concrete slab foundation is structurally sound and well-suited to Queensland's climate. Timber and laminate flooring can be vulnerable to water damage, but the elevated construction mitigates much of that risk.

Solar Panels

This property has solar panels, which are typically covered under a home and contents policy as a fixed fixture. It's worth confirming with your insurer exactly how solar panels are treated — whether they're included in the building sum insured or require a separate endorsement — to avoid any gaps in cover.

No Pool, No Ducted Climate Control, Not in a Cyclone Zone

The absence of a pool removes a common liability consideration. No ducted climate control simplifies the mechanical systems covered under the policy. And sitting outside a designated cyclone risk area removes one of the most significant premium loading factors for Queensland properties.

Standard Fittings Quality

Standard-grade fittings and finishes mean rebuild costs are predictable and don't attract the premium loadings associated with high-end or custom finishes. This keeps the building sum insured — and therefore the premium — grounded.

---

Tips for Homeowners in Crestmead

Even with a competitive quote in hand, there are always ways to protect your cover and potentially improve your position at renewal.

1. Review Your Building Sum Insured Annually

Construction costs in south-east Queensland have risen significantly in recent years. The $454,000 building sum insured should be reviewed each year to ensure it reflects current rebuild costs — not just the market value of the property. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Document Your Contents Thoroughly

With $50,000 in contents cover, it's worth maintaining an up-to-date home inventory. Photograph valuables, keep receipts where possible, and store a copy of your inventory securely off-site or in the cloud. This makes any future claim significantly smoother.

3. Maintain Your Weatherboard Exterior

Timber weatherboard requires regular upkeep — painting, sealing, and checking for rot or pest damage. Neglected maintenance can not only shorten the life of the cladding but may also affect your ability to claim if damage is deemed to result from lack of upkeep. A well-maintained home is also a lower-risk home in the eyes of insurers.

4. Confirm Solar Panel Coverage

Ask your insurer specifically how your solar panel system is covered. Confirm whether the panels, inverter, and associated wiring are included in your building sum insured, and whether accidental damage or power surge scenarios are covered. As solar becomes more valuable and widespread, coverage terms are evolving — so it pays to be specific.

---

Compare Your Own Quote at CoverClub

Whether you're a Crestmead local or a homeowner anywhere in Australia, comparing quotes is the single most effective way to make sure you're not overpaying for cover. CoverClub makes it easy to see how your premium stacks up against suburb, state, and national benchmarks — in plain language, without the jargon. Get a home insurance quote today and find out where you stand.