Croydon Park is a well-established suburb in Sydney's Inner West, known for its leafy streets and mix of older character homes alongside newer builds. This analysis looks at a home and contents insurance quote for a five-bedroom, free-standing home in the 2133 postcode — and asks the question every homeowner should be asking: is this quote actually fair?

---

Is This Quote Fair?

The quote in question comes in at $21,788 per year (or $2,081/month) for combined home and contents cover, with a building sum insured of $1,080,000 and contents valued at $200,000. Our price rating for this quote is Expensive — above average for the area.

To put that in perspective: the suburb average for Croydon Park sits at just $5,302 per year, and the median is even lower at $4,295. This quote is roughly four times the suburb average — a significant gap that warrants a closer look.

That said, context matters enormously in insurance. A high sum insured, a large floor area, and certain property features can all push premiums well above what a typical home in the same suburb might attract. This isn't necessarily a sign of price gouging — but it does mean it's worth shopping around to ensure you're not overpaying for the same level of cover.

---

How Croydon Park Compares

Understanding where your premium sits relative to broader benchmarks is one of the most useful tools a homeowner has. Here's how this quote stacks up:

| Benchmark | Premium |

|---|---|

| This Quote | $21,788/yr |

| Croydon Park Suburb Average | $5,302/yr |

| Croydon Park Suburb Median | $4,295/yr |

| Croydon Park 25th Percentile | $3,108/yr |

| Croydon Park 75th Percentile | $6,482/yr |

| Inner West LGA Average | $2,955/yr |

| NSW State Average | $9,528/yr |

| NSW State Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

Even against the NSW state average of $9,528/yr, this quote is more than double. Compared to the national average of $5,347/yr, the gap is even wider. It's worth noting that NSW state averages are skewed upward by high-value properties and flood-prone areas — so the median figures are often more representative of what most homeowners actually pay.

For Croydon Park specifically, the sample of 15 quotes shows a relatively tight range, with 75% of quotes falling below $6,482/yr. This quote sits well outside that upper bound, reinforcing the "expensive" rating.

---

Property Features That Affect Your Premium

Several characteristics of this property help explain — at least in part — why this premium is elevated. Let's unpack the key factors:

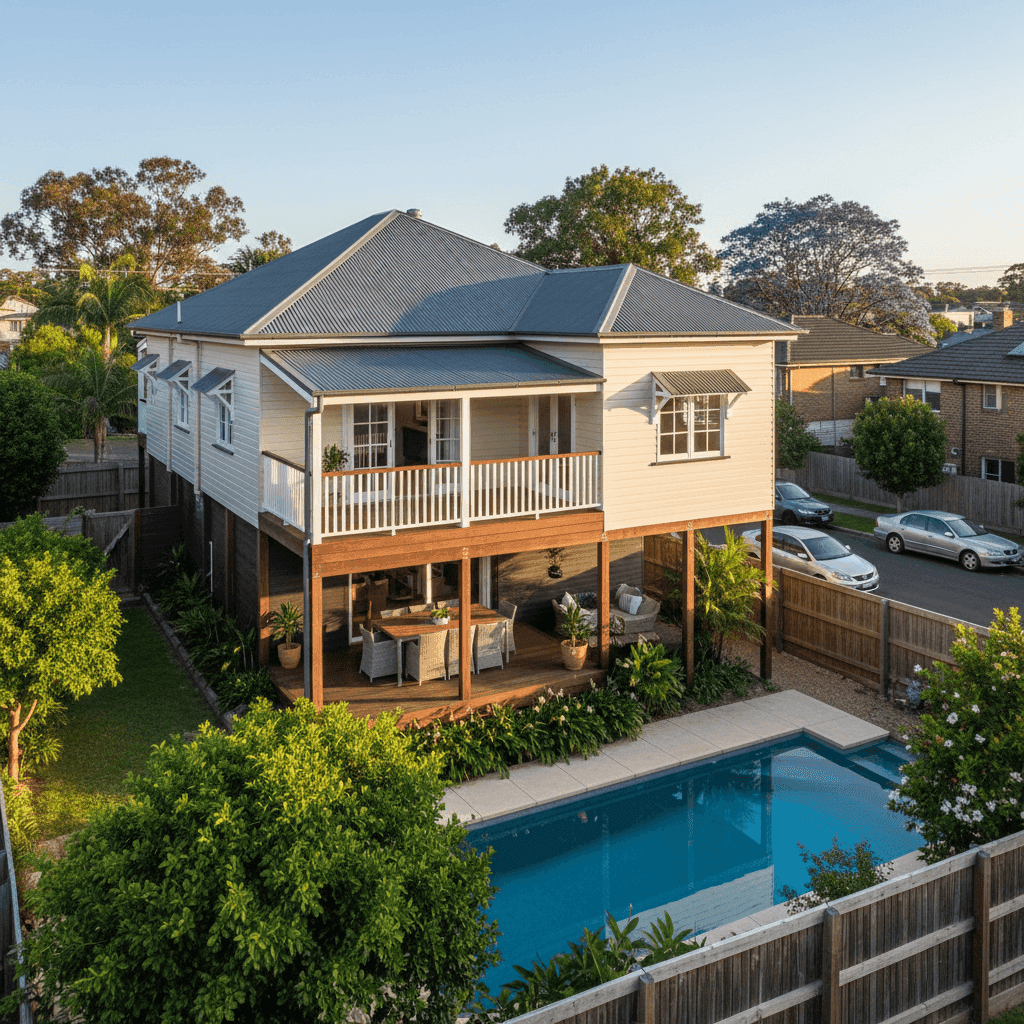

Large Building Size & High Sum Insured

At 315 sqm and a building sum insured of $1,080,000, this is a substantial home. Rebuild costs in Sydney's Inner West are among the highest in the country, and insurers price accordingly. A higher sum insured directly increases your premium, as the insurer's maximum liability is greater.

Vinyl Cladding Exterior

Vinyl cladding is generally considered a moderate-risk wall material. While it's durable and low-maintenance, some insurers apply a loading to cladded homes due to concerns around fire spread and moisture ingress over time. This can contribute to a higher base premium compared to brick veneer or full brick construction.

Elevated Foundation (Stumps)

The property is elevated by at least one metre on stump foundations — a construction style more common in Queensland but also found in parts of Sydney. Elevated homes can attract mixed treatment from insurers: on one hand, they may be less susceptible to inundation from surface water; on the other, they can be more exposed to wind and may require specific underfloor coverage. The elevated nature of this home is a notable rating factor.

Steel / Colorbond Roof

Colorbond roofing is generally viewed favourably by insurers. It's durable, fire-resistant, and performs well in severe weather. This is unlikely to be a factor driving the premium up — if anything, it may be keeping it lower than it would otherwise be.

Swimming Pool

Having a pool on the property adds to both the rebuild cost and the insurer's liability exposure. Pool surrounds, equipment, and fencing all need to be factored into the building sum insured, and some policies treat pool-related liability separately.

Ducted Climate Control

Ducted air conditioning systems are a meaningful contributor to rebuild costs. These systems are expensive to install and replace, and they're typically included in the building sum insured. This is another feature that justifies a higher sum insured — and therefore a higher premium.

No Solar Panels, No Cyclone Risk

The absence of solar panels removes one potential premium loading, and the property being outside a cyclone risk zone means it avoids the significant surcharges that apply to homes in northern Queensland and parts of WA. These are two factors working in the homeowner's favour.

---

Tips for Homeowners in Croydon Park

If you're a homeowner in Croydon Park — or anywhere in Sydney's Inner West — here are four practical steps to make sure you're getting value from your home insurance:

- Review your sum insured carefully. The single biggest driver of this premium is the $1,080,000 building sum insured. Make sure this reflects the actual cost to rebuild your home (not its market value), and use a reputable building cost calculator to verify. Over-insuring is a common and costly mistake.

- Compare quotes from multiple insurers. With a premium this far above the suburb average, it's essential to get competing quotes. Different insurers assess risk differently — especially for non-standard construction like vinyl cladding and stump foundations. Get a comparison quote at CoverClub to see what other insurers might offer for the same property.

- Ask about excess trade-offs. This policy carries a $2,000 building excess and a $1,000 contents excess. Increasing your excess — particularly on the building side — can meaningfully reduce your annual premium. If you have the financial buffer to absorb a higher out-of-pocket cost in a claim, this can be a smart way to lower your ongoing costs.

- Check what's actually included in contents cover. With $200,000 in contents cover, make sure your policy includes the items that matter most — jewellery, electronics, and portable valuables. Some policies have sub-limits on high-value items that could leave you underinsured even if the total sum looks adequate.

---

Ready to Compare?

A premium of $21,788 per year is a significant household expense. Whether you're reviewing an existing policy or shopping for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. At CoverClub, we make it easy to see how your quote stacks up — and to find better value without sacrificing cover. Start your comparison today and see what's available for your Croydon Park home.