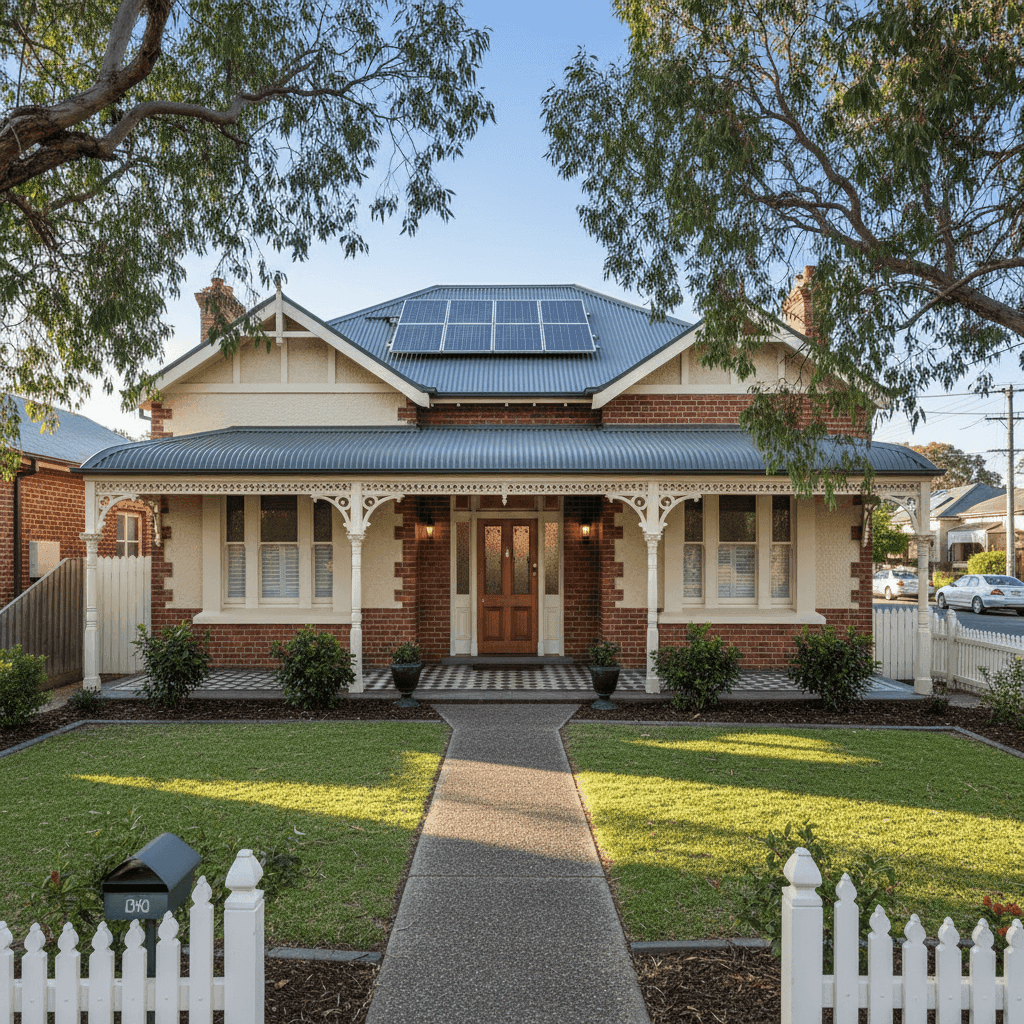

Cumberland Park is a well-established residential suburb sitting just 6 kilometres south of the Adelaide CBD, known for its leafy streets, Federation-era homes, and a strong sense of community. If you own a free standing home here, understanding what you should be paying for home and contents insurance — and why — can make a real difference to your budget and your peace of mind.

This article breaks down a real home insurance quote for a 3-bedroom, 2-bathroom free standing home in Cumberland Park (SA 5041), compares it against local, state, and national benchmarks, and highlights the property features that are likely pushing the premium in one direction or another.

---

Is This Quote Fair?

The annual premium for this property came in at $2,692 per year (or $258 per month), covering both building and contents. The building is insured for $1,350,940 and contents for $279,000, with a $1,000 excess applying to both.

Our price rating for this quote is FAIR — Around Average, which means the premium sits in a reasonable range given the property's characteristics and location. It's not a bargain, but it's not overpriced either. For a home of this age, size, and finish quality, a "fair" rating is actually a solid outcome — older homes with high-end fittings and a substantial sum insured can attract notably steeper premiums from some insurers.

That said, "fair" doesn't mean you shouldn't shop around. Even within the average band, premiums can vary by hundreds of dollars between insurers for the same property.

---

How Cumberland Park Compares

Let's put this $2,692 quote into context with the broader market:

| Benchmark | Premium |

|---|---|

| This quote | $2,692/yr |

| LGA (Mitcham) average | $2,403/yr |

| SA state average | $2,433/yr |

| SA state median | $1,679/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, this quote is only modestly above the Mitcham LGA average ($2,403) and the SA state average ($2,433) — a difference of roughly $260–$289 per year. Given the significantly higher-than-average sum insured ($1,350,940 for the building alone), that gap is quite reasonable.

Second, the quote sits comfortably below the national median of $2,764, which is a strong result. Nationally, home insurance costs have been climbing sharply in recent years, driven by extreme weather events, inflation in building costs, and reinsurance pressures. South Australia, and Adelaide's inner southern suburbs in particular, have generally fared better than coastal Queensland, northern NSW, or Western Australia's cyclone-prone regions.

You can explore Cumberland Park-specific insurance data to see how premiums in the postcode are trending over time.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on the quoted premium — some working in the homeowner's favour, others adding complexity.

Age of Construction (1910)

This is one of the most significant rating factors. A home built in 1910 is well over a century old, and insurers price older properties more cautiously. Ageing plumbing, wiring, and structural elements can increase the likelihood of claims. That said, many Federation-era homes in suburbs like Cumberland Park have been extensively renovated, and insurers will factor in the current condition where evidence is provided.

Top-of-the-Range Fittings

With fittings rated as "top of the range," the cost to repair or rebuild to the same standard is considerably higher than a standard finish. This directly supports the elevated building sum insured of $1,350,940 — and it's important that this figure accurately reflects true replacement cost, not just market value.

Timber and Laminate Flooring

Timber flooring is a common feature in older Adelaide homes and adds both aesthetic and material value. However, it can be more susceptible to water damage than tile, which insurers factor into contents and building risk assessments.

Steel/Colorbond Roof

A Colorbond roof is generally viewed favourably by insurers. It's durable, fire-resistant, and low-maintenance — a meaningful advantage over older terracotta or asbestos cement roofing that's common on homes of this era.

Solar Panels

The presence of solar panels adds a layer of complexity to the policy. Panels need to be covered under the building sum insured, and it's worth confirming with your insurer that they're explicitly included — particularly for damage caused by storms, hail, or fire.

Ducted Climate Control

Ducted systems are a significant fixed installation and should be captured in the building sum insured. They can be costly to repair or replace, so ensuring your insured amount accounts for this is important.

Slab Foundation

A concrete slab foundation is generally considered stable and low-risk by underwriters, which is a modest positive factor in the overall risk assessment.

---

Tips for Homeowners in Cumberland Park

1. Verify Your Sum Insured Reflects True Rebuild Cost

At $1,350,940, the building sum insured is substantial — but it needs to reflect the actual cost to demolish and rebuild to the same standard, including site access, council requirements, and heritage considerations that may apply to a 1910 property. Underinsurance is one of the most common and costly mistakes homeowners make. Use a professional quantity surveyor or an online building calculator to validate this figure annually.

2. Confirm Solar Panels Are Explicitly Covered

Not all policies automatically include solar panels under the building definition. Check your Product Disclosure Statement (PDS) carefully, and if there's any ambiguity, ask your insurer in writing. Storm and hail damage to panels is a real risk, even in Adelaide's relatively mild climate.

3. Shop Around at Renewal Time

A "fair" rating means you're not being overcharged — but the market is competitive, and insurers price risk differently. Even a 10–15% saving on a $2,692 premium is $270–$400 back in your pocket. Compare quotes at CoverClub before your renewal date to make sure you're still getting a competitive deal.

4. Consider Your Excess Strategically

Both the building and contents excess are set at $1,000. Opting for a higher voluntary excess (say, $2,000) can meaningfully reduce your annual premium. If you have a good claims history and a financial buffer to cover a higher out-of-pocket cost in the event of a claim, this can be a smart trade-off.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. Get a home insurance quote through CoverClub and see how your premium stacks up — it only takes a few minutes, and the savings can be significant.

Explore more SA home insurance data or dive into Cumberland Park suburb statistics to better understand what homeowners in your area are paying.