If you own a free standing home in Curra, QLD 4570, you're probably wondering whether the home insurance premium you've been quoted is reasonable — or whether you're paying more than you should. This article breaks down a real quote for a four-bedroom, two-bathroom brick veneer home in Curra, comparing it against local, state-wide, and national benchmarks so you can make a genuinely informed decision.

---

Is This Quote Fair?

The quote in question comes in at $2,218 per year (or $221/month) for combined home and contents cover, with a building sum insured of $722,000 and contents valued at $50,000. The building excess is set at $3,000, and the contents excess at $1,000.

Our price rating for this quote is FAIR — Around Average.

That might sound underwhelming, but in the context of Queensland's notoriously elevated insurance market, landing near the average is actually a reasonable outcome. Queensland consistently records some of the highest home insurance premiums in the country, driven by weather-related risks including floods, storms, and hail. Curra, located in the Gympie region of the Sunshine Coast hinterland, is no exception to the broader Queensland pricing environment — though it fares better than many coastal and far-north Queensland postcodes.

At $2,218, this quote sits below both the suburb average ($2,683/yr) and the suburb median ($2,367/yr), which is an encouraging sign. It's not in the cheapest quartile of quotes seen in the area, but it's comfortably below the 75th percentile of $3,590/yr — meaning it's better value than at least half the quotes being issued in this postcode. You can explore the full pricing picture for this postcode at the Curra suburb stats page.

---

How Curra Compares

To put this quote in proper perspective, it helps to look at the numbers side by side:

| Benchmark | Premium |

|---|---|

| This Quote | $2,218/yr |

| Curra Suburb Average | $2,683/yr |

| Curra Suburb Median | $2,367/yr |

| Fraser Coast LGA Average | $3,385/yr |

| QLD State Average | $4,547/yr |

| QLD State Median | $3,931/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

Based on 82 quotes collected for the Curra postcode.

The standout figure here is the Queensland state average of $4,547/yr — more than double this quote. That gap reflects just how much premium variation exists within Queensland itself. Coastal and cyclone-prone areas in north Queensland, as well as flood-affected river towns, push the state average significantly higher. Curra, while not immune to weather events, benefits from not being classified as a cyclone risk area, which meaningfully reduces the cost of cover.

Compared to the national average of $2,965/yr, this quote is around $747 cheaper per year — a solid saving. Even against the national median of $2,716/yr, this policy comes in below the midpoint, which is a positive result for a Queensland property. For broader Queensland context, visit the QLD state insurance stats page.

---

Property Features That Affect Your Premium

Several characteristics of this particular home work in the owner's favour when it comes to pricing.

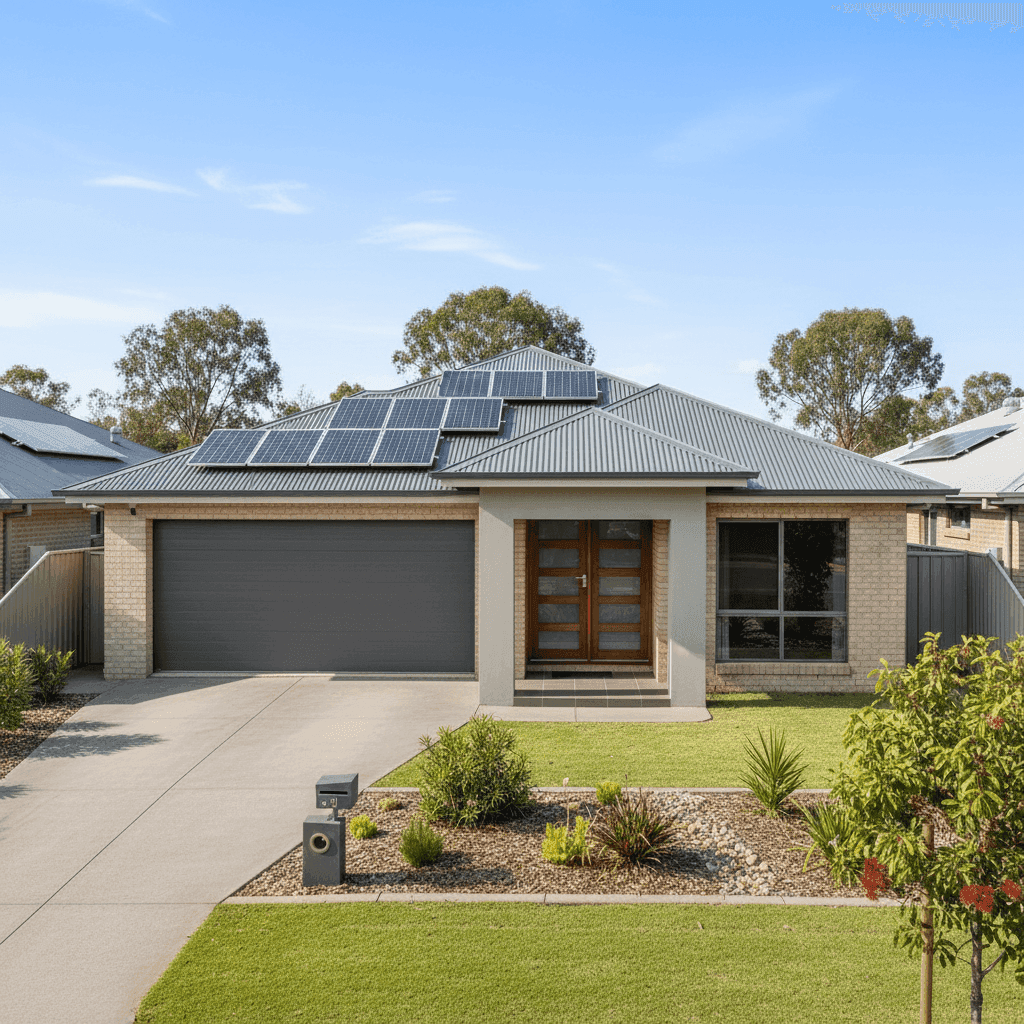

Brick veneer construction is generally well-regarded by insurers. It offers good resistance to fire and pests, and while it doesn't have the full structural resilience of double brick, it performs better in risk assessments than timber or weatherboard cladding — particularly in bushfire-adjacent areas like the Gympie hinterland.

Steel/Colorbond roofing is another positive. Colorbond is durable, low-maintenance, and performs well in high-wind events. It's less susceptible to damage from hail compared to some tile options, and insurers tend to price it favourably as a result.

The slab foundation is a standard and stable choice in Queensland's climate, reducing the risk of subsidence or movement-related claims. Combined with tile flooring, the home has a profile that suggests lower susceptibility to water damage — tiles don't warp or swell the way timber floors can.

The property was built in 2015, making it a relatively modern home. Newer builds are typically constructed to more recent building codes, which incorporate improved wind and weather resistance standards. This generally translates to lower claim frequency and, in turn, more competitive premiums.

Solar panels are present on this property. While they add value to the home and are worth insuring, they can slightly increase the replacement cost calculation, which may nudge premiums up marginally. It's worth confirming with your insurer that the solar system is explicitly covered under the building policy and that the sum insured accounts for the cost of replacement.

The absence of a pool and ducted climate control keeps the risk profile straightforward — fewer mechanical systems means fewer potential claims.

---

Tips for Homeowners in Curra

1. Review your sum insured regularly. A building sum insured of $722,000 for a 214 sqm home built in 2015 reflects current construction costs, which have risen sharply in recent years. Make sure your sum insured is based on a current rebuild cost estimate — not the market value of the property — and revisit this figure annually to avoid underinsurance.

2. Consider your excess settings carefully. A $3,000 building excess is on the higher end of the scale. While a higher excess typically reduces your annual premium, it means a significant out-of-pocket cost if you need to make a claim. Think about whether that trade-off suits your financial situation, particularly given the storm and flood risk associated with South East Queensland.

3. Confirm solar panel coverage. Solar systems are increasingly common in Queensland homes, but not all policies cover them automatically or comprehensively. Check whether your policy covers the panels for storm damage, accidental breakage, and theft — and whether the inverter and mounting hardware are included.

4. Compare quotes before renewal. Even a "fair" quote can often be improved. The insurance market is competitive, and premiums can vary significantly between providers for the same property and level of cover. Using a comparison tool at renewal time is one of the simplest ways to ensure you're not overpaying.

---

Ready to Compare?

Whether you're reviewing an existing policy or shopping for cover for the first time, CoverClub makes it easy to see how your premium stacks up. Get a home insurance quote today and find out if there's a better deal available for your Curra property.