Home insurance premiums across Queensland can vary enormously — even between neighbouring suburbs. In this article, we take a close look at a real home and contents insurance quote for a four-bedroom, free standing home in Curra, QLD 4570, and put it in context against local, state, and national benchmarks. Whether you're a homeowner in Curra or just shopping around, this analysis will help you understand what's driving the numbers.

---

Is This Quote Fair?

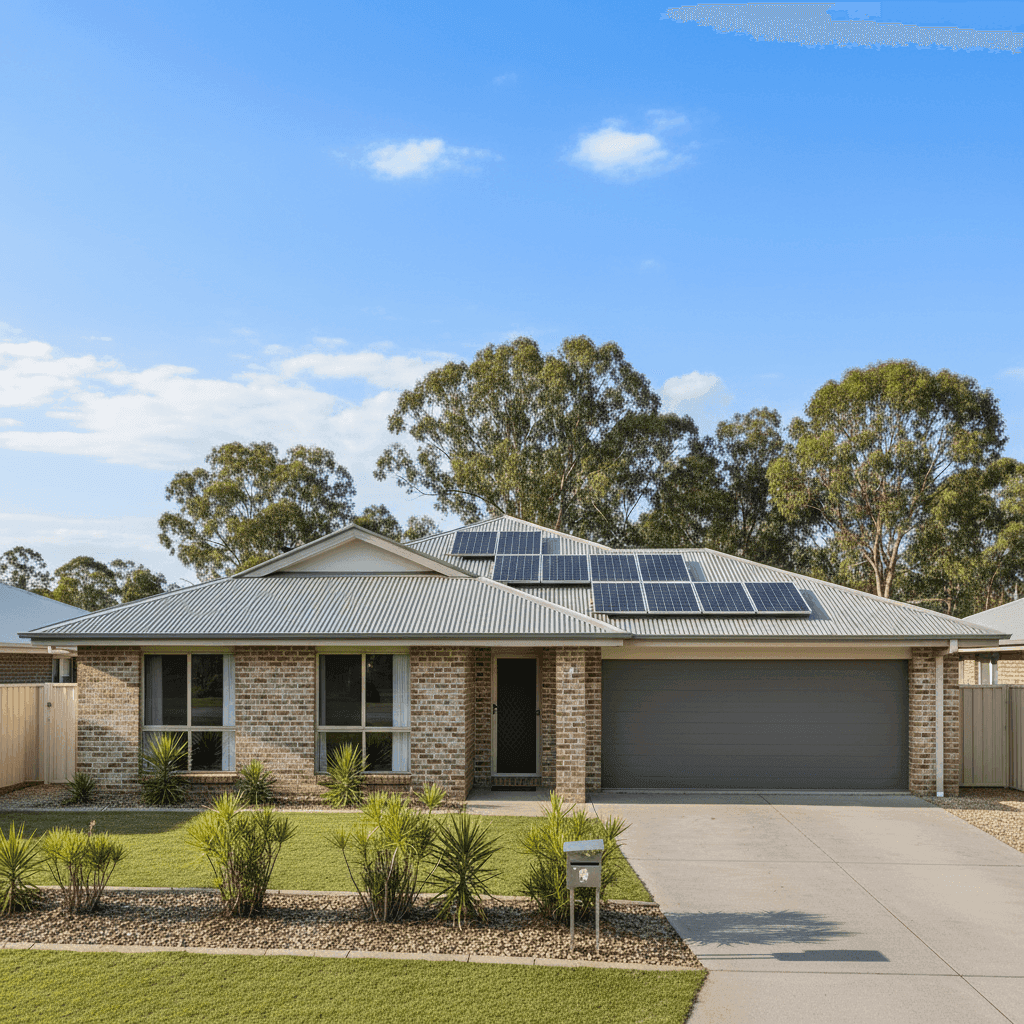

The quote in question comes in at $3,389 per year (or $318 per month) for combined home and contents cover. The building is insured for $442,000 and contents for $154,000, with a $1,000 building excess and $500 contents excess.

Our price rating for this quote is FAIR — Around Average.

That rating reflects where the premium sits relative to comparable properties in the area. Based on data from 82 quotes collected for Curra and surrounds, the suburb average sits at $2,683 per year and the median at $2,367. At $3,389, this quote lands above both of those figures — but it's still comfortably within the suburb's 75th percentile of $3,590. In other words, roughly 75% of similar properties in the area are paying the same or less, but only just.

The "fair" rating acknowledges that while this isn't the cheapest quote on the market, it's not out of step with what Curra homeowners are typically paying for a property of this size and specification. The higher-than-median price is likely influenced by the sum insured levels, the inclusion of contents cover, and certain property features — more on those below.

---

How Curra Compares

One of the most useful things you can do when evaluating any insurance quote is to zoom out and look at the broader picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Curra (QLD 4570) | $2,683/yr | $2,367/yr |

| Fraser Coast LGA | $3,385/yr | — |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out here. First, Queensland's average home insurance premium of $4,547 per year is dramatically higher than the national average of $2,965 — a gap of more than $1,500. This reflects the elevated risk profile of much of the Sunshine State, where cyclones, flooding, and storm damage are significant concerns for insurers.

Curra itself, however, sits well below the Queensland average. At a suburb median of $2,367, it's actually tracking below the national median of $2,716 — which is a relatively favourable position for a regional Queensland property. The Fraser Coast LGA average of $3,385 closely mirrors this particular quote, suggesting the pricing is broadly consistent with what's typical for the region.

For a deeper dive into local pricing trends, visit the Curra suburb stats page.

---

Property Features That Affect Your Premium

Every property is different, and insurers weigh up a range of factors when calculating your premium. Here's how the features of this particular home are likely influencing the cost:

Brick Veneer Walls & Steel/Colorbond Roof Brick veneer construction is generally viewed favourably by insurers — it's durable, fire-resistant, and holds up well in storms. A Colorbond steel roof is similarly well-regarded in Australia, offering strong resistance to wind and rain. Together, these materials tend to attract more competitive premiums compared to, say, weatherboard or fibrous cement cladding.

Slab Foundation & Tile Flooring A concrete slab foundation is the standard for Queensland homes of this era and presents minimal additional risk. Tiled flooring is low-maintenance and resilient, which also works in the homeowner's favour from an insurer's perspective.

Solar Panels This property has solar panels installed, which adds a modest amount to the replacement cost of the building. Insurers typically include solar systems under the building sum insured, so it's important to ensure the $442,000 figure accounts for the cost of replacing the panels in the event of total loss or storm damage.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and is generally covered under building insurance. Like solar, it contributes to the overall rebuild cost and can nudge premiums slightly higher — though the impact is usually modest.

Built in 1990 At around 35 years old, this home is neither brand new nor particularly aged. Properties from this era are generally straightforward to insure, though some insurers may factor in the potential for older plumbing or electrical systems when pricing risk.

No Pool, No Cyclone Risk Zone The absence of a pool removes a common liability risk, and the property falling outside a designated cyclone risk area is a meaningful premium advantage for a Queensland home. Many properties further north carry significant cyclone loading in their premiums.

---

Tips for Homeowners in Curra

1. Review your sum insured regularly Building costs have risen sharply in recent years. The $442,000 sum insured should reflect the full cost to rebuild — not the market value of the property. Use a building cost calculator or speak with a local builder to make sure you're not underinsured.

2. Check that your solar system is covered Not all policies automatically cover solar panels, or they may apply separate sub-limits. Confirm with your insurer that your panels and inverter are included in the building sum insured and that the coverage amount is adequate.

3. Consider your contents figure carefully $154,000 in contents cover is a reasonable starting point for a four-bedroom home, but it's easy to underestimate. Do a room-by-room inventory — don't forget electronics, appliances, clothing, and outdoor furniture — to make sure you're not left short after a claim.

4. Compare quotes before renewing Loyalty doesn't always pay in insurance. Even if your current premium feels fair, it's worth getting a few competing quotes at renewal time. Premiums can shift significantly between insurers for the same property, and the savings can be substantial.

---

Ready to Compare?

If you're a homeowner in Curra or anywhere in Queensland, CoverClub makes it easy to see how your current premium stacks up. Get a home insurance quote today and compare your options side by side — it only takes a few minutes and could save you hundreds.