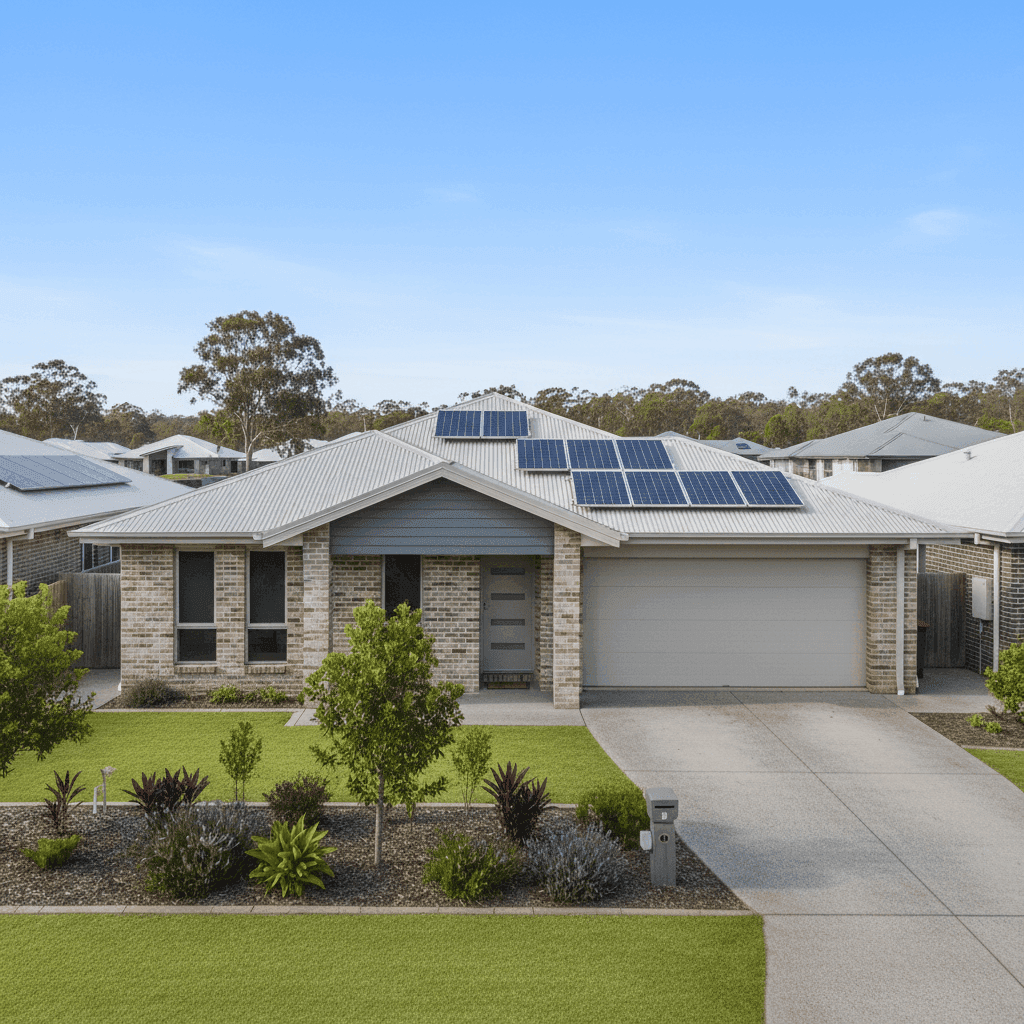

Curra is a quiet rural locality in Queensland's Fraser Coast region, sitting inland from the Sunshine Coast hinterland. For owners of a free standing home in this area, understanding what drives your insurance premium — and whether you're paying a fair price — can make a real difference to your household budget. This analysis breaks down a recent home and contents insurance quote for a 3-bedroom, 2-bathroom property in Curra (QLD 4570) and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $5,112 per year (or $483/month), covering both building (sum insured: $622,000) and contents ($50,000), each with a $1,000 excess. Our price rating for this quote is Expensive — Above Average.

To put that in perspective, the suburb average premium in Curra sits at just $2,683/year, and the median is even lower at $2,367/year. This quote is nearly double the local median, which is a significant gap worth investigating.

That said, it's important to note that the Queensland state average for home and contents insurance is $4,547/year, and the Fraser Coast LGA average is even higher at $4,810/year. Viewed through that lens, this quote is only modestly above the broader regional norm — suggesting that while Curra's own suburb-level pricing tends to run lower, the wider LGA and state context reflects elevated risk across the region.

The bottom line: this quote is on the expensive side relative to your immediate neighbours, but not wildly out of step with what many Queenslanders are paying. Whether it's the right price for your property depends on the specific features and risk factors at play.

---

How Curra Compares

Here's a snapshot of where this $5,112 quote sits across different benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Curra (QLD 4570) | $2,683/yr | $2,367/yr |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

| Fraser Coast LGA | $4,810/yr | — |

(Based on 82 quotes sampled for the Curra suburb. See full [Curra suburb insurance stats](https://coverclub.com.au/stats/QLD/4570/curra), [Queensland state stats](https://coverclub.com.au/stats/QLD), and [national insurance stats](https://coverclub.com.au/stats/national).)

A few things stand out from this data:

- Curra's local averages are well below the state average, suggesting that many properties in the suburb attract relatively modest premiums — likely due to lower replacement values, simpler construction, or favourable risk profiles.

- Queensland as a whole is significantly more expensive than the national average, with the state median ($3,931) sitting 45% above the national median ($2,716). This reflects the elevated natural hazard risk across much of Queensland, including flood, storm, and cyclone exposure.

- The Fraser Coast LGA average ($4,810) is the highest benchmark in this comparison, reinforcing that the broader region carries meaningful insurance risk — even if individual suburbs like Curra can sometimes come in lower.

This quote, at $5,112, sits above all of these benchmarks except the Fraser Coast LGA average, which it narrowly exceeds.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining when thinking about what's driving the premium.

Brick veneer construction with a Colorbond roof is generally considered a moderate-to-good risk profile by insurers. Brick veneer offers solid fire resistance and structural integrity, while steel/Colorbond roofing is durable and performs well in high-wind events — a meaningful consideration in Queensland. These features typically work in the homeowner's favour.

Slab foundation is standard for Queensland homes built in the 2000s and 2010s and doesn't generally attract loading from insurers. Similarly, tile flooring is a durable, low-maintenance choice that poses minimal additional risk.

Built in 2014, this home is relatively modern, which usually means it was constructed to more recent building codes — including improved cyclone tie-down standards and flood-resilient design requirements that were progressively introduced across Queensland following major weather events. This can be a positive factor for insurers.

Solar panels are worth flagging. While they add value to the home, solar systems can increase the cost of a claim if damaged — particularly in hail or storm events — and some insurers load premiums accordingly. It's worth confirming with your insurer exactly how your solar system is covered under your policy.

The building sum insured of $622,000 for a 169 sqm home works out to roughly $3,680/sqm — which is on the higher end of the rebuild cost spectrum. If this figure has been set conservatively (or has grown with construction cost inflation), it will directly influence the premium. It's worth periodically reviewing your sum insured to ensure it reflects current rebuild costs rather than an inflated estimate.

---

Tips for Homeowners in Curra

1. Shop around — especially if you're above the suburb median With 82 quotes sampled in Curra, there's clearly a wide range of pricing in this market (the 25th percentile sits at $1,792/yr, while the 75th is $3,590/yr). If your premium is well above the local median, it's a strong signal to compare alternatives. Get a new quote at CoverClub to see what other insurers are offering for your property.

2. Review your building sum insured Construction costs have risen sharply across Australia in recent years, but that doesn't mean your sum insured needs to be set at maximum — it needs to be accurate. An inflated sum insured leads to a higher premium without providing meaningful additional protection. Use a building cost calculator or speak with a quantity surveyor to check your figure.

3. Ask about your solar panel coverage Solar panels are becoming increasingly common on Queensland homes, but coverage varies considerably between policies. Some insurers include them automatically under building cover; others require a separate endorsement. Make sure you understand exactly what's covered — and what the excess would be — if your panels were damaged in a storm or hail event.

4. Consider a higher excess to reduce your premium Both the building and contents excess on this policy are set at $1,000. Increasing your excess — say, to $2,000 or $2,500 — can meaningfully reduce your annual premium. Just make sure the saving is worth the additional out-of-pocket cost if you do need to make a claim.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for the first time, it pays to compare. CoverClub makes it easy to see how your quote stacks up against real data from your suburb, your state, and across Australia. Start comparing home insurance quotes today and make sure you're not paying more than you need to for the cover your home deserves.