Currumbin Valley is one of South East Queensland's most picturesque pockets — a lush, hinterland retreat tucked behind the Gold Coast's famous coastline. It's a sought-after location for families and lifestyle seekers alike, but like any Queensland property, the right home insurance cover is essential. This article breaks down a real home and contents insurance quote for a four-bedroom free standing home in Currumbin Valley (postcode 4223), helping you understand what's driving the price and how it stacks up against local and national benchmarks.

---

Is This Quote Fair?

The annual premium for this quote comes in at $4,301 per year (or $386/month), covering a building sum insured of $858,000 and contents valued at $63,000, each with a $1,000 excess.

Our independent price rating for this quote is Fair — Around Average, which is a reasonable outcome for a property of this type and size in the area. It's not the cheapest on the market, but it's not overpriced either. For homeowners who haven't reviewed their policy in a while, this kind of benchmark check is exactly the sort of reality test that can either provide reassurance — or reveal an opportunity to save.

The "fair" rating reflects the fact that this premium sits comfortably within the typical range for comparable properties in the suburb, without being a standout deal. Given the property's characteristics (more on those below), there's logic behind the pricing.

---

How Currumbin Valley Compares

To put the $4,301 annual premium in context, here's how it measures up across different comparison points:

| Benchmark | Average | Median |

|---|---|---|

| Currumbin Valley (4223) | $4,034/yr | $3,814/yr |

| Queensland (State) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here.

Versus the suburb: This quote is modestly above the Currumbin Valley suburb average of $4,034 and the median of $3,814 — but it falls well within the interquartile range (25th percentile: $2,607 / 75th percentile: $5,050), based on a sample of 55 quotes. That means roughly half of comparable quotes in the area fall between $2,607 and $5,050, and this one sits in the upper-middle of that band. Given the property's size (235 sqm) and high building sum insured ($858,000), that's not surprising.

Versus Queensland: The Queensland state average of $9,129/year looks alarming at first glance — but the median of $3,903 tells a more balanced story. Queensland's average is heavily skewed by high-risk coastal and cyclone-prone areas in North Queensland, where premiums can be eye-watering. Currumbin Valley is not a designated cyclone risk area, which is a meaningful advantage. This property's premium is very close to the state median, which is a positive signal.

Versus national figures: Compared to the national average of $5,347, this quote comes in below — another encouraging sign. The national median of $2,764 is lower, but again, that figure includes smaller properties, lower sum-insured policies, and lower-risk locations across the country.

The Gold Coast LGA average of $8,161/year further underscores that this property is performing well relative to its broader region.

---

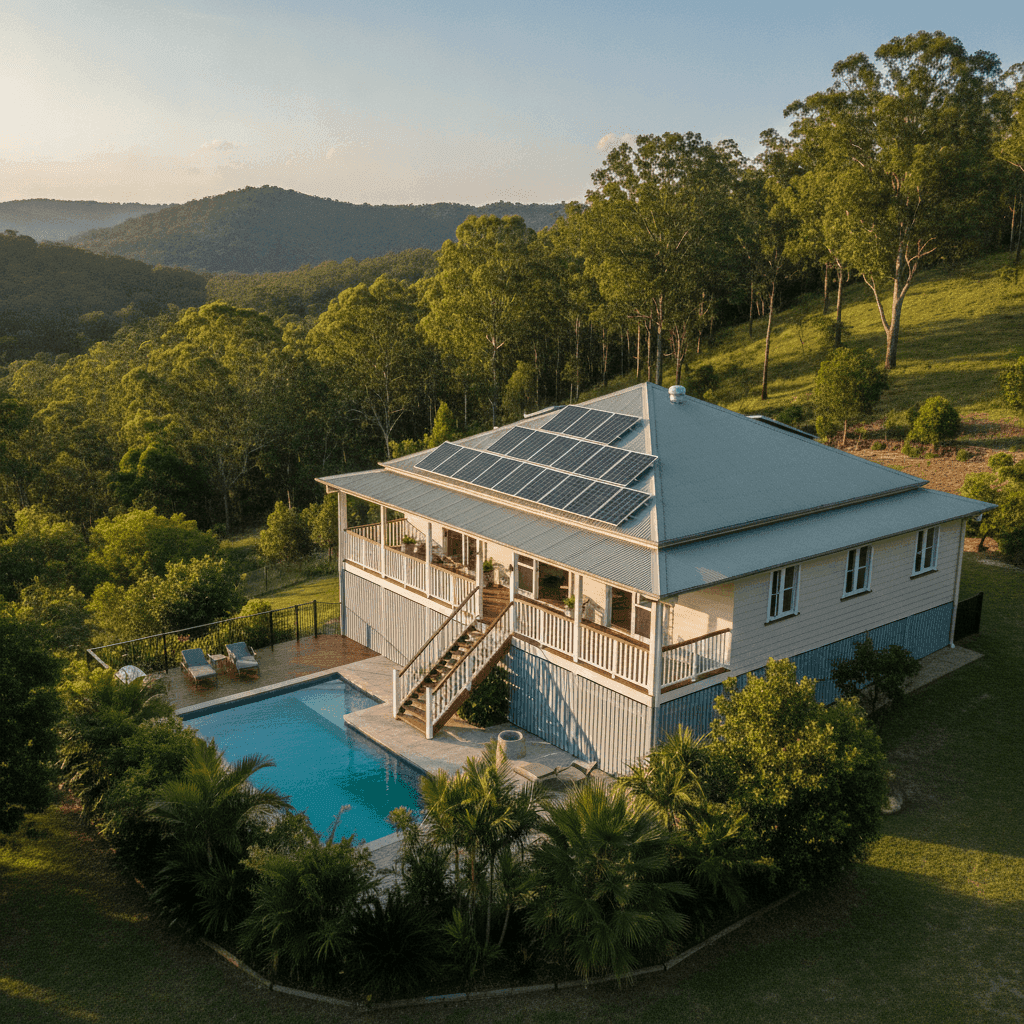

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated. Here's what matters most:

Weatherboard timber walls are a key factor. While timber homes have a warm aesthetic and are common in Queensland's older housing stock, they carry a higher fire risk than brick veneer or full brick construction. Insurers typically price this in, as timber is more susceptible to both fire spread and moisture damage over time.

Steel/Colorbond roof is generally viewed favourably by insurers. Colorbond is durable, low-maintenance, and performs well in high-wind and hail events — all relevant considerations in South East Queensland's storm season.

Slab foundation is considered a stable, lower-risk foundation type compared to stumped or suspended timber floors. This works in the property's favour from an underwriting perspective.

Timber/laminate flooring adds to the overall replacement cost of the home, which flows through into the building sum insured. High-quality flooring is more expensive to reinstate after a flood or fire event.

The swimming pool adds a modest amount to the contents or structural value that needs to be covered, and may also introduce some liability considerations depending on the policy.

Solar panels are an increasingly common feature and most insurers now include them under building cover — but it's worth confirming this explicitly in your policy documents, as some treat them as optional extras.

Ducted climate control is a significant fixed asset that contributes to the building's replacement cost. Ducted systems are expensive to replace and are typically captured in the building sum insured.

Slight elevation (less than 1m) provides a minor buffer against surface water ingress, though it's not a significant flood mitigation factor at this height. Properties elevated more substantially (e.g., traditional Queenslanders on high stumps) tend to benefit more from reduced flood risk pricing.

The 1989 construction year places this home in an era before many modern building codes, which can mean older wiring, plumbing, and materials. Some insurers factor this into their risk assessment.

---

Tips for Homeowners in Currumbin Valley

1. Review your building sum insured annually Construction costs have risen sharply in recent years. A $858,000 sum insured may have been accurate when the policy was first taken out, but it's worth cross-checking against current rebuild cost estimates — not the market value of the land and home. Underinsurance is one of the most common and costly mistakes Australian homeowners make.

2. Confirm solar panels are explicitly covered Ask your insurer directly whether your solar panel system is included under your building cover, and for how much. Some policies have sub-limits or exclude panels installed after the original policy was written. Given the cost of modern solar systems, this is worth clarifying in writing.

3. Shop around at renewal time A "fair" rating means you're not being ripped off — but it also means there may be better value available. Insurance premiums can vary significantly between providers for the same property. Using a comparison platform like CoverClub at renewal time takes minutes and could reveal meaningful savings.

4. Consider your excess strategically Both the building and contents excess on this policy are set at $1,000. Increasing your excess (e.g., to $2,500 or $5,000) can reduce your annual premium noticeably. If you have sufficient savings to cover a higher out-of-pocket amount in the event of a claim, this can be a smart way to lower ongoing costs.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new property, CoverClub makes it easy to see how your quote stacks up. Get a home insurance quote today and compare options tailored to your property — so you can make a confident, informed decision about protecting one of your most valuable assets.