Currumbin Waters is one of the Gold Coast's most sought-after residential pockets — a quiet, leafy suburb sitting just inland from the coast, with a strong mix of established family homes and a relaxed lifestyle that draws buyers from across Queensland and beyond. If you own a free standing home here, understanding what you should be paying for home and contents insurance is an important part of protecting one of your biggest assets.

This article breaks down a real home insurance quote for a four-bedroom, two-bathroom free standing home in Currumbin Waters (postcode 4223), and puts the numbers in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium in this quote comes in at $2,838 per year (or $272 per month), covering a building sum insured of $600,000 and contents valued at $35,000, with a $500 excess on both building and contents. Our pricing analysis rates this quote as Fair — Around Average.

That rating reflects a premium that sits comfortably within the normal range for the suburb, without being a standout bargain or an obvious overpay. For homeowners who haven't shopped around in a while, a "fair" rating is actually a meaningful result — many Australians are paying well above what comparable properties attract simply because they haven't compared recently.

At $2,838, this quote lands just above the suburb's 25th percentile of $2,733 per year, meaning roughly three-quarters of comparable quotes in the area come in higher. That's a solid position to be in, though it still leaves room to potentially find a more competitive price with a broader comparison.

---

How Currumbin Waters Compares

To put this premium in proper context, it helps to look at how Currumbin Waters insurance costs stack up against broader benchmarks.

| Benchmark | Premium |

|---|---|

| This quote | $2,838/yr |

| Suburb average | $3,540/yr |

| Suburb median | $3,674/yr |

| Suburb 25th percentile | $2,733/yr |

| Suburb 75th percentile | $4,253/yr |

| Gold Coast LGA average | $8,161/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, the Queensland state average of $9,129 per year looks alarming at first glance — but it's heavily skewed by high-risk properties in cyclone-prone and flood-affected regions across the state. The state median of $3,903 is a much more representative figure, and this quote sits comfortably below it.

Similarly, the Gold Coast LGA average of $8,161 reflects the wide diversity of properties across the region, from low-lying flood zones to elevated hinterland acreage. Currumbin Waters, with its relatively benign risk profile, tends to attract more moderate premiums than many Gold Coast postcodes.

Compared to the national median of $2,764, this quote is only marginally higher — a reassuring sign that the homeowner isn't being penalised unfairly for their location.

---

Property Features That Affect Your Premium

Every home insurance quote is shaped by the specific characteristics of the property. Here's how the features of this particular home influence its risk profile and, in turn, its premium.

Concrete external walls are generally viewed favourably by insurers. Concrete construction is resilient to fire, resistant to termite damage, and holds up well in high-wind events — all factors that reduce the likelihood of a large claim.

Steel/Colorbond roofing is another positive. Colorbond is a staple of Australian residential construction for good reason — it's durable, lightweight, and performs well in storms. Insurers typically regard it as lower risk than older materials like terracotta tiles or fibrous cement sheeting.

Stump foundations are common in Queensland homes of this era, and while they allow for good airflow and can be beneficial in flood-prone areas, they do introduce some considerations around subfloor access and structural movement over time. Insurers are generally comfortable with this construction type in established suburbs like Currumbin Waters.

Timber and laminate flooring can be a factor in contents and building claims — particularly in the event of water damage — but this is a standard flooring type across the region and unlikely to significantly elevate the premium.

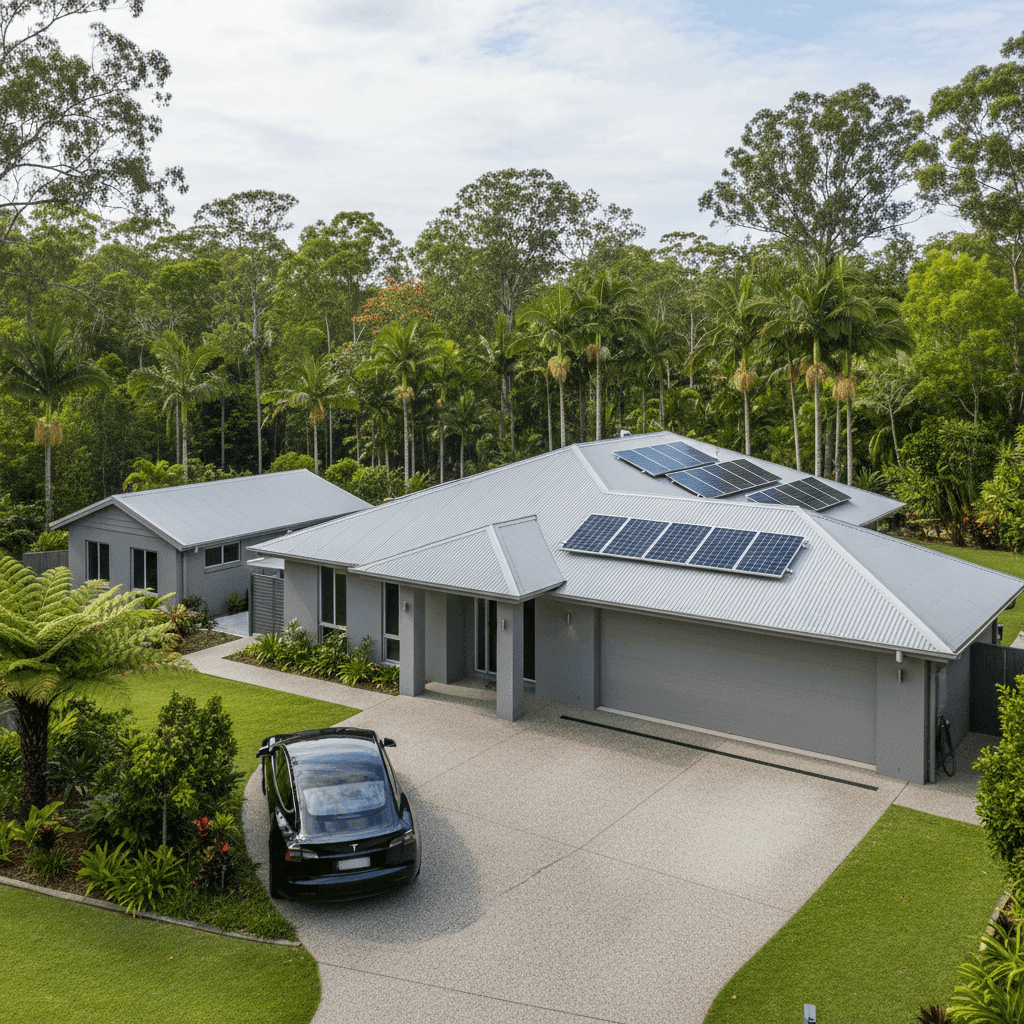

Solar panels are worth noting. While they add value to the property, they also represent an insurable asset. It's important to confirm with your insurer whether solar panels are covered under the building sum insured, and whether the $600,000 building cover adequately accounts for their replacement cost.

The granny flat is a significant feature that deserves attention. A secondary dwelling on the property increases the overall replacement cost and can affect the terms of your cover. Homeowners should ensure their insurer is aware of the granny flat and that it's explicitly included in the building sum insured — underinsurance is a real risk when secondary structures aren't properly accounted for.

The property is not located in a cyclone risk area, which is a meaningful premium advantage in Queensland. Cyclone-rated properties — particularly in North Queensland — can face dramatically higher premiums, so Currumbin Waters homeowners benefit from a more moderate risk classification.

---

Tips for Homeowners in Currumbin Waters

1. Review your building sum insured carefully At $600,000, the building sum insured needs to cover full rebuilding costs — not just the market value of the home. With a 235 sqm home, a granny flat, and solar panels to account for, it's worth using a building cost calculator or speaking with a quantity surveyor to confirm this figure is adequate. Underinsurance remains one of the most common and costly mistakes Australian homeowners make.

2. Confirm your granny flat is covered Not all policies automatically extend full cover to secondary dwellings. Check your Product Disclosure Statement (PDS) to understand exactly what's included, and consider whether the granny flat's contents (if tenanted or used as accommodation) require a separate policy or endorsement.

3. Compare quotes at renewal — every year A "fair" rating means this premium is reasonable, but the insurance market shifts constantly. Loyalty doesn't always pay — insurers regularly offer more competitive rates to new customers than to long-standing ones. Setting a reminder to compare quotes before each renewal could save hundreds of dollars annually.

4. Check your contents sum insured reflects reality At $35,000, the contents value is on the modest side for a four-bedroom home. It's easy to underestimate the cumulative value of furniture, appliances, clothing, electronics, and personal items. A quick home inventory — room by room — often reveals that contents are worth significantly more than the insured amount.

---

Ready to Compare?

Whether you're renewing soon or simply curious about what else is out there, comparing quotes is the fastest way to know if you're getting genuine value. Get a home insurance quote at CoverClub and see how your current premium stacks up — it takes just a few minutes and could make a real difference at renewal time.