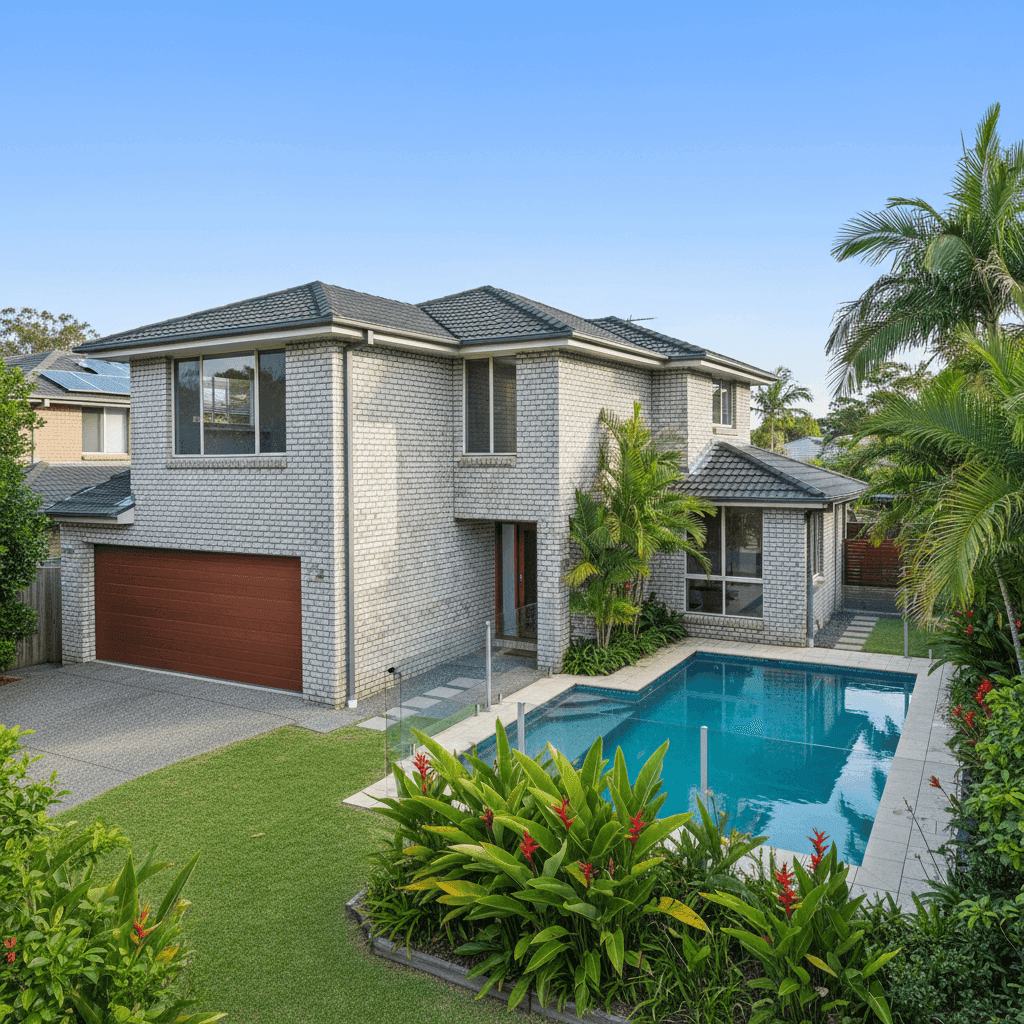

Currumbin Waters is one of the Gold Coast's most sought-after pockets — a leafy, canal-laced suburb that sits just minutes from the beach and the hinterland. It's also a suburb where home insurance costs can vary considerably depending on your property's characteristics and the insurer you choose. In this article, we break down a real home and contents insurance quote for a three-bedroom, free-standing home in Currumbin Waters (postcode 4223) and put it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $1,970 per year (or $189 per month), covering both building and contents with a sum insured of $608,000 for the building and $50,000 for contents. Both the building and contents excess are set at $2,000.

Our pricing model rates this quote as CHEAP — below average for the area. That's a meaningful finding. When a premium lands below the suburb's 25th percentile of $2,733 per year, it suggests the policyholder is getting a genuinely competitive deal — not just marginally better than average, but well into the lower tier of what's available in this postcode.

For homeowners who've been auto-renewed on the same policy for a few years, this kind of comparison is a useful wake-up call: the market can offer significantly better value than what many people are currently paying.

---

How Currumbin Waters Compares

To understand what "cheap" really means here, it helps to look at the numbers side by side.

| Benchmark | Premium |

|---|---|

| This quote | $1,970/yr |

| Suburb average (4223) | $3,540/yr |

| Suburb median (4223) | $3,674/yr |

| Suburb 25th percentile | $2,733/yr |

| Suburb 75th percentile | $4,253/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Gold Coast LGA average | $8,161/yr |

Based on 23 quotes collected for the Currumbin Waters area.

The quote at $1,970 sits $1,570 below the suburb average and $1,933 below the suburb median — a substantial saving. Compared to the broader Gold Coast LGA average of $8,161 and the Queensland state average of $9,129, the difference is even more striking, though it's worth noting those figures are heavily influenced by high-risk flood and cyclone zones elsewhere in the state.

Even against the national median of $2,764, this quote holds up well — coming in nearly $800 cheaper.

You can explore more pricing data for this postcode on our Currumbin Waters insurance stats page, or browse the broader Queensland insurance statistics and national home insurance data for additional context.

---

Property Features That Affect Your Premium

Several characteristics of this property likely contribute to its competitive premium. Understanding these factors can help you make smarter decisions when reviewing your own cover.

Brick Veneer Construction

Brick veneer external walls are generally viewed favourably by insurers. They offer solid fire resistance and structural durability compared to lightweight cladding or weatherboard, which can translate to lower rebuild risk assessments — and often, lower premiums.

Tiled Roof

A tile roof, particularly on a home built in 1996, is considered a reliable and low-maintenance roofing material. Tiles perform well in the Gold Coast's subtropical climate, resisting UV degradation and moderate wind events. Insurers typically price tiled roofs more competitively than older corrugated iron or flat membrane roofs.

Concrete Slab Foundation

A slab foundation is standard for Queensland homes of this era and is generally well-regarded by insurers. It reduces the risk of subfloor moisture issues and pest-related structural damage that can affect homes on stumps or piers.

No Cyclone Risk Designation

Currumbin Waters falls outside Queensland's designated cyclone risk zone — a significant factor. Properties in cyclone-rated areas (particularly Far North Queensland) routinely attract much higher premiums due to the additional structural requirements and claim exposure. Being outside that zone is a genuine pricing advantage.

Swimming Pool

The presence of a pool adds a modest layer of liability and maintenance considerations for insurers, but for a standard residential property on the Gold Coast, a pool is common enough that it rarely causes a dramatic premium spike. It's worth ensuring your policy specifically covers pool-related liability and any associated structures like fencing or equipment.

Ducted Climate Control

Ducted air conditioning systems represent a meaningful contents and building asset. At $50,000 in contents cover, it's worth confirming whether the ducted system is covered under building or contents — typically, permanently installed systems fall under building cover, which is included here at $608,000.

Standard Fittings

With standard-grade fittings throughout, the rebuild cost estimate of $608,000 for 139 square metres reflects a reasonable per-square-metre rate for the Gold Coast region. Homes with high-end finishes, custom joinery, or imported materials often require a higher sum insured to avoid being underinsured in the event of a total loss.

---

Tips for Homeowners in Currumbin Waters

Whether you're reviewing your existing policy or shopping for a new one, here are a few practical steps worth taking.

1. Check your sum insured annually Construction costs on the Gold Coast have risen considerably over recent years. A sum insured set several years ago may no longer reflect the true cost of rebuilding your home. Use a building cost calculator or speak with a quantity surveyor to verify your figure — underinsurance is one of the most common and costly mistakes homeowners make.

2. Consider a higher excess to reduce your premium Both the building and contents excess on this quote sit at $2,000. If you have a solid emergency fund and are unlikely to make small claims, opting for a higher excess (say, $2,500–$5,000) can meaningfully reduce your annual premium. Just make sure the excess is an amount you could genuinely afford to pay at claim time.

3. Review your contents sum insured carefully $50,000 in contents cover is a common starting point, but it can underestimate the true value of furniture, appliances, clothing, and electronics in a family home. Take an inventory — many people are surprised by how quickly the total adds up. Underinsuring your contents means you'll bear the shortfall yourself after a claim.

4. Compare quotes at renewal — every year The fact that this quote came in well below the suburb average is a reminder that loyalty doesn't always pay in insurance. Premiums can shift significantly between providers and between policy years. Shopping around annually — or using a comparison tool — is one of the simplest ways to avoid overpaying.

---

Ready to See What You Could Pay?

If you own a home in Currumbin Waters or anywhere on the Gold Coast, it's worth knowing where your premium sits relative to the market. CoverClub makes it easy to get a home insurance quote and compare your options — so you can feel confident you're not paying more than you need to.