Daisy Hill is a leafy, established suburb in Brisbane's south-east corridor, popular with families drawn to its quiet streets, proximity to Daisy Hill Conservation Park, and good school catchments. But owning a freestanding home here — particularly one built in the 1980s — comes with its own set of insurance considerations. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom property in Daisy Hill QLD 4127, and puts the numbers into context so you can make a more informed decision about your own cover.

---

Is This Quote Fair?

The quote in question comes in at $5,158 per year (or $451 per month) for combined home and contents insurance, with a building sum insured of $612,000 and contents valued at $33,000. The building excess is $2,000 and the contents excess is $1,000.

Our pricing analysis rates this quote as Expensive — above average for the area.

To understand why, it helps to look at the benchmarks. The suburb average premium in Daisy Hill sits at $3,919 per year, while the median is considerably lower at $2,428. This quote lands well above both figures, suggesting there are meaningful factors pushing the premium up beyond what a typical Daisy Hill homeowner might pay. That said, every property is different, and as we'll explore below, several features of this particular home justify some of the additional cost.

---

How Daisy Hill Compares

Putting this $5,158 quote into a broader context reveals some interesting contrasts.

| Benchmark | Premium |

|---|---|

| This quote | $5,158 / yr |

| Daisy Hill suburb average | $3,919 / yr |

| Daisy Hill suburb median | $2,428 / yr |

| QLD state average | $9,129 / yr |

| QLD state median | $3,903 / yr |

| National average | $5,347 / yr |

| National median | $2,764 / yr |

| Brisbane LGA average | $16,277 / yr |

A few things stand out here. First, while this quote is above the local suburb average, it sits below both the Queensland state average and the national average — which is worth noting. Queensland premiums are notoriously high due to the state's exposure to cyclones, flooding, and severe storms, which pushes the state average up to $9,129. Daisy Hill, located in Brisbane's outer south-east, is not classified as a cyclone risk area, which helps keep premiums comparatively moderate.

The Brisbane LGA average of $16,277 is strikingly high, but this figure is heavily skewed by high-value riverfront and flood-prone properties elsewhere in the LGA. Daisy Hill's own median of $2,428 reflects a more typical suburban risk profile.

You can explore more local pricing data on the Daisy Hill suburb stats page, compare it against Queensland-wide insurance trends, or benchmark against national home insurance averages.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the above-average premium. Understanding them can help you have a more informed conversation with your insurer.

Fibro Asbestos External Walls

This is arguably the most significant risk factor for this property. Homes built before the mid-1980s in Australia frequently used fibro sheeting containing asbestos. While the material is stable when undamaged, any repair or rebuild following an insured event — fire, storm, or impact — requires specialist asbestos removal and safe disposal, which dramatically increases the cost of claims. Insurers price this risk into the premium, and it's one of the primary reasons this quote sits above the suburb average.

Construction Year: 1984

A home built in 1984 is now over 40 years old. Older homes can carry higher risk due to ageing electrical wiring, plumbing, and structural components. Insurers factor in the increased likelihood of maintenance-related claims and the higher cost of sourcing period-appropriate materials for repairs.

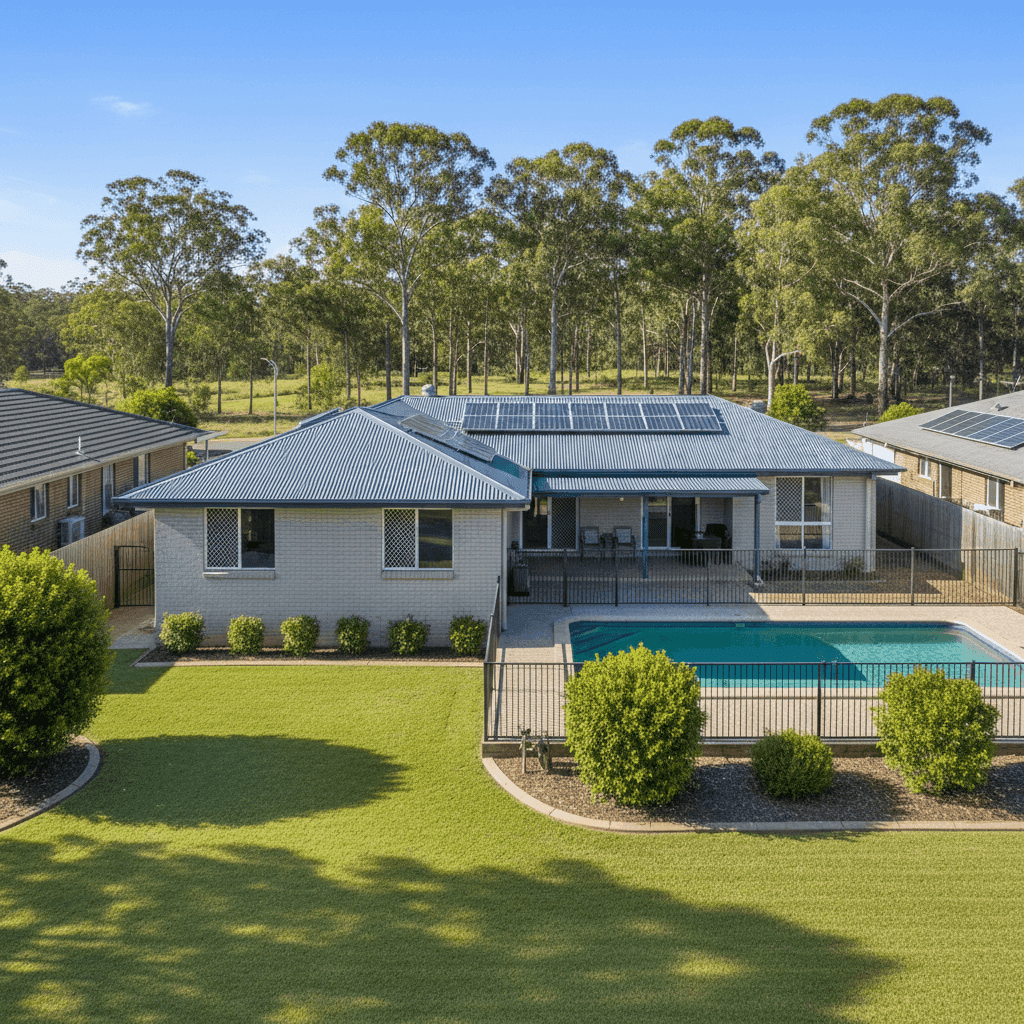

Building Sum Insured: $612,000

At 214 square metres, the building sum insured of $612,000 works out to roughly $2,860 per square metre — a reasonable figure for a full rebuild including demolition, professional fees, and the added complexity of asbestos removal. A higher sum insured naturally means a higher premium, but underinsuring a property like this could leave you significantly out of pocket after a major loss.

Swimming Pool

Pools add both value and liability to a property. From an insurance perspective, they increase the replacement cost of the home and introduce additional liability exposure. Most insurers include pool coverage within the building policy, but it does contribute to a higher overall premium.

Solar Panels

Solar panels are increasingly common on Australian rooftops, but they do add to the insured value of the home. Panels are vulnerable to hail, storm damage, and theft, and replacing a full system can cost thousands. This is reflected in the premium calculation.

Timber and Laminate Flooring

While not as significant a risk factor as the wall construction, timber and laminate floors are more expensive to repair or replace than concrete or tile, particularly in the event of water damage. This adds modestly to the overall risk profile.

---

Tips for Homeowners in Daisy Hill

If you're looking to manage your home insurance costs without compromising on protection, here are four practical steps worth considering.

1. Get multiple quotes and compare carefully The spread of premiums in Daisy Hill is wide — from $1,216 at the 25th percentile to $3,321 at the 75th percentile. That's a significant range, and it means shopping around can genuinely pay off. Use a comparison tool like CoverClub to see multiple options side by side.

2. Review your sum insured annually Building costs in south-east Queensland have risen sharply in recent years. Make sure your sum insured reflects current rebuild costs — not the figure you set when you first took out the policy. An independent quantity surveyor can provide a formal assessment if you're unsure.

3. Ask about asbestos-specific policy terms Not all policies handle asbestos the same way. Some may include asbestos removal as part of the standard rebuild cover, while others treat it as an exclusion or a sub-limit. Read the Product Disclosure Statement carefully and ask your insurer directly how they handle asbestos-containing materials in a claim scenario.

4. Consider your excess settings This policy carries a $2,000 building excess and a $1,000 contents excess. Opting for a higher voluntary excess can reduce your annual premium — but only if you're confident you could comfortably cover that amount out of pocket in the event of a claim. It's a trade-off worth modelling based on your financial situation.

---

Compare Your Options with CoverClub

Whether you're renewing your existing policy or shopping for cover on a new purchase, it pays to know where your quote sits relative to the market. CoverClub makes it easy to compare home and contents insurance quotes for properties across Australia, with suburb-level pricing data to give you real context. Start your comparison today and make sure you're getting the right cover at a fair price.