If you own a free standing home in Daisy Hill, QLD 4127, you've probably wondered whether you're paying a fair price for home insurance — or leaving money on the table. This article breaks down a real home and contents insurance quote for a three-bedroom brick veneer home in the suburb, comparing it against local, state, and national benchmarks so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $1,899 per year (or roughly $182 per month) for combined home and contents cover, with a building sum insured of $400,000 and contents valued at $70,000. Both the building and contents excess are set at $1,000.

Our pricing engine has rated this quote as Fair — Around Average, which is a reasonable outcome for a property of this type and age. It sits comfortably within the middle of the market, neither a standout bargain nor an overpriced outlier.

To put that in perspective:

- The suburb's median premium for Daisy Hill is $2,428/yr — meaning this quote is roughly $529 cheaper than what half of comparable properties in the area are paying.

- The suburb average sits at $3,919/yr, which is significantly higher, pulled upward by properties with elevated risk profiles or higher sums insured.

- At the 25th percentile, the cheapest quarter of Daisy Hill quotes come in around $1,216/yr — so there is room to go lower, though that would likely reflect less coverage or different property characteristics.

In short, this quote is a reasonable result — below both the suburb average and median — but not at the very bottom of the market. Homeowners who shop around may find slightly better pricing, but they should ensure they're comparing like-for-like coverage.

---

How Daisy Hill Compares

Daisy Hill sits within the Brisbane LGA, which carries a strikingly high average premium of $16,277/yr. That figure is heavily skewed by high-value properties and flood-exposed areas across greater Brisbane, so it's not particularly useful as a direct comparison — but it does highlight just how variable premiums can be across the region.

Looking at broader benchmarks from CoverClub's national insurance data:

| Benchmark | Premium |

|---|---|

| This quote | $1,899/yr |

| Daisy Hill suburb median | $2,428/yr |

| Daisy Hill suburb average | $3,919/yr |

| QLD state median | $3,903/yr |

| QLD state average | $9,129/yr |

| National median | $2,764/yr |

| National average | $5,347/yr |

This quote beats the QLD state median by over $2,000 per year and sits well below the national median of $2,764/yr. That's a meaningful saving, particularly given Queensland's reputation for higher-than-average insurance costs driven by extreme weather events, flooding, and storm activity.

You can explore more localised data on the Daisy Hill suburb stats page or review Queensland-wide insurance trends to see how different postcodes stack up.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence where its premium lands — for better or worse.

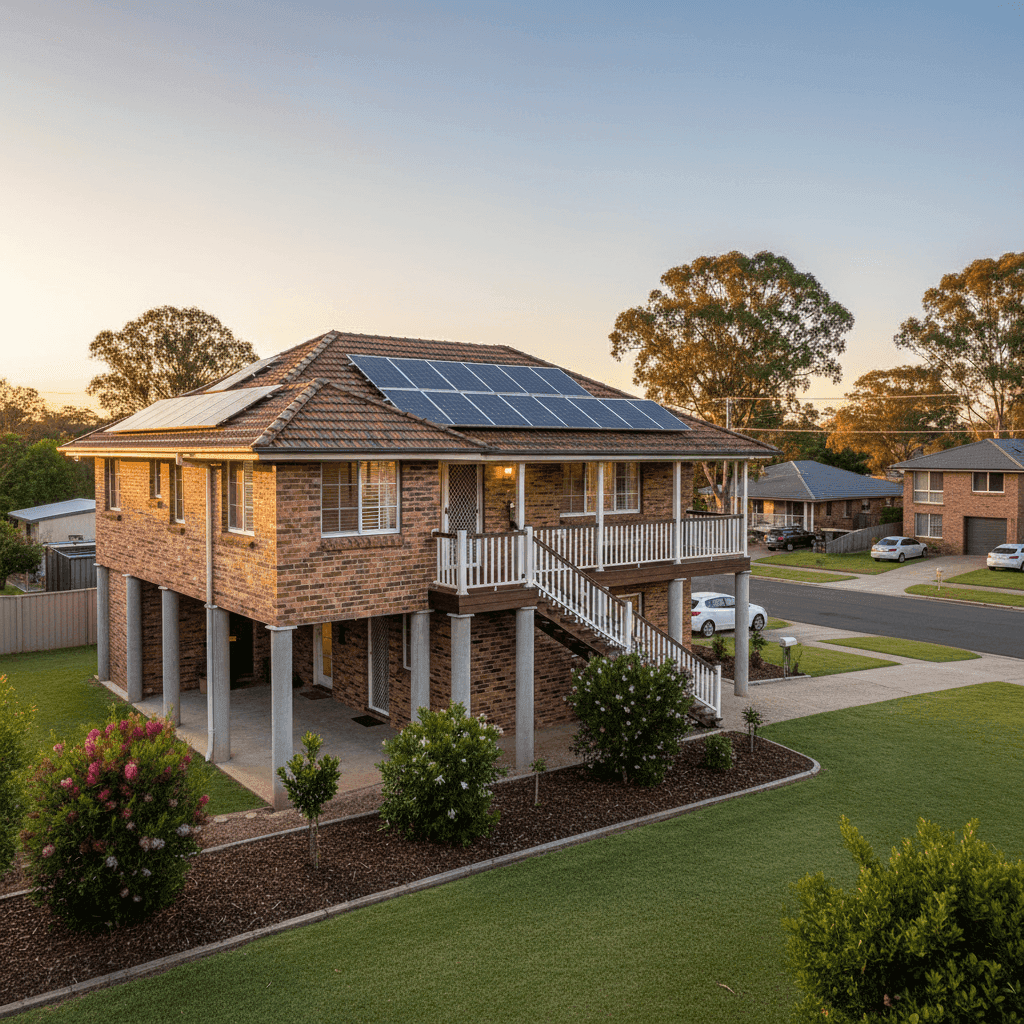

Brick Veneer Walls & Tiled Roof Brick veneer construction paired with a tiled roof is generally viewed favourably by insurers. These materials are considered durable and relatively fire-resistant, which can help keep premiums competitive compared to timber-clad or Colorbond-roofed homes in some risk categories.

Elevated on Stumps (At Least 1 Metre) This is a notable feature. Being elevated by at least one metre on stumps — a classic Queensland construction style — can actually work in the homeowner's favour when it comes to flood risk. Water is less likely to inundate the living areas of the home during a flood event, which some insurers factor into their pricing. However, elevated homes can also face higher wind-related risks, so the net effect varies by insurer.

Built in 1985 A home approaching 40 years old introduces some underwriting considerations. Older properties may have ageing plumbing, electrical systems, or roofing that increases the likelihood of a claim. Insurers will factor in the age of the building when calculating the premium, and it's worth ensuring your sum insured accurately reflects the cost to rebuild — not just the market value.

Solar Panels The presence of solar panels adds a modest layer of complexity to the policy. Solar systems need to be accounted for in the building sum insured, as they can be costly to replace after storm damage or hail. It's worth confirming with your insurer that the panels are explicitly covered under your building policy.

No Pool, No Ducted Climate Control The absence of a pool removes a common liability concern, and the lack of ducted air conditioning means fewer mechanical systems that could fail and trigger a claim. Both factors contribute to a cleaner risk profile.

Standard Fittings With standard-quality fittings throughout, there are no high-end fixtures or finishes that would push the rebuild cost — or the premium — higher than necessary.

---

Tips for Homeowners in Daisy Hill

1. Review your sum insured regularly With construction costs rising across Australia, a building sum insured set even a couple of years ago may no longer reflect what it would actually cost to rebuild your home today. Use a building cost calculator or speak with a quantity surveyor to make sure $400,000 is still an appropriate figure for a 214 sqm brick veneer home in this area.

2. Confirm solar panel coverage Don't assume your solar panels are automatically covered. Check your Product Disclosure Statement (PDS) to confirm they're included under the building definition, and verify the replacement value is factored into your sum insured.

3. Ask about flood cover Daisy Hill and the broader Brisbane region have experienced significant flood events in recent years. Make sure your policy explicitly includes flood cover — not just storm or rainwater damage — as these are often defined differently and can lead to disputes at claim time.

4. Compare quotes before renewal Insurance loyalty rarely pays off. Even if your current premium feels reasonable, it's worth running a comparison at renewal time. The 39 quotes sampled in Daisy Hill show a wide spread — from $1,216/yr at the 25th percentile to $3,321/yr at the 75th — meaning the right insurer for your property profile could save you hundreds annually.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for cover on a new property, CoverClub makes it easy to compare home and contents insurance quotes tailored to your specific address and situation. Get a quote today at CoverClub and see how your premium stacks up against the market — you might be surprised what you find.