If you own a free standing home in Dalby, QLD 4405, you're likely no stranger to the challenge of finding affordable home insurance. Dalby sits in Queensland's Darling Downs region — a landscape of rich agricultural land, warm summers, and the occasional severe storm that insurers pay close attention to. This article breaks down a real home and contents insurance quote for a three-bedroom, one-bathroom weatherboard home in the area, and puts that figure under the microscope so you can judge whether it represents good value.

---

Is This Quote Fair?

The quote in question comes in at $3,976 per year (or $381 per month) for combined home and contents cover, with a building sum insured of $580,000 and contents valued at $50,000. The building excess is $5,000 and the contents excess $2,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Compared to the suburb average of $4,280 per year, this quote sits roughly $300 below what most Dalby homeowners are paying for similar cover. That's a meaningful saving without having to sacrifice on the level of protection.

That said, "around average" doesn't necessarily mean "as good as it gets." The suburb's 25th percentile sits at $2,543 per year, which tells us that a quarter of comparable quotes in Dalby come in well below this figure. If you're prepared to shop around, there's a reasonable chance you could find more competitive pricing — particularly if your property profile and risk factors align favourably with certain insurers.

At the upper end, the 75th percentile reaches $4,888 per year, so this quote is comfortably below that threshold. In practical terms, you're not being overcharged, but you're also not getting the sharpest deal on the market.

---

How Dalby Compares

To put this quote in proper context, it helps to zoom out and look at the broader picture. You can explore the full breakdown on the Dalby suburb insurance stats page.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,976 |

| Dalby Suburb Average | $4,280 |

| Dalby Suburb Median | $3,373 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

| South Burnett LGA Average | $2,940 |

A few things stand out here. First, Queensland's state average of $9,129 is extraordinarily high — a figure heavily skewed by cyclone-prone coastal and far-north Queensland postcodes where premiums can be eye-watering. Dalby, sitting inland on the Darling Downs, doesn't carry that same level of cyclone exposure, which is reflected in its far more moderate pricing. You can see how QLD stacks up overall on the Queensland insurance stats page.

Second, the national average of $5,347 is also above this quote, though the national median of $2,764 is considerably lower. This again speaks to how averages get pulled upward by high-risk regions. Compared to national benchmarks, Dalby homeowners are paying broadly in line with the middle of the market.

Interestingly, the South Burnett LGA average of $2,940 is noticeably lower than the Dalby suburb average of $4,280. This suggests that within the broader LGA, some areas attract cheaper premiums than Dalby itself — possibly due to differences in flood risk mapping, proximity to emergency services, or the age and construction style of local housing stock.

---

Property Features That Affect Your Premium

This particular property has a number of characteristics that insurers weigh carefully when calculating risk.

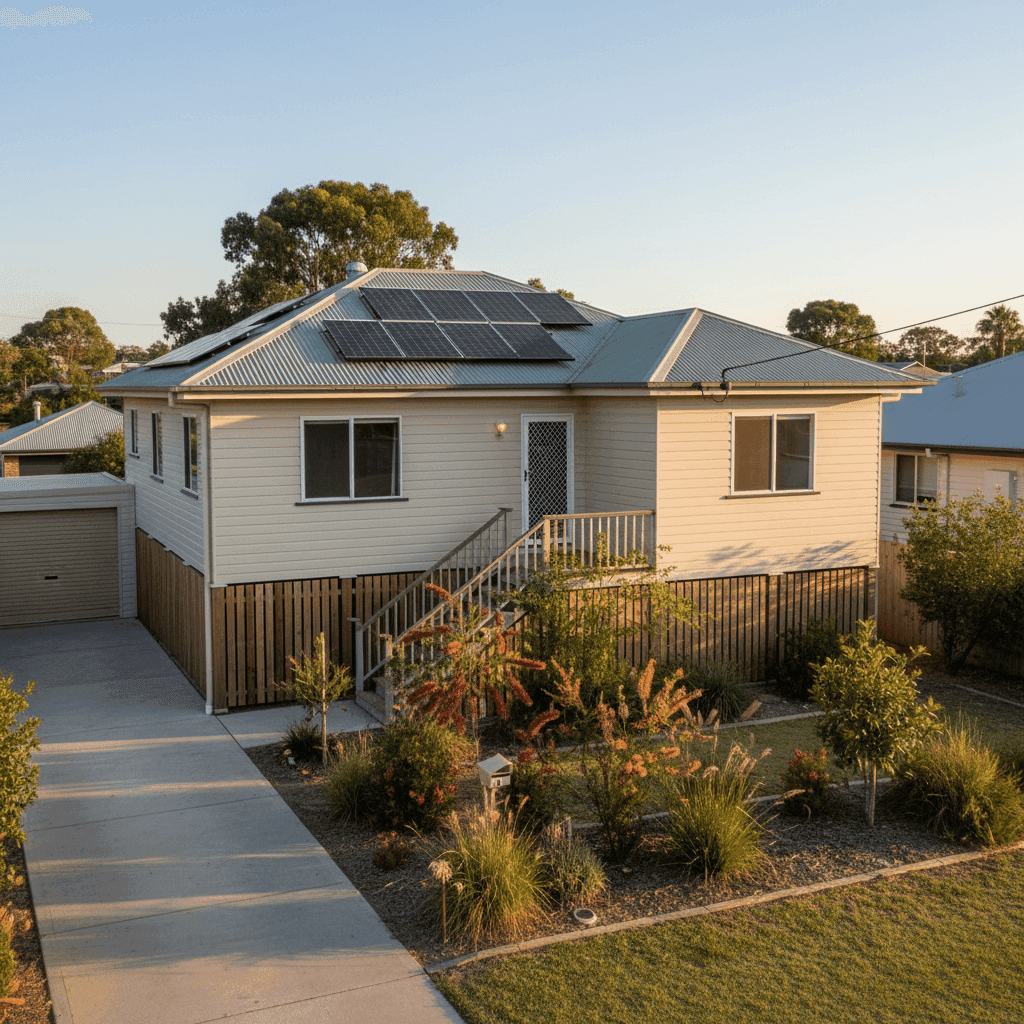

Age and construction: Built in 1901, this is a heritage-era home — over 120 years old. Older homes often attract higher premiums because ageing materials, outdated wiring, and plumbing systems can increase the likelihood and cost of a claim. Weatherboard timber walls, while charming and common across regional Queensland, are considered a higher fire risk than brick or rendered masonry, which can push premiums upward.

Stumped foundation: Homes on stumps (also known as pier foundations) are common in Queensland and offer good airflow underneath the structure. However, they can be more vulnerable to movement and pest damage over time, and some insurers factor this into their risk assessment.

Roof: The steel/Colorbond roof is actually a positive for insurers. Colorbond is durable, low-maintenance, and performs well in hail and storm events compared to older roofing materials like terracotta tiles or fibrous cement.

Solar panels: The presence of solar panels adds replacement value to the property. Homeowners should confirm that their building sum insured adequately accounts for the cost of replacing the solar system, as panels and inverters can represent a significant expense.

Ducted climate control: Ducted systems are expensive to repair or replace, and their inclusion should be reflected in both the building sum insured and the overall assessment of the property's replacement cost.

No pool, no cyclone risk zone: The absence of a pool removes one common source of liability claims, and being outside a designated cyclone risk area keeps the premium from escalating the way it does for coastal Queensland properties.

Building size and sum insured: At 130 sqm with a building sum insured of $580,000, the per-square-metre replacement cost is approximately $4,460. Given the age of the property and the cost of restoring period-era features, this figure may be appropriate — but it's worth getting a professional building valuation to ensure you're neither underinsured nor paying for more cover than you need.

---

Tips for Homeowners in Dalby

1. Review your sum insured regularly Construction costs have risen sharply in recent years. A sum insured set even two or three years ago may no longer reflect the true cost of rebuilding your home from scratch. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Ask about excess trade-offs This quote carries a $5,000 building excess, which is on the higher side. While a higher excess typically reduces your annual premium, it also means you'll need to cover more out of pocket if you do make a claim. Consider whether a lower excess might be worth a modest premium increase, particularly for an older property where maintenance claims could arise.

3. Confirm your solar panels are covered Solar systems are sometimes treated as a grey area between building and contents cover. Check your policy wording carefully to ensure your panels, inverter, and associated wiring are fully covered under your building policy.

4. Compare quotes before renewal Insurance loyalty rarely pays. Insurers frequently offer their best pricing to new customers, meaning long-term policyholders can quietly drift into paying above-market rates. Shopping around at renewal — or even mid-term — is one of the simplest ways to keep your premium in check.

---

Ready to Compare?

Whether this quote feels right or you suspect you could do better, the smartest move is to see what else is out there. At CoverClub, we make it easy to compare home and contents insurance options tailored to your property and location. Get a quote today and find out whether you're getting the cover you deserve at a price that makes sense.