If you own a four-bedroom free standing home in Dapto, NSW 2530, you've probably wondered whether your home insurance premium is reasonable — or whether you're quietly paying too much. Dapto is a well-established suburb in the Wollongong local government area, sitting at the southern end of Lake Illawarra. It's a popular choice for families thanks to its affordability relative to Sydney, good schools, and easy freeway access. But how does that translate into home insurance costs? Let's break it down.

---

Is This Quote Fair?

The quote in question comes to $2,240 per year (or $215 per month) for combined home and contents cover on a four-bedroom, two-bathroom free standing home. The building is insured for $586,000, with contents covered at $50,000, and both building and contents excesses are set at $1,000.

Our price rating for this quote is EXPENSIVE — Above Average.

To put that in context: the average home and contents premium across Dapto sits at around $1,555 per year, with a median of $1,452. This quote lands well above both figures — roughly 44% higher than the suburb average and 54% above the median. Even when measured against the 75th percentile of local quotes ($1,892/yr), this premium still exceeds what most Dapto homeowners are paying.

That said, "expensive" doesn't automatically mean "wrong." A higher sum insured, specific property features, and the insurer's own risk appetite all play a role. But it does suggest there's meaningful room to shop around.

---

How Dapto Compares

Understanding where Dapto sits in the broader insurance landscape helps put this quote in perspective. Here's a quick snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Dapto (NSW 2530) | $1,555/yr | $1,452/yr |

| Wollongong LGA | $2,751/yr | — |

| NSW (State) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

(Based on 23 quotes sampled for the Dapto suburb. [View full Dapto suburb stats](https://coverclub.com.au/stats/NSW/2530/dapto).)

A few things stand out here. First, Dapto is actually quite affordable compared to both the NSW state average and the national average — the state median of $3,770 is more than double Dapto's local median. This reflects the relatively lower risk profile of the suburb compared to coastal, flood-prone, or cyclone-affected areas of NSW and Queensland.

Second, the Wollongong LGA average of $2,751 is notably higher than Dapto's suburb average, suggesting that other parts of the LGA — particularly areas closer to the escarpment or waterfront — carry higher premiums. Dapto, positioned slightly inland near the lake's southern fringe, benefits from a more moderate risk profile overall.

The quote at $2,240 sits between Dapto's local average and the broader Wollongong LGA average, which could indicate the insurer is pricing based on LGA-level data rather than suburb-specific risk — a common practice that can disadvantage homeowners in lower-risk pockets of a larger area.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining through an insurance lens:

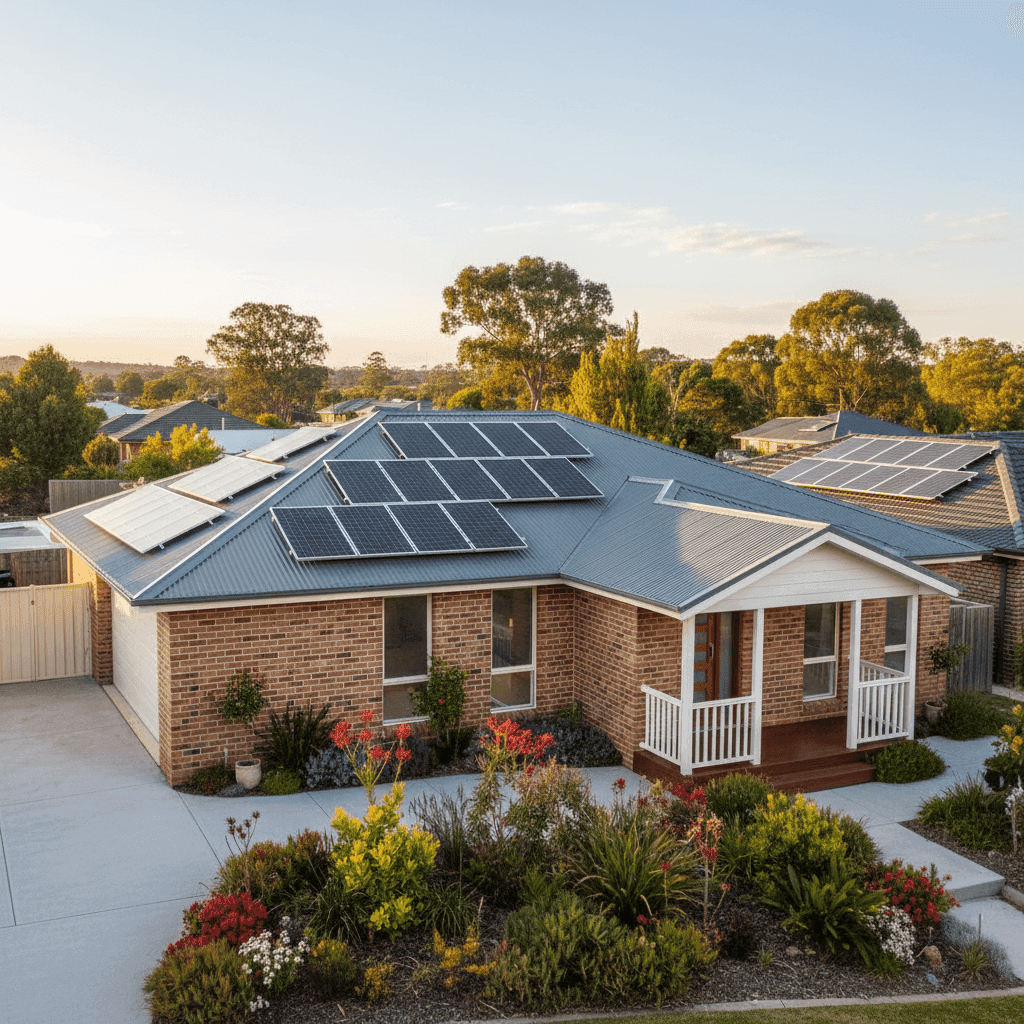

Brick Veneer Walls Brick veneer is a well-regarded construction type for insurance purposes. It offers solid fire resistance and durability, which generally works in your favour at premium time. Full brick is slightly preferred by some insurers, but brick veneer is widely considered a lower-risk external wall material compared to timber weatherboard or fibre cement.

Steel/Colorbond Roof A Colorbond steel roof is another positive signal to insurers. It's durable, low-maintenance, and performs well in high-wind events. Unlike terracotta or concrete tiles, steel roofing is less prone to cracking or displacement in storms — a meaningful consideration in the Illawarra region where easterly weather systems can bring significant rainfall.

Stump Foundation The home sits on stumps, which is common in older properties built around the 1980s in this region. Stumped foundations can be a mild risk flag for some insurers, as they may be associated with movement, moisture, or pest vulnerability over time. Ensuring stumps are in good condition — and documenting this — can help when negotiating cover.

Timber/Laminate Flooring Flooring type contributes to the overall rebuild cost calculation. Timber and laminate floors are mid-range in terms of replacement cost and don't typically push premiums significantly in either direction.

Solar Panels This property has solar panels installed, which can add modestly to the insured value of the building. Most home insurance policies cover solar panels as part of the building sum insured, but it's worth confirming your policy explicitly includes them — and that your sum insured accounts for the replacement cost of the system.

Ducted Climate Control Ducted air conditioning is a fixed building feature that contributes to rebuild costs. Like solar panels, it should be factored into your building sum insured to avoid underinsurance.

Construction Year: 1984 At around 40 years old, this home sits in a bracket that some insurers treat with additional scrutiny — particularly regarding electrical wiring, plumbing, and roofing integrity. If any of these have been updated or renovated, it's worth noting this to your insurer, as it can positively influence your risk assessment.

---

Tips for Homeowners in Dapto

1. Shop around — seriously With a premium sitting above the suburb average, this is a clear case where comparing quotes across multiple insurers could yield meaningful savings. Use CoverClub's quote comparison tool to see what other providers are offering for the same level of cover.

2. Review your sum insured carefully A building sum insured of $586,000 for a 214 sqm home in Dapto represents a rebuild cost of roughly $2,737 per sqm — which is within a reasonable range for 2026 construction costs. However, it's worth validating this figure using a professional building cost estimator or the calculator provided by your insurer. Overinsuring unnecessarily inflates your premium; underinsuring leaves you exposed.

3. Check your policy covers solar panels and ducted A/C These are fixed assets that add real value to your home. Confirm they're explicitly listed under your building cover and that the sum insured reflects their current replacement cost — particularly given the rising cost of solar systems and HVAC equipment.

4. Consider raising your excess to reduce your premium With both building and contents excesses currently at $1,000, there may be scope to increase these — particularly if you have an emergency fund that could comfortably cover a higher out-of-pocket cost in a claim. Many insurers offer meaningfully lower premiums in exchange for a higher excess, which can make sense for homeowners who are unlikely to make small claims.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new property, it pays to know what the market looks like. CoverClub makes it easy to compare home and contents insurance quotes across multiple providers — so you can see exactly where your premium sits and whether there's a better deal available. Start your free comparison today and make sure you're getting the right cover at a fair price.

For more data on insurance costs in your area, visit our Dapto suburb stats page or explore NSW-wide insurance benchmarks.