If you own a free standing home in Darley, VIC 3340, you're likely already aware that home insurance is one of those non-negotiable household expenses — but how much should you actually be paying? This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom weatherboard property in Darley, comparing it against local, state, and national benchmarks so you can make a more informed decision at renewal time.

---

Is This Quote Fair?

The quote in question comes in at $1,991 per year (or $202 per month) for combined home and contents cover, with a building sum insured of $670,000 and contents valued at $50,000. The building excess sits at $2,500, while the contents excess is $2,000.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up when you dig into the numbers. The suburb average premium in Darley is $2,502 per year, and the median sits at $2,256 per year. This quote falls below both figures, landing between the 25th percentile ($1,781/yr) and the median ($2,256/yr) of the 60 quotes we've collected for this area. In other words, roughly half of Darley homeowners are paying more, and about a quarter are paying less.

It's not a bargain-basement price, but it's genuinely competitive for the property type and features involved — particularly given the pool, solar panels, and ducted climate control, all of which can push premiums higher (more on those shortly).

---

How Darley Compares

To put this quote in broader context, here's how Darley stacks up against the rest of Victoria and the country:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Darley (3340) | $2,502/yr | $2,256/yr |

| LGA (Melton) | $2,509/yr | — |

| Victoria | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Darley and the broader Melton LGA are closely aligned, suggesting consistent pricing across the region rather than any suburb-specific loading. Second, this quote sits 33% below the Victorian average and a remarkable 63% below the national average — though that national figure is heavily skewed by high-risk areas in Queensland and Western Australia, where cyclone and flood exposure drives premiums sky-high.

Compared to the Victorian state average, Darley homeowners generally enjoy more affordable premiums, which reflects the area's relatively low natural hazard profile. You can explore the full Darley suburb insurance statistics or browse national home insurance data to see how your own situation compares.

---

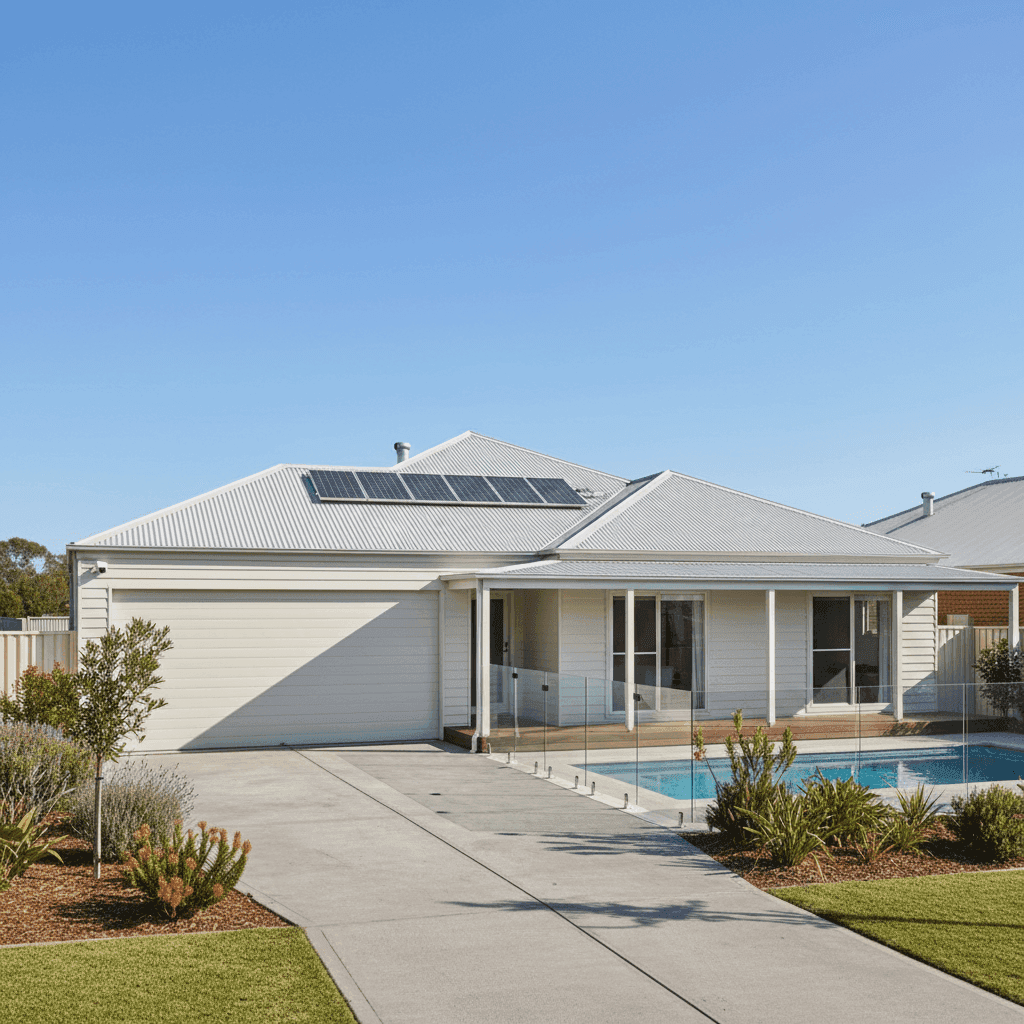

Property Features That Affect Your Premium

Not all homes are priced the same, and several characteristics of this particular property play a meaningful role in how insurers calculate the premium.

Weatherboard Timber Construction

Weatherboard homes are among the most common dwelling types in Victoria's growth corridors, but they do carry a higher fire risk than brick veneer or full brick construction. Insurers typically apply a modest loading for timber-framed and weatherboard-clad homes, reflecting the greater potential for fire spread and the cost of repairs or rebuilding.

Steel/Colorbond Roof

On the positive side, a Colorbond steel roof is generally viewed favourably by insurers. It's durable, low-maintenance, resistant to ember attack, and less susceptible to storm damage than older tile or fibrous cement roofing. This can help offset some of the loading associated with timber wall construction.

Stump Foundation

Homes on stumps (also called pier or post foundations) are common in older Victorian properties and can be a flag for insurers — particularly around subsidence risk and the cost of underfloor access during repairs. The 1992 construction year means this home predates many modern building standards, which is worth keeping in mind when reviewing your sum insured.

Swimming Pool

A pool adds liability exposure to any home insurance policy. If a visitor or neighbour is injured on your property, your insurer may be called upon to cover legal costs and damages. Many policies include some level of legal liability cover, but it's worth confirming the limit — typically $20 million is standard in Australia.

Solar Panels

Solar panels are increasingly common across Victoria's outer suburbs, but they add replacement value to the building and can complicate roof repairs. Insurers vary in how they treat solar systems — some include them automatically under the building sum insured, while others require them to be listed separately. Always confirm your panels are covered.

Ducted Climate Control

Ducted heating and cooling systems are a significant fixed asset and can be expensive to repair or replace. Their inclusion in the building sum insured is standard, but it's a good reminder to ensure your $670,000 building cover is sufficient to account for all fixed inclusions — particularly in the current construction cost environment.

---

Tips for Homeowners in Darley

Whether you're renewing your current policy or shopping around for the first time, here are four practical steps worth taking.

1. Review your building sum insured annually. Construction costs in Victoria have risen sharply over the past few years. A sum insured that was adequate in 2020 may fall short today. Use an independent building cost calculator or ask your insurer how they determine replacement value — and make sure it accounts for demolition, debris removal, and professional fees, not just the build itself.

2. Check how your solar panels are covered. Ask your insurer directly whether your solar system is included under the building sum insured or whether it needs to be listed as a separate item. If it's not explicitly covered, you could face a significant gap in the event of storm damage or a rooftop fire.

3. Understand your pool liability obligations. Pool fencing laws in Victoria are strict, and non-compliance can affect both your legal standing and your insurance coverage. Ensure your pool barrier meets current Victorian standards — not just for safety, but to avoid any potential claim complications.

4. Compare quotes at renewal, not just at purchase. Many homeowners set and forget their home insurance, but premiums can shift significantly from year to year. Even if your current quote is rated as fair, it's worth running a comparison to see whether another insurer offers equivalent cover at a lower price — or better cover at the same price.

---

Find a Better Deal with CoverClub

Whether this quote is your current policy or one you're considering, the best way to know if you're getting value is to compare. At CoverClub, we make it easy to see how your premium stacks up and explore alternatives — all in one place. Get a home insurance quote today and see what's available for your Darley property.