If you own a free standing home in Dawesville, WA 6211, you already know it's one of the Peel region's most appealing coastal suburbs — nestled between the Peel Inlet and the Indian Ocean, with a relaxed lifestyle that attracts families and retirees alike. But that enviable location comes with its own set of insurance considerations. This article breaks down a real building insurance quote for a four-bedroom, three-bathroom free standing home in the area, compares it against local, state, and national benchmarks, and offers practical advice for homeowners looking to get better value on their cover.

---

Is This Quote Fair?

The quote in question is $10,481 per year (or $1,004/month) for building-only cover with a sum insured of $800,000 and a $2,000 building excess. Our price rating for this quote is EXPENSIVE — above average.

To put that in perspective, the suburb average premium in Dawesville sits at just $1,935 per year, and the median is even lower at $1,742. This quote is more than five times the local median — a significant gap that warrants a closer look.

Even when compared to the broader Western Australian average of $2,811/year or the national average of $5,347/year, this premium stands out as unusually high. It's worth noting that the national average is skewed upward by high-risk regions such as cyclone-prone areas in Queensland and the Northern Territory, so a quote nearly double the national average for a property in a non-cyclone zone is a red flag worth investigating.

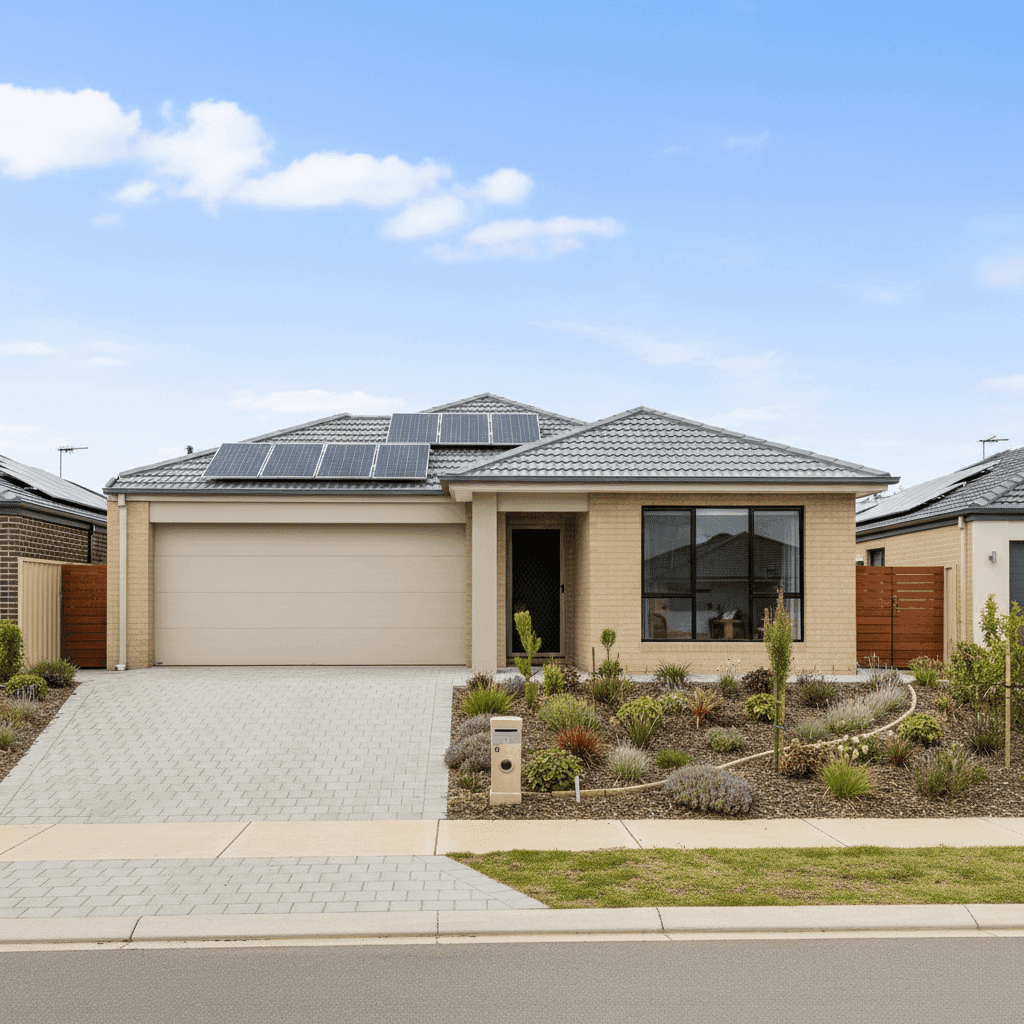

The high sum insured of $800,000 is likely the single biggest driver here. Rebuilding a 235 sqm double brick home with quality fittings, ducted climate control, and solar panels is not cheap — but homeowners should verify whether this figure is based on an accurate building replacement cost estimate, or whether it may be over-insured. An inflated sum insured directly inflates your premium.

---

How Dawesville Compares

Here's a snapshot of how premiums stack up across different reference points:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $10,481 |

| Dawesville Suburb Average | $1,935 |

| Dawesville Suburb Median | $1,742 |

| Dawesville 25th Percentile | $1,013 |

| Dawesville 75th Percentile | $2,262 |

| Waroona LGA Average | $2,254 |

| WA State Average | $2,811 |

| National Average | $5,347 |

| National Median | $2,764 |

You can explore live suburb-level data on the Dawesville insurance stats page, compare it against the WA state overview, or see how it sits in the broader national context.

The sample of 38 quotes from Dawesville gives us a reasonably reliable local benchmark. With 75% of local quotes coming in under $2,262 per year, a premium of $10,481 places this property well outside the typical range — even accounting for a higher-than-average sum insured.

---

Property Features That Affect Your Premium

Several characteristics of this property influence the premium, both positively and negatively.

Features That May Increase the Premium

- Sum Insured ($800,000): This is the most significant factor. At 235 sqm, an $800,000 sum insured implies a rebuild cost of roughly $3,400 per sqm — on the higher end, even for quality double brick construction in WA. It's worth obtaining a professional building replacement cost estimate to confirm this figure is accurate.

- Ducted Climate Control: Ducted air conditioning systems are expensive to replace and add to the overall insured value of the home's fixtures and fittings.

- Solar Panels: Rooftop solar systems are typically covered under building insurance and add to the replacement cost calculation, pushing premiums up slightly.

- Slab Foundation & Tile Flooring: These are generally neutral to positive risk factors, though tiled flooring throughout can increase replacement costs compared to carpet.

Features That May Reduce the Premium

- Double Brick Construction: Double brick is one of the most insurer-favoured wall types in Australia. It's highly resistant to fire, wind, and impact, and typically attracts lower premiums than timber or clad construction.

- Tiled Roof: Terracotta or concrete tiles are durable and fire-resistant, generally viewed favourably by insurers compared to corrugated iron or Colorbond in some risk scenarios.

- 2009 Build Year: A relatively modern home means updated wiring, plumbing, and structural standards — all of which reduce the likelihood of claims related to ageing infrastructure.

- Not in a Cyclone Risk Zone: Dawesville is not classified as a cyclone risk area, which removes one of the most significant premium loading factors seen in northern WA and Queensland.

- Slight Elevation (Less Than 1m): Modest elevation can offer marginal protection against surface water flooding, though it's unlikely to dramatically affect the premium at this level.

---

Tips for Homeowners in Dawesville

1. Review Your Sum Insured Carefully

The most actionable step you can take is to verify your building's replacement value. Use an independent quantity surveyor or a reputable online calculator to estimate the true cost of rebuilding your home from scratch — not its market value. Over-insuring by even $100,000–$200,000 can add hundreds of dollars to your annual premium unnecessarily.

2. Shop Around and Compare Multiple Insurers

No two insurers price the same property the same way. Given that this quote is significantly above the Dawesville suburb average, there's a strong chance that alternative insurers would price this risk more competitively. Get a comparison quote through CoverClub to see what other providers are offering for the same property.

3. Consider a Higher Excess

This quote carries a $2,000 building excess. Opting for a higher voluntary excess — say $3,000 or $5,000 — can meaningfully reduce your annual premium. If you have the financial capacity to absorb a larger out-of-pocket cost in the event of a claim, this is often a smart trade-off.

4. Bundle Building and Contents Cover

While this quote is for building only, many insurers offer meaningful discounts when you combine building and contents policies. If you're currently holding a separate contents policy elsewhere, it may be worth pricing a combined package — you could end up paying less overall while simplifying your insurance administration.

---

Ready to Find a Better Deal?

Whether you're reviewing an existing policy or shopping for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see how your premium stacks up against real quotes from Dawesville and across Western Australia. Start your free comparison today and make sure your home is covered at a price that actually makes sense.