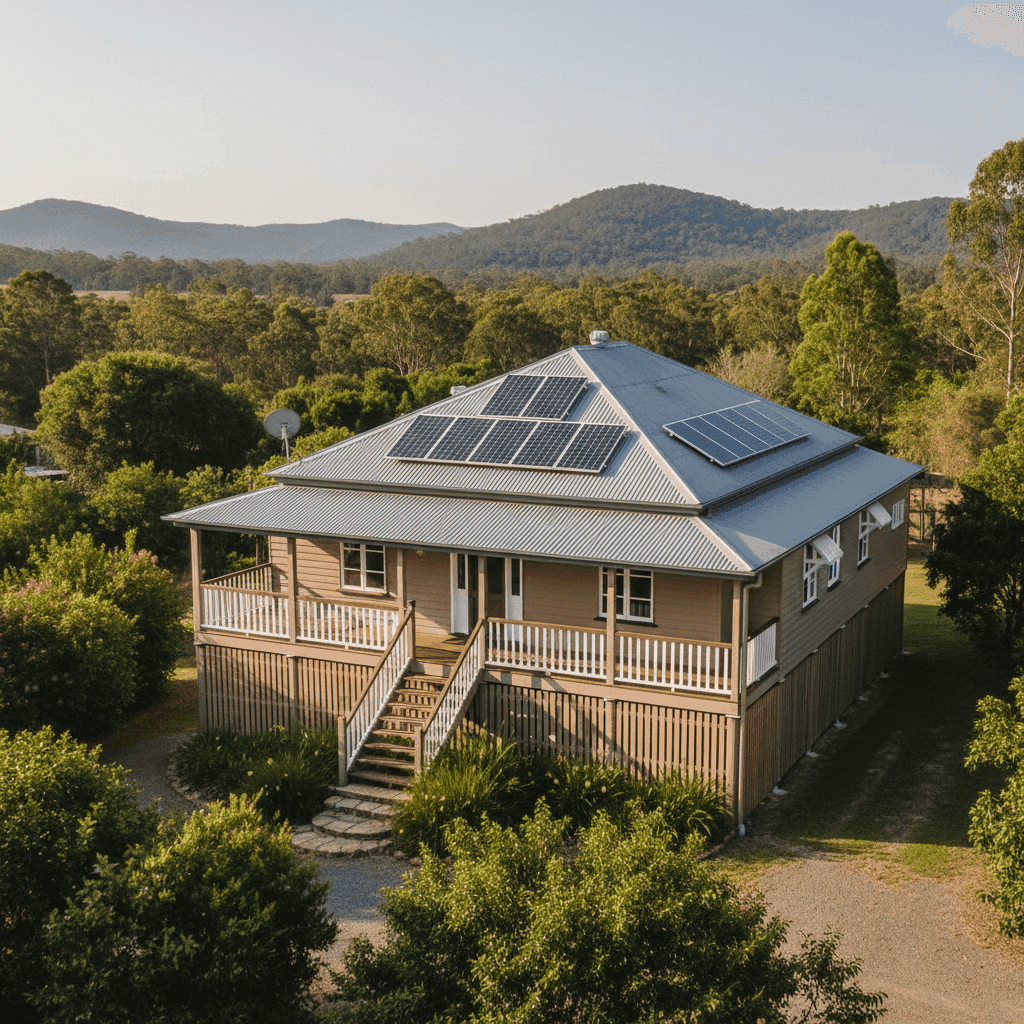

Nestled in the scenic hinterland north of Brisbane, Dayboro is a charming semi-rural suburb that blends country lifestyle with reasonable proximity to the city. It's also home to a wide variety of properties — including larger, character-filled homes like the five-bedroom free-standing weatherboard we're analysing today. If you own a similar property in postcode 4521 and you're wondering whether your home insurance premium stacks up, this breakdown is for you.

---

Is This Quote Fair?

The quote in question comes in at $3,419 per year (or $328/month) for combined home and contents cover, with a building sum insured of $996,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — around average for the area. That assessment is backed by real data: based on 48 quotes collected for Dayboro (QLD 4521), the suburb's median premium sits at $3,358/yr, meaning this quote lands just $61 above the midpoint. It's comfortably within the typical range for the suburb — not the cheapest available, but far from the most expensive either.

To put it in context, the suburb's 25th percentile is $2,855/yr and the 75th percentile reaches $4,675/yr. This quote sits between the median and the upper quartile, which makes sense given the property's generous size (315 sqm), elevated construction, and above-average sum insured.

---

How Dayboro Compares

One of the most striking things about this quote is how well Dayboro performs relative to broader benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Dayboro (4521) | $3,884/yr | $3,358/yr |

| Moreton Bay LGA | $3,435/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

The Queensland state average of $9,129/yr is heavily skewed by high-risk coastal and cyclone-prone regions in Far North Queensland — areas like Cairns and Townsville where premiums can be eye-watering. Dayboro is not classified as a cyclone risk area, which is a significant advantage. The state median of $3,903/yr is a more meaningful comparison point, and this quote sits just below it.

Against national figures, the picture is similarly reassuring. The national average of $5,347/yr is dragged up by high-risk postcodes across QLD, WA, and NT. At $3,419/yr, this Dayboro quote is nearly $2,000 below that national average — a meaningful saving for a large, well-appointed home.

The Moreton Bay LGA average of $3,435/yr is perhaps the most relevant local comparison, and this quote is almost exactly in line with it — just $16 below. All things considered, the "fair" rating is well-deserved.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them can help you make smarter decisions when reviewing your cover.

Weatherboard timber walls are one of the most influential factors. Timber-framed homes are generally considered higher risk than brick veneer or double brick construction because they are more susceptible to fire and can be more costly to repair or rebuild. Insurers typically price this in, so it's worth ensuring your sum insured accurately reflects the full cost of rebuilding a timber home.

Elevated on stumps is a classic Queenslander feature, and it cuts both ways. On the positive side, elevation of at least one metre provides meaningful flood resilience — water is less likely to enter the living areas during a flood or heavy rain event, which is a genuine risk in parts of south-east Queensland. On the downside, stumped homes can be more expensive to repair structurally, and some insurers price this accordingly.

Steel/Colorbond roofing is generally viewed favourably by insurers. It's durable, low-maintenance, and performs well in storms compared to older terracotta or concrete tile roofs. For a property built in 1996, a Colorbond roof is a solid asset.

Solar panels add value to the property but also add complexity to an insurance claim. Make sure your policy explicitly covers solar panels — both the panels themselves and any damage they might cause to the roof. Some policies include them automatically; others require you to specify them.

Ducted climate control is a high-value fixed installation that contributes to the building sum insured. At $996,000, the sum insured here is substantial, which partly explains the premium sitting above the suburb median. Underinsurance is a serious risk in Australia — always ensure your sum insured reflects current rebuild costs, not just market value.

---

Tips for Homeowners in Dayboro

1. Review your sum insured annually. Construction costs have risen sharply in recent years. A sum insured that was adequate in 2021 may fall well short today. Use a building cost calculator or speak to a quantity surveyor to confirm your $996,000 figure still covers a full rebuild — especially for a 315 sqm weatherboard home with quality fittings.

2. Check your flood and stormwater cover. Dayboro sits in a catchment area that can experience significant rainfall events. While your elevated foundations offer some natural protection, confirm that your policy covers flood (not just storm damage) — these are often separate definitions in Australian policies, and the distinction matters enormously at claim time.

3. Confirm solar panel coverage. With solar panels on the roof, verify that your policy covers them for both accidental damage and storm events. Also check whether the policy covers damage caused by the panels (e.g., a panel coming loose in a storm and damaging the roof). This is an easy oversight that can be costly.

4. Compare quotes before renewal. A "fair" rating means you're not being overcharged — but it doesn't mean you couldn't do better. Insurers reprice risk constantly, and loyalty doesn't always pay. Set a reminder to compare quotes at least 30 days before your renewal date to give yourself time to switch if a better deal is available.

---

Compare Your Home Insurance Today

Whether you're renewing your existing policy or insuring a new home in Dayboro, it pays to see what the market is offering. CoverClub makes it easy to compare home insurance quotes in minutes — no jargon, no pressure, just clear data to help you make a confident decision. You can also explore detailed premium statistics for Dayboro and postcode 4521 to benchmark any quote you receive.