If you own a four-bedroom free standing home in Deception Bay, QLD 4508, you're probably well aware that home insurance isn't cheap in South-East Queensland. Sitting within the Moreton Bay region, Deception Bay is a well-established coastal suburb that presents a particular mix of risk factors for insurers — from its proximity to Moreton Bay to its broad range of housing stock. This article breaks down a real home insurance quote for a brick veneer property in the area, compares it against local, state and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $3,166 per year (or $309/month) for combined Home and Contents cover, with a $1,000 excess on both building and contents. The building is insured for $1,000,000 and contents are covered for $50,000.

Our rating for this quote is FAIR — Around Average, and the data backs that up. Based on 87 quotes collected for Deception Bay (postcode 4508), the suburb average sits at $3,048/year and the median at $2,655/year. At $3,166, this quote lands just above the suburb average and comfortably within the 25th–75th percentile range of $1,957 to $3,247.

In plain terms: you're not being overcharged, but you're also not getting a bargain. There's a reasonable spread of cheaper options available in the suburb — the bottom quarter of quotes come in under $1,957 — so it's worth exploring whether a comparable policy could be found at a lower price point.

---

How Deception Bay Compares

One of the more reassuring aspects of this quote is how Deception Bay stacks up against broader benchmarks. Queensland as a whole is notoriously expensive for home insurance, largely due to cyclone exposure in the north, flooding risk in low-lying areas, and the general cost of rebuilding in a high-demand construction market.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Deception Bay (4508) | $3,048/yr | $2,655/yr |

| Moreton Bay LGA | $3,145/yr | — |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

As you can see, Queensland's average premium of $4,547 is significantly higher than the national average of $2,965. Deception Bay actually performs quite well by Queensland standards — its suburb average is roughly 33% below the state average, which is a meaningful difference. The suburb's average is also broadly in line with the national figure, suggesting that despite being in a higher-risk state, Deception Bay itself isn't dramatically more expensive than the rest of the country.

The Moreton Bay LGA average of $3,145 is close to the suburb figure, indicating consistent pricing across the region rather than any unusual outlier risk specific to this pocket of the coast.

---

Property Features That Affect Your Premium

Several characteristics of this particular property will influence how insurers assess and price the risk.

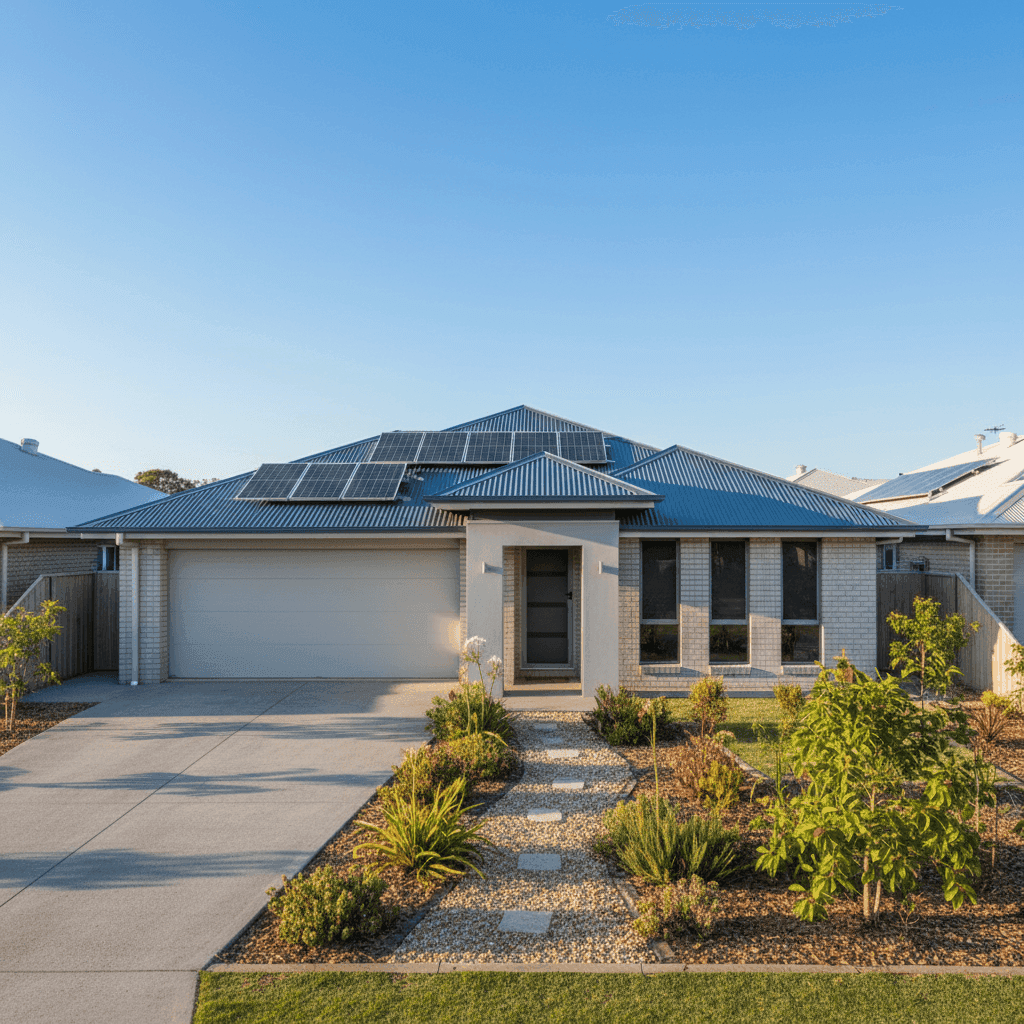

Brick Veneer Walls & Colorbond Roof This is a favourable combination from an insurer's perspective. Brick veneer is considered a resilient external wall material — it handles heat, minor impact and moisture better than many alternatives. Colorbond steel roofing is similarly well-regarded: it's durable, resistant to corrosion, and performs reliably in storm conditions. Together, these materials typically attract more competitive premiums compared to, say, weatherboard cladding or older tile roofing.

Concrete Slab Foundation A slab foundation is standard for homes of this era (built in 2004) and is generally viewed as stable and low-risk. It avoids some of the subsidence and pest-related concerns that can affect older homes on stumps or piers.

Solar Panels The presence of solar panels adds modest complexity to a home insurance policy. Panels represent a capital asset that can be damaged by hail, storm or falling debris, and some insurers include them under building cover automatically while others may require a separate endorsement. It's worth confirming with your insurer exactly how your solar system is covered — particularly the panels themselves, inverter, and any battery storage if applicable.

Standard Fittings & Tile Flooring Standard-quality fittings keep the rebuild cost estimate more predictable and generally don't push premiums higher the way premium or custom fixtures might. Tile flooring throughout is practical and durable, and won't inflate the contents or building valuation unnecessarily.

Building Size: 214 sqm At 214 square metres, this is a mid-to-large sized home for the suburb. The $1,000,000 sum insured is on the higher end for a property of this size and construction type — it may be worth reviewing whether that figure accurately reflects the current cost to rebuild, as over-insuring can mean paying more in premiums than necessary.

---

Tips for Homeowners in Deception Bay

1. Review your sum insured regularly Construction costs have risen sharply in recent years, but that doesn't necessarily mean your sum insured needs to be set at $1,000,000 for a 214 sqm home. Use a building cost calculator or speak with a quantity surveyor to get a realistic rebuild estimate. Over-insuring inflates your premium without providing additional benefit at claim time.

2. Compare quotes — don't auto-renew With 87 quotes in our Deception Bay dataset ranging from under $1,957 to over $3,247, there's clearly significant variation between insurers. Loyalty doesn't always pay in insurance. Run a fresh comparison at CoverClub each year before your renewal date to make sure you're still getting a competitive deal.

3. Confirm solar panel coverage Given the property has solar panels installed, double-check the policy wording on how they're covered. Some policies treat panels as part of the building sum insured, while others have specific sub-limits or exclusions. If your system is valuable, ensure the coverage is adequate.

4. Consider your excess level Both the building and contents excess on this quote are set at $1,000. Opting for a higher voluntary excess — say $2,500 or $5,000 — can meaningfully reduce your annual premium. If you're financially comfortable absorbing a larger out-of-pocket cost in the event of a claim, this can be an effective way to lower ongoing costs.

---

Ready to Compare?

Whether you're renewing your policy or shopping around for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see how your current premium stacks up against the market — and to find a policy that suits both your property and your budget. Enter your address to get started.