Deception Bay is a coastal suburb on the northern fringe of the Moreton Bay region, roughly 40 kilometres north of Brisbane's CBD. It's a popular choice for families seeking space and relative affordability — and a six-bedroom, free-standing home here is exactly the kind of substantial property that warrants careful attention when it comes to insurance. In this article, we break down a real home and contents insurance quote for a property like this, compare it against suburb, state, and national benchmarks, and share some practical tips for getting the best possible cover at a fair price.

---

Is This Quote Fair?

The quote in question sits at $3,630 per year (or $348 per month), covering both building (insured at $1,099,000) and contents ($40,000), each with a $2,000 excess. Our price rating for this quote is Expensive — above average for the Deception Bay area.

To put that in context: the suburb average premium across 107 quotes collected for Deception Bay (4508) is $2,727 per year, with a median of $2,612. This quote comes in roughly 33% above the suburb average and sits well above the 75th percentile threshold of $3,269 — meaning it's pricier than at least three-quarters of comparable quotes in the area.

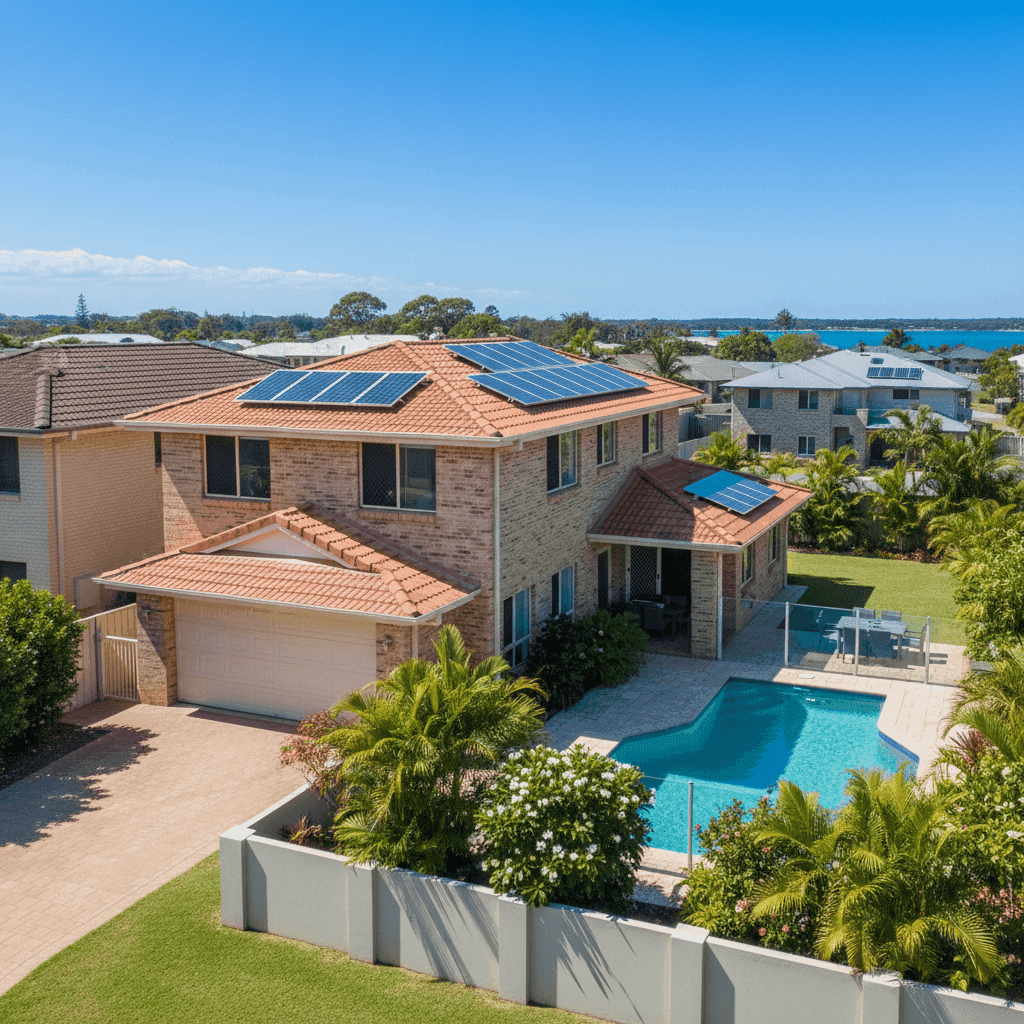

That said, "expensive" doesn't automatically mean "wrong." A 354 sqm home with six bedrooms, three bathrooms, a pool, solar panels, and ducted climate control is a larger and more complex property than most. The building sum insured of $1,099,000 is substantial, and insurers will price accordingly. Still, there's a reasonable case to be made that this premium deserves scrutiny — and potentially a second opinion.

---

How Deception Bay Compares

Understanding where Deception Bay sits within the broader insurance landscape is useful context for any homeowner.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Deception Bay (4508) | $2,727/yr | $2,612/yr |

| Moreton Bay LGA | $3,435/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. Queensland's average premium of $9,129 is dramatically higher than the national average of $5,347 — largely because the state average is pulled upward by high-risk cyclone and flood zones in North Queensland. The median is a more reliable indicator for most homeowners: QLD sits at $3,903, while the national median is $2,764.

Deception Bay's median of $2,612 is actually slightly below the national median, which is encouraging. The suburb is not classified as a cyclone risk area, and while parts of the Moreton Bay region can be susceptible to flooding, Deception Bay generally benefits from more moderate risk profiles compared to other QLD postcodes. You can explore the full Queensland insurance data or the national overview for broader comparisons.

At $3,630, this particular quote exceeds both the suburb and national medians — reinforcing the "expensive" rating and suggesting there may be room to find a more competitive price.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on what insurers charge. Here's how they stack up:

Double brick construction is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well in storms — all factors that can reduce the likelihood and severity of claims. Homes with brick veneer or lightweight cladding often attract higher premiums by comparison.

Tiled roof is another positive. Concrete or terracotta tiles are considered among the more resilient roofing materials, particularly for wind and hail events. They tend to fare better than Colorbond or corrugated iron in some storm scenarios, though they can be more costly to repair if damaged.

Slab foundation is standard for many Queensland homes of this era and doesn't typically add risk from an insurer's perspective. Similarly, tiled flooring throughout is a practical, low-maintenance choice that reduces the risk of water damage compared to timber or carpet.

The swimming pool adds replacement cost to the building sum insured and introduces some liability considerations — insurers factor in the cost of pool fencing, filtration systems, and potential damage. Solar panels are another asset that increases the rebuild cost and must be adequately covered under the building policy. Many homeowners underestimate the replacement value of a full solar system.

Ducted climate control is a significant fixture that adds to the building's value and complexity. Ensuring it's properly included in your sum insured is important — ducted systems can cost tens of thousands of dollars to replace.

Construction year (1980) is worth noting. Homes built in the 1980s may have older wiring, plumbing, or roofing that some insurers view as higher risk. It's worth confirming that any updates to these systems are documented, as this can positively influence your premium.

---

Tips for Homeowners in Deception Bay

1. Review your sum insured carefully At $1,099,000, the building sum insured is substantial — and rightly so for a 354 sqm home with premium fixtures. But it's worth using a professional building cost estimator (or consulting a quantity surveyor) to confirm this figure is accurate. Being over-insured means paying more than necessary; being under-insured can leave you seriously exposed at claim time.

2. Shop around — especially if your quote is above the suburb average With this quote sitting above the 75th percentile for Deception Bay, there's a real chance a competing insurer would offer similar cover for less. Premiums can vary significantly between providers for identical properties. Get a comparison quote through CoverClub to see what else is available.

3. Consider your excess strategically Both the building and contents excess are set at $2,000. Opting for a higher excess — say $2,500 or $3,000 — can meaningfully reduce your annual premium. If you're unlikely to make small claims, this trade-off often makes financial sense over the long term.

4. Check what's included for pool and solar Not all policies treat pools and solar panels the same way. Some insurers include them automatically under building cover; others require specific endorsements or have sub-limits. Read the Product Disclosure Statement (PDS) carefully, or ask your insurer directly, to confirm these assets are fully covered.

---

Ready to Compare?

Whether you're renewing your policy or shopping for the first time, it pays to compare. CoverClub makes it easy to see how your premium stacks up against real quotes from across Deception Bay and Queensland. Start your comparison at CoverClub and make sure you're not paying more than you should for the cover your home deserves.