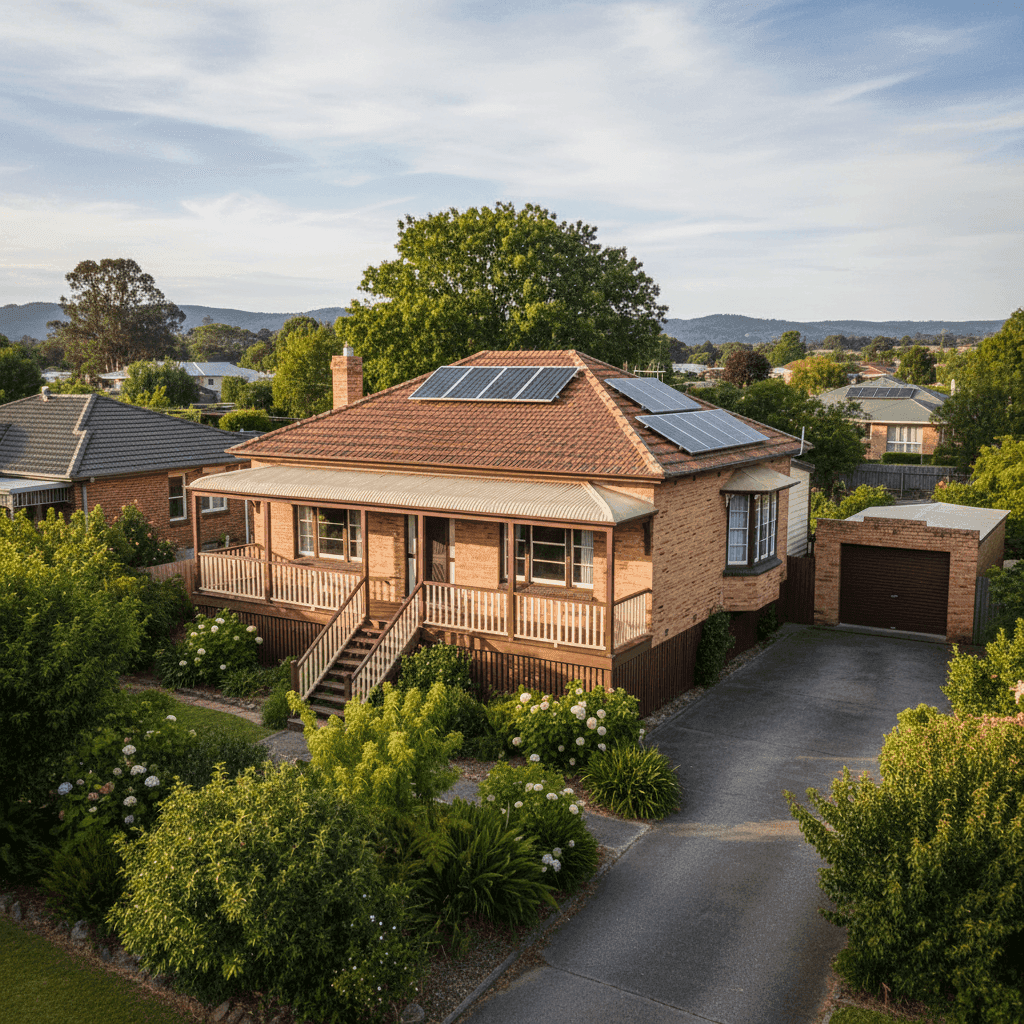

Deloraine is one of Tasmania's most picturesque towns — a heritage-rich community nestled in the Meander Valley, known for its historic streetscapes and cool-climate charm. If you own a free standing home here, understanding what drives your insurance premium can make a real difference to your back pocket. In this article, we analyse a recent home and contents insurance quote for a 4-bedroom, 3-bathroom property in Deloraine TAS 7304 to help you benchmark your own cover.

---

Is This Quote Fair?

The quote in question comes in at $6,598 per year (or $632/month) for combined home and contents cover, with a building sum insured of $2,529,000 and contents valued at $499,999. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — Above Average.

To put that in perspective, the suburb average premium for Deloraine sits at just $1,814 per year, with a median of $1,652. This quote is more than 3.6 times the local suburb average — a significant gap that warrants a closer look.

That said, it's important not to compare apples with oranges. The sum insured here is exceptionally high at $2.53 million for the building alone, which reflects a large, premium-quality home rather than a typical Deloraine property. When you're insuring a substantial asset with top-of-the-range fittings, a higher premium is to be expected. The contents cover of just under $500,000 also adds meaningfully to the overall cost.

Even so, if you're paying this kind of premium, it's worth shopping around to ensure you're getting the most competitive rate for your level of cover.

---

How Deloraine Compares

Here's how this quote stacks up against broader benchmarks, based on data from CoverClub's national insurance statistics:

| Benchmark | Average Premium |

|---|---|

| Deloraine (suburb average) | $1,814/yr |

| Deloraine (suburb median) | $1,652/yr |

| West Tamar LGA average | $2,040/yr |

| Tasmania average | $2,458/yr |

| Tasmania median | $2,272/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

| This quote | $6,598/yr |

Interestingly, Deloraine is actually a relatively affordable suburb to insure compared to both Tasmanian state averages and the national benchmark. The suburb's 25th percentile sits at $1,243/year and the 75th percentile at $1,930/year, suggesting that most homeowners in the area are paying well under $2,000 annually — a reflection of the region's lower risk profile and more modest property values.

The quote analysed here sits well above all of these benchmarks, driven primarily by the very high sum insured rather than any particular risk factor associated with the location itself.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated:

Construction Year (1930)

This is a pre-war home, and older properties often attract higher premiums due to the cost of restoring heritage-style features, sourcing period-appropriate materials, and the general complexity of older building structures. A 1930s double brick home in Deloraine may have significant heritage value — and that's reflected in the rebuild cost.

Double Brick Walls

Double brick construction is generally viewed favourably by insurers. It's durable, fire-resistant, and offers good structural integrity. This can work in your favour when it comes to pricing, compared to timber-framed or clad alternatives.

Tiled Roof

Terracotta or concrete tile roofs are considered a lower fire risk than Colorbond or corrugated iron in some assessments, though they can be more costly to repair or replace. Overall, tiles are a neutral-to-positive factor for insurers.

Stump Foundation & Elevation

The property sits on stumps and is elevated by less than 1 metre. Stump foundations are common in older Tasmanian homes and can introduce some vulnerability to subfloor moisture and pest damage, though the modest elevation here is unlikely to significantly increase flood risk.

Top-of-the-Range Fittings

This is one of the biggest premium drivers. High-end kitchen appliances, premium bathroom fixtures, bespoke joinery, and luxury flooring all push up the cost to rebuild — and therefore the sum insured. The $2.53 million building sum insured is a direct reflection of this.

Solar Panels & Ducted Climate Control

Both of these features add value to the property and increase the replacement cost. Solar panel systems — particularly larger installations — need to be explicitly covered, and ducted climate control systems are expensive to replace if damaged by fire, storm, or electrical fault.

No Pool, No Cyclone Risk

The absence of a pool removes a common liability risk, and Deloraine's location means cyclone cover is not a factor — both of which keep the premium lower than they might otherwise be.

---

Tips for Homeowners in Deloraine

1. Review Your Sum Insured Carefully

With a building sum insured of $2.53 million, it's essential to ensure this figure accurately reflects the cost to rebuild (not the market value) of your home. Over-insuring can mean unnecessarily high premiums, while under-insuring leaves you exposed. Consider getting a professional building valuation every few years, especially for older or heritage-style homes.

2. Shop Around — Especially at This Premium Level

At $6,598/year, even a 10–15% saving translates to $660–$990 back in your pocket annually. Use a comparison platform like CoverClub to get multiple quotes side by side. Insurers price risk differently, and a heritage double-brick home in regional Tasmania may be assessed very differently from one provider to the next.

3. Consider Your Excess Settings

Both the building and contents excesses are set at $1,000. Opting for a higher voluntary excess — say $2,000 or $2,500 — can noticeably reduce your annual premium. Just make sure you're comfortable covering that amount out of pocket in the event of a claim.

4. Bundle and Ask About Discounts

Many insurers offer discounts for bundling home and contents policies (which this quote already does), paying annually rather than monthly, or for security features like monitored alarms and deadbolts. It's always worth asking your insurer what discounts are available — they don't always advertise them upfront.

---

Compare Your Home Insurance Today

Whether you're a long-time Deloraine local or new to the area, it pays to regularly review your home insurance. Premiums shift, your property's value changes, and new providers enter the market. Head to CoverClub to compare home and contents quotes tailored to your property — and make sure you're not paying more than you need to.

For more localised data on insurance costs in your area, visit the Deloraine suburb stats page or explore Tasmania-wide insurance trends.