Deniliquin, nestled in the heart of the Riverina region of southern New South Wales, is a town with deep agricultural roots and a strong sense of community. For homeowners here, protecting a free standing home with the right insurance cover is an important financial decision — and understanding whether you're paying a fair premium can make a real difference. This article breaks down a real home and contents insurance quote for a three-bedroom, one-bathroom free standing home in Deniliquin (postcode 2710), and puts it in context with local, state, and national data.

---

Is This Quote Fair?

The annual premium for this property came in at $2,065 per year (or roughly $198 per month), covering both building (sum insured: $600,000) and contents ($50,000). The building excess is set at $2,000, with a $1,000 excess on contents.

Our independent price rating for this quote is FAIR — Around Average. That means the premium sits in a reasonable range for this type of property and location, neither a standout bargain nor an overpriced outlier.

To put that in perspective:

- The suburb average for Deniliquin is $2,961/yr, meaning this quote comes in roughly $896 below the local average — a meaningful saving.

- The suburb median sits at $2,177/yr, and this quote falls just below that midpoint, which reinforces the "around average" rating.

- The LGA average (Hay LGA) is $2,021/yr, and at $2,065, this quote is tracking very close to that benchmark.

So while the rating is "fair" rather than "great value," it's worth noting this premium is actually below both the suburb average and the suburb median — which is a solid result for a property with some unique characteristics (more on those below).

---

How Deniliquin Compares

When you zoom out to a broader view, Deniliquin looks like a relatively affordable place to insure a home. Here's how the numbers stack up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Deniliquin (2710) | $2,961/yr | $2,177/yr |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

The NSW state average of $9,528 is strikingly high — heavily influenced by coastal and flood-prone areas across the state, including parts of Sydney and Northern NSW that attract significantly elevated premiums. The NSW state insurance data reflects just how wide the spread can be across the state.

At the national level, the average of $5,347 is similarly pulled upward by high-risk zones around the country. Deniliquin sits well below both of these figures, even at the suburb average.

The local suburb data for Deniliquin shows a 25th percentile of $1,381/yr and a 75th percentile of $4,582/yr — a fairly wide spread across just 22 quotes sampled. This range suggests that insurer pricing in the area varies considerably, making it well worth comparing multiple quotes before committing.

---

Property Features That Affect Your Premium

This particular property has a number of characteristics that insurers weigh carefully when calculating a premium.

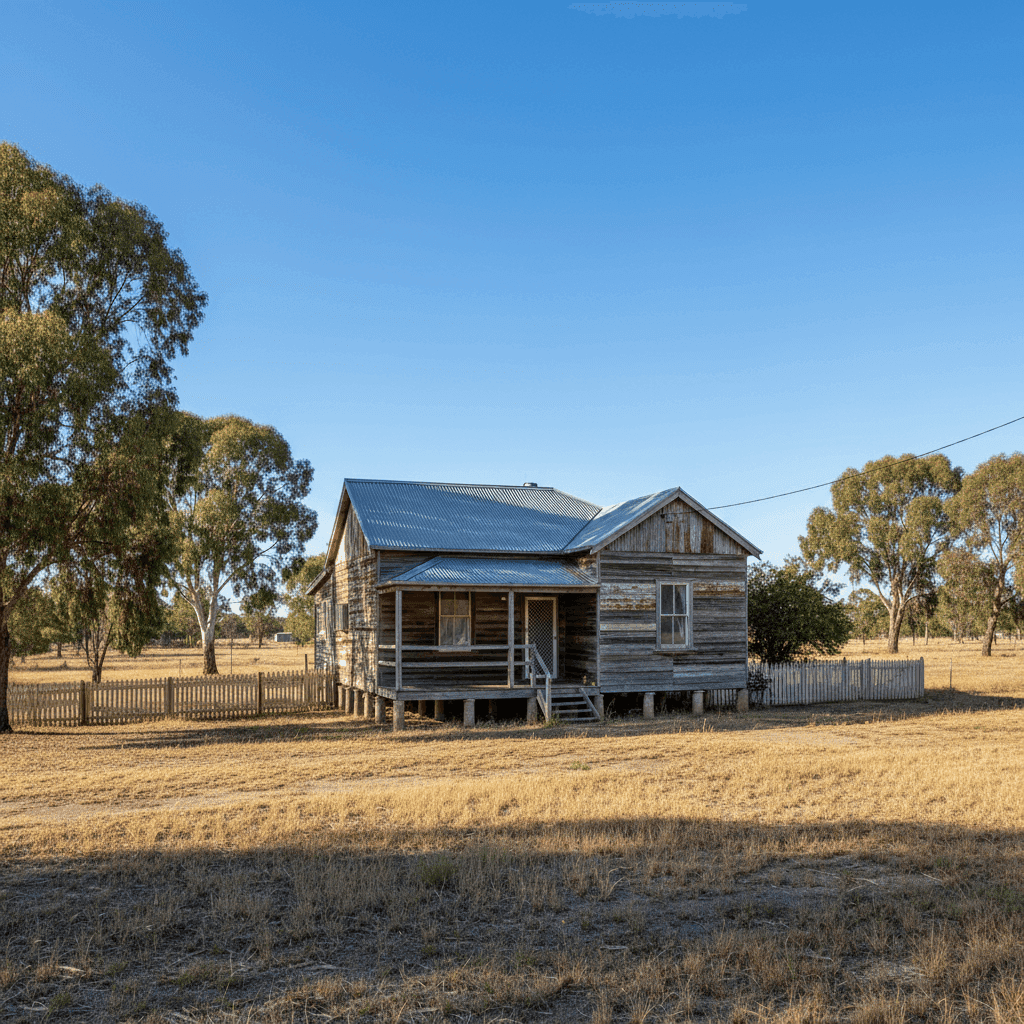

Age of construction (1870): This home is over 150 years old — a significant factor. Older homes often attract higher premiums due to the cost of sourcing period-appropriate materials, the potential for outdated wiring or plumbing, and the greater likelihood of wear-related claims. That said, many heritage homes in regional NSW have been well-maintained, and some insurers take a more nuanced view of older properties.

Foundation on stumps: A stump (or pier) foundation is common in older Australian homes, particularly in regional areas. While stumps provide good ventilation and can perform well in certain soil conditions, insurers may factor in the risk of subsidence, timber deterioration, or pest damage. It's worth ensuring your policy explicitly covers these risks.

Steel/Colorbond roof: This is generally viewed favourably by insurers. Colorbond roofing is durable, low-maintenance, and performs well in a range of weather conditions. It's also fire-resistant, which is a positive consideration in rural NSW.

External walls listed as "Other": Non-standard wall construction (which could include materials like weatherboard, fibrous cement, or heritage materials) can influence premiums. Insurers tend to price more cautiously when wall materials fall outside the standard brick or brick veneer categories.

Ducted climate control: The presence of ducted heating and cooling adds to the replacement value of the home and may modestly increase the building sum insured required — and by extension, the premium.

No pool, no solar panels: The absence of a pool and solar panels simplifies the risk profile slightly and removes two common sources of additional premium loading.

Building sum insured of $600,000: For a 130 sqm home in regional NSW, this is a relatively high sum insured. It's important to ensure this figure accurately reflects the cost to rebuild the home to its current standard — not its market value. Given the age and construction type, rebuild costs for a heritage property can be genuinely elevated.

---

Tips for Homeowners in Deniliquin

1. Don't rely on market value to set your sum insured In a regional town like Deniliquin, property market values can be quite different from rebuild costs. A heritage home built in 1870 may have a relatively modest market value but a very high rebuild cost due to the specialised labour and materials involved. Use a building cost calculator or consult a quantity surveyor to make sure you're not underinsured.

2. Shop around — the spread in Deniliquin is wide With quotes ranging from $1,381 to $4,582 in this postcode, there's clearly significant variation between insurers. The quote analysed here sits below the suburb median, but that doesn't mean it's the best available. Comparing quotes on CoverClub takes just a few minutes and could save you hundreds.

3. Review your excess settings This policy carries a $2,000 building excess and a $1,000 contents excess. Opting for a higher excess is one of the most straightforward ways to reduce your annual premium — but make sure the excess is an amount you could genuinely afford to pay at claim time.

4. Check for flood and water damage cover Deniliquin sits near the Edward River and has historically experienced flooding events. Make sure your policy explicitly includes flood cover, and review the Product Disclosure Statement (PDS) carefully to understand any exclusions or sub-limits that may apply to water damage claims.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for cover for the first time, it pays to compare. CoverClub makes it easy to see how your quote stacks up against real data from your suburb and beyond. Get a home insurance quote today and find out if you could be paying less for the same level of protection.