If you own a free standing home in Devereux Creek, QLD 4753, you already know that insurance is one of those non-negotiable costs — and in regional Queensland, it can be a significant one. This article breaks down a real home and contents insurance quote for a 2-bedroom property in the area, examines how it stacks up against local, state, and national benchmarks, and offers practical tips to help you get the best value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,613 per year (or $248/month) for combined home and contents cover, with a building sum insured of $269,000 and contents valued at $50,000. The building excess is $3,000 and the contents excess sits at $1,000.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up well when you dig into the numbers. The suburb median premium for Devereux Creek is $2,713/year, meaning this quote is sitting just $100 below the midpoint — a solid result. The suburb average is higher still at $3,513/year, which suggests a handful of more expensive quotes are pulling that figure upward. Landing below both the median and the average is a genuinely positive outcome for this homeowner.

It's worth noting that "fair" doesn't mean "the cheapest possible" — it means the price is competitive and reasonable for the risk profile of the property and location. Given the cyclone risk designation for this area (more on that below), achieving a sub-median premium is meaningful.

---

How Devereux Creek Compares

To put this quote in proper context, here's how Devereux Creek stacks up against broader benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $2,613/yr |

| Suburb median (Devereux Creek) | $2,713/yr |

| Suburb average (Devereux Creek) | $3,513/yr |

| Suburb 25th percentile | $2,363/yr |

| Suburb 75th percentile | $4,375/yr |

| LGA average (Mackay) | $8,458/yr |

| QLD state median | $3,903/yr |

| QLD state average | $9,129/yr |

| National median | $2,764/yr |

| National average | $5,347/yr |

A few things stand out here. First, the LGA average for Mackay is a striking $8,458/year — more than three times this quote. That figure is heavily influenced by higher-risk properties across the broader Mackay region, and it underscores just how variable premiums can be even within the same local government area.

Second, the Queensland state average of $9,129/year is extraordinarily high compared to the national average of $5,347/year. This reflects the outsized impact of cyclone, flood, and storm risk across much of Queensland. Devereux Creek sits in a cyclone risk zone, so it's notable that this particular quote tracks much closer to the national median ($2,764/year) than to the Queensland average.

You can explore more detailed premium data for this suburb at the Devereux Creek insurance stats page, or compare it against the broader Queensland insurance landscape and national benchmarks.

---

Property Features That Affect Your Premium

Every property has a unique combination of characteristics that insurers weigh when calculating risk. Here's how the features of this particular home come into play:

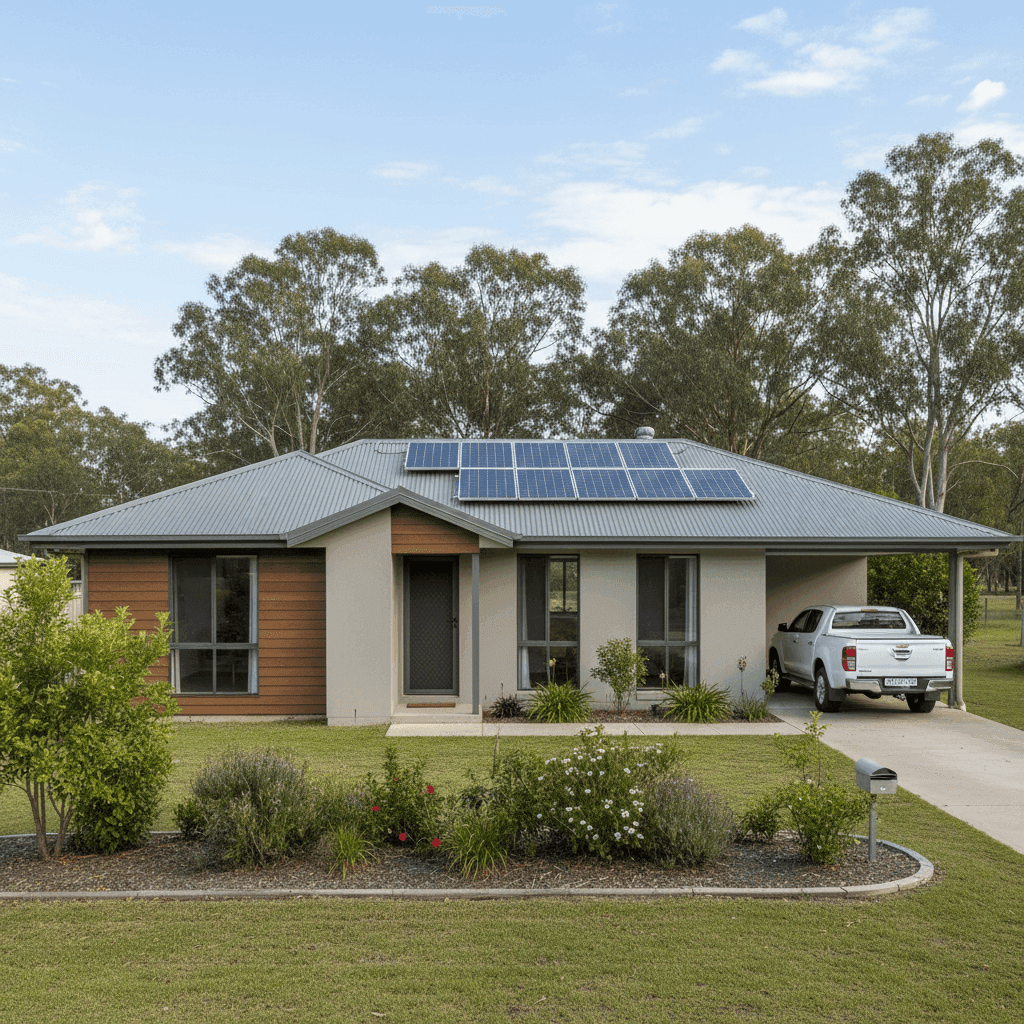

Cyclone Risk Area

This is arguably the single biggest factor for properties in and around Devereux Creek. Being designated a cyclone risk area means insurers apply specific loading to premiums to account for the potential for wind, rain, and structural damage during severe weather events. Homeowners in these zones should ensure their policy explicitly covers cyclone damage and review any applicable excess conditions.

Steel/Colorbond Roof

A Colorbond steel roof is generally viewed favourably by insurers. It's durable, fire-resistant, and performs well in high-wind conditions — all of which are relevant in this region. Compared to older tile or timber roofing, Colorbond can contribute to a more competitive premium.

Slab Foundation

A concrete slab foundation is considered low-risk by most insurers. It offers strong structural integrity and is less susceptible to subsidence or pest-related damage than timber stumps or piers, which can be a factor in older Queensland homes.

Solar Panels

The property includes solar panels, which adds a layer of complexity to the insurance picture. Solar systems represent a real asset value, and homeowners should confirm whether their policy covers panels under the building sum insured or as a separate item — and whether storm or hail damage is explicitly included.

Building Size and Age

At 139 sqm, this is a modestly sized home, which keeps the building sum insured ($269,000) proportionate and helps avoid over-insurance. Built in 2006, the property is relatively modern, which generally means it was constructed to more recent building codes — an advantage in cyclone-prone regions where standards have tightened over the decades.

Tile Flooring and Standard Fittings

Tile flooring is practical and cost-effective to replace, and standard-quality fittings mean the rebuild cost estimate is unlikely to be inflated by high-end fixtures. Both factors contribute to a more straightforward and reasonably priced sum insured.

---

Tips for Homeowners in Devereux Creek

1. Review Your Cyclone Excess Carefully

Many policies in cyclone-designated areas apply a separate, higher excess specifically for cyclone-related claims. This can be a flat dollar amount or a percentage of the sum insured. Make sure you understand what you'd actually be out of pocket in the event of a claim — the standard $3,000 building excess on this quote may or may not apply to cyclone events depending on the insurer's Product Disclosure Statement (PDS).

2. Check Your Solar Panel Coverage

Solar panels are increasingly common in Queensland, but not all policies treat them the same way. Confirm with your insurer whether your panels are covered under the building policy, whether there's a separate limit, and what events are included (particularly hail and storm damage, which are real risks in this region).

3. Don't Set and Forget Your Sum Insured

Building costs have risen sharply in recent years due to labour shortages and material price increases. A sum insured of $269,000 for a 139 sqm home may be appropriate today, but it's worth revisiting annually. Underinsurance is a significant risk — if your rebuild cost exceeds your sum insured, you'll be covering the gap yourself.

4. Compare Quotes at Renewal

The insurance market is competitive, and premiums can vary significantly between providers for the same property. The spread between the 25th percentile ($2,363/yr) and the 75th percentile ($4,375/yr) in Devereux Creek alone shows how much room there is between the cheapest and most expensive options. Shopping around at renewal — rather than simply auto-renewing — could save you hundreds of dollars a year.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for cover on a new property, comparing quotes is the smartest way to make sure you're not overpaying. Head to CoverClub to get a home and contents insurance quote tailored to your property in Devereux Creek — and see how your premium stacks up against the local market in seconds.