Diddillibah is a quiet, leafy suburb nestled in the Sunshine Coast hinterland — a region that blends semi-rural charm with easy access to the coast. It's an increasingly popular location for families seeking larger properties, and a six-bedroom free-standing home here is a significant asset worth protecting. But when it comes to home insurance, are residents getting a fair deal? We've analysed a recent home and contents quote for a property in Diddillibah to help you understand what's driving the cost — and whether there's room to do better.

---

Is This Quote Fair?

The quote in question comes in at $4,809 per year (or $454/month) for a combined home and contents policy. The building is insured for $1,600,000, with contents covered at $200,000, and both excesses are set at $5,000.

Our price rating for this quote is Expensive — above average for the suburb.

To put that in perspective, the suburb average for Diddillibah sits at $4,375/yr, with a median of $4,079/yr. This quote lands roughly $730 above the local median, which is a meaningful gap. It also exceeds the suburb's 75th percentile of $4,440/yr — meaning this premium is higher than at least three-quarters of comparable quotes we've seen in the area.

That said, context matters. This is a large, well-appointed property with a number of features that naturally push premiums upward (more on that below). The high building sum insured of $1.6 million is a significant factor on its own.

---

How Diddillibah Compares

Understanding your premium means looking beyond just your street. Here's how this quote stacks up across different benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $4,809/yr |

| Diddillibah suburb average | $4,375/yr |

| Diddillibah suburb median | $4,079/yr |

| Sunshine Coast LGA average | $7,249/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, this quote is actually well below the Sunshine Coast LGA average of $7,249/yr and comfortably under the Queensland state average of $9,129/yr — both of which are heavily influenced by high-risk coastal and cyclone-prone properties across the region.

Compared to the national average of $5,347/yr, this quote is also cheaper, which is a reassuring sign. However, it does sit above both the Queensland and national medians, suggesting that while the premium isn't extreme in a broader context, there may still be room to negotiate or shop around.

You can explore more local data on the Diddillibah suburb stats page, compare it to Queensland-wide figures, or benchmark against national home insurance statistics.

---

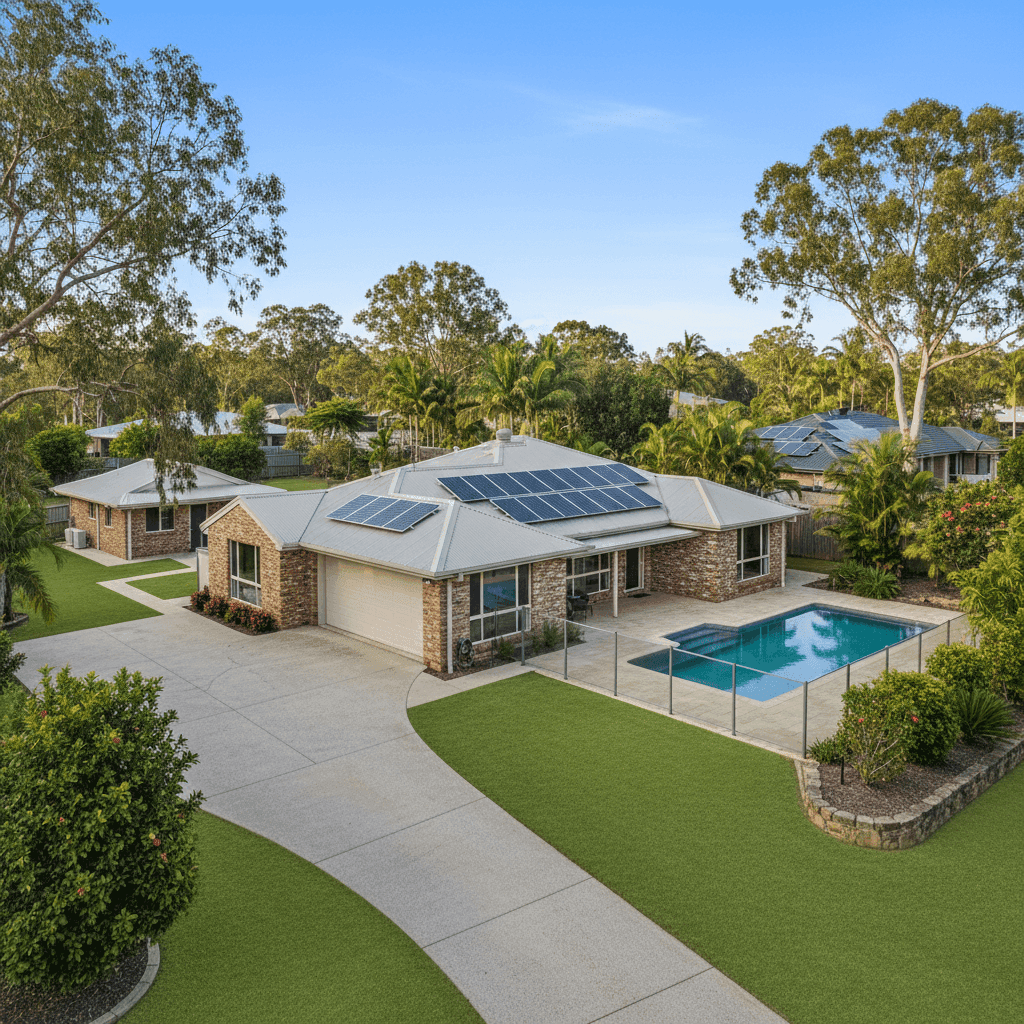

Property Features That Affect Your Premium

This isn't a standard three-bedroom brick home — and the premium reflects that. Several features of this property have a direct bearing on what insurers charge:

Size and Sum Insured

At 214 sqm and insured for $1,600,000, this is a substantial dwelling. A higher building sum insured means a greater potential payout for the insurer, which flows directly into your premium. For a six-bedroom, four-bathroom home, this rebuild value isn't unreasonable, but it's worth getting a professional building valuation periodically to ensure you're not over-insured.

Swimming Pool

Pools add value to a home but also add liability and maintenance risk from an insurer's perspective. Pool-related incidents — from structural damage to liability claims — can increase the cost of coverage.

Solar Panels

Solar panels are increasingly common on Sunshine Coast properties, but they do add complexity to a claim. Panels can be damaged by storms, hail, or falling debris, and their replacement cost needs to be factored into the building sum insured. Some insurers price this risk into the base premium.

Granny Flat

The presence of a granny flat effectively means insurers are covering an additional dwelling structure. This increases both the rebuild cost and the potential for claims, contributing to a higher premium.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace, and insurers take note. A full system failure following a storm or electrical surge can represent a significant claim.

Construction Type

Brick veneer walls with a steel/Colorbond roof on a concrete slab is generally considered a solid, lower-risk construction type. This likely works in the homeowner's favour compared to timber-framed or older construction methods. Colorbond roofing in particular is durable and performs well in storms.

No Cyclone Risk

Diddillibah falls outside designated cyclone risk zones, which is a meaningful premium saver compared to coastal or far-north Queensland properties. This is one reason the premium here is significantly below the QLD state average.

---

Tips for Homeowners in Diddillibah

If you're looking to get better value from your home insurance, here are four practical steps worth considering:

- Review your building sum insured annually. Construction costs have risen sharply in recent years, but so has the risk of over-insuring. Use a quantity surveyor or online rebuild calculator to ensure your $1.6M figure accurately reflects current rebuild costs — not just market value.

- Consider a higher excess to reduce your premium. Both excesses on this policy are set at $5,000. If you have the financial buffer to absorb a larger out-of-pocket cost in a claim, asking for a higher excess (say, $10,000) could bring your annual premium down noticeably.

- Bundle and ask for discounts. Many insurers offer discounts when you hold multiple policies — such as home, contents, and car insurance — with the same provider. It's worth asking your insurer directly what loyalty or bundling discounts apply.

- Compare quotes at renewal time. The home insurance market in Queensland is competitive, and premiums can vary significantly between providers for the same property. Don't auto-renew without checking alternatives — even a 10–15% saving on a $4,800 premium is real money back in your pocket.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for the first time, CoverClub makes it easy to see how your premium stacks up and find a better deal. Get a home insurance quote today and compare options tailored to your Diddillibah property — it only takes a few minutes and could save you hundreds each year.