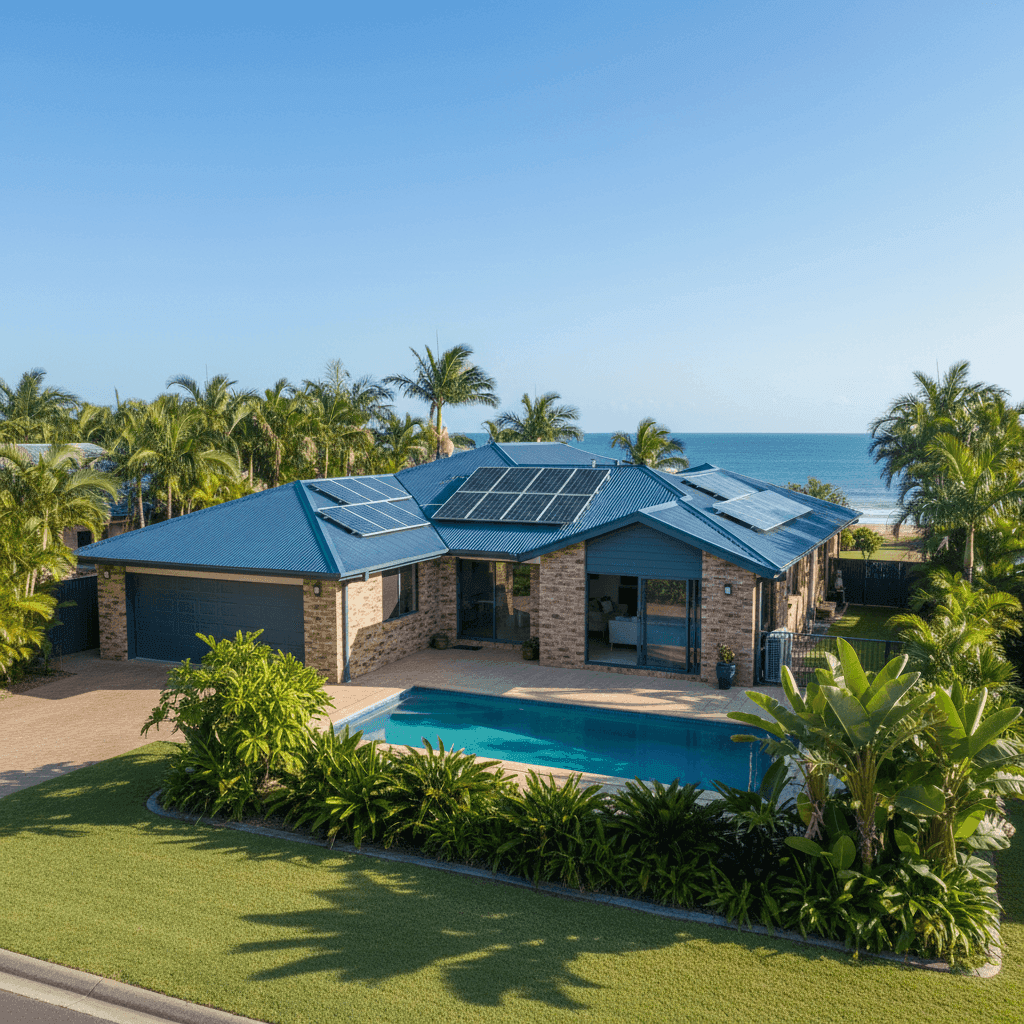

If you own a free standing home in Dingo Beach, QLD 4800, you already know that living along the Whitsunday coast comes with its fair share of beauty — and its fair share of insurance complexity. This analysis looks at a real home and contents insurance quote for a four-bedroom, two-bathroom brick veneer home in the area, breaking down whether the premium is competitive and what factors are driving the cost.

---

Is This Quote Fair?

The quote in question sits at $5,678 per year (or $544 per month) for combined home and contents cover, with a building sum insured of $1,001,000 and contents valued at $130,000. Both the building and contents excesses are set at $1,000.

Our price rating for this quote is Expensive (Above Average) — meaning it sits above what we'd typically expect for a comparable property in the area. That said, "above average" doesn't automatically mean the quote is unreasonable. Dingo Beach sits in a cyclone risk zone, and insurers price this in heavily. When you factor in a pool, solar panels, and ducted climate control — all of which add to replacement costs — a higher premium becomes easier to understand, even if it still warrants scrutiny.

The key question isn't just whether this quote is high in isolation, but whether you could get equivalent cover for meaningfully less elsewhere. That's where comparison becomes essential.

---

How Dingo Beach Compares

To put this quote in context, here's how it stacks up against suburb, state, and national benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $5,678/yr |

| Dingo Beach suburb average | $4,467/yr |

| Dingo Beach suburb median | $4,887/yr |

| Dingo Beach 25th percentile | $3,603/yr |

| Dingo Beach 75th percentile | $5,409/yr |

| LGA (Mackay) average | $8,458/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. The quote of $5,678 sits above the suburb's 75th percentile of $5,409, meaning it's more expensive than at least three-quarters of comparable quotes we've seen in Dingo Beach. That's a meaningful signal that there may be room to negotiate or shop around.

Interestingly, the QLD state average of $9,129 is dramatically higher than the state median of $3,903 — a sign that a small number of very high-risk or high-value properties are pulling the average up significantly. The Mackay LGA average of $8,458 tells a similar story. By those measures, this quote actually looks reasonable. But comparing against the suburb median of $4,887 suggests there's a gap worth investigating.

It's also worth noting the national average of $5,347 is close to this quote — so on a national scale, this isn't an outlier. The higher cost is largely a reflection of the elevated risk profile of coastal Queensland properties.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's a breakdown of the key factors at play:

Cyclone Risk Zone

This is the single biggest driver of premium costs in Dingo Beach. Properties in cyclone-prone areas attract significantly higher premiums due to the potential for catastrophic structural damage. Insurers apply cyclone sub-limits and specific excess conditions in many policies, so it's critical to read the Product Disclosure Statement (PDS) carefully.

Construction: Brick Veneer Walls & Steel/Colorbond Roof

Brick veneer is generally viewed favourably by insurers — it's durable and fire-resistant. The Colorbond steel roof is similarly well-regarded for cyclone-prone regions, as it's engineered to handle high wind loads better than some alternatives. This combination may actually be working in the homeowner's favour compared to, say, a timber-framed home with terracotta tiles.

Slab Foundation & Tiled Flooring

A concrete slab foundation is considered low-risk by most insurers — it's resistant to termites and flooding (to a degree), and doesn't carry the subsidence risk associated with some other foundation types. Tiles throughout are also a practical, durable choice that won't inflate the premium unnecessarily.

Pool, Solar Panels & Ducted Climate Control

These three features collectively increase the replacement value of the property and therefore the sum insured. A pool requires specific liability cover, solar panel systems can be costly to replace (especially rooftop arrays), and ducted climate control systems add tens of thousands of dollars to a full rebuild cost. All three are factored into the $1,001,000 building sum insured, which is a substantial figure.

Age of Construction (1985)

A home built in 1985 is approaching 40 years old. While it may have been well-maintained, older homes can present higher risk to insurers due to ageing electrical wiring, plumbing, and roofing materials. Some insurers also apply different pricing to homes built before modern cyclone-resistant building codes were introduced in Queensland (post-Cyclone Tracy reforms).

Building Size: 235 sqm

At 235 square metres, this is a reasonably large home. Rebuild costs scale with size, and at current construction rates in regional Queensland, a full rebuild of a home this size could easily exceed $1 million — so the sum insured appears appropriately calibrated.

---

Tips for Homeowners in Dingo Beach

1. Shop Around — Seriously

With the quote sitting above the suburb's 75th percentile, comparing at least three to five insurers is strongly advisable. Premiums for the same property can vary by thousands of dollars depending on how each insurer models cyclone risk, rebuild costs, and your specific features. Get a comparison quote at CoverClub to see what else is available.

2. Review Your Sum Insured Carefully

Over-insuring and under-insuring are both costly mistakes. A building sum insured of $1,001,000 for a 235 sqm home in regional QLD may be appropriate, but it's worth getting an independent building replacement cost estimate every few years — especially as construction costs have risen sharply since 2020. Ask your insurer how they calculate the sum insured and whether it includes demolition and debris removal costs.

3. Check Your Cyclone Excess

Many policies in cyclone-declared zones apply a separate, higher excess for cyclone-related claims — sometimes 1–2% of the sum insured, which on a $1,001,000 building could mean a $10,000–$20,000 out-of-pocket cost before your insurer pays a cent. Make sure you understand this before signing up, and factor it into your comparison.

4. Ask About Discounts for Safety Features

Some insurers offer discounts for cyclone-rated roofing, security systems, or homes that meet certain wind-resistance standards. Given this property has a Colorbond roof and is on a slab, it may qualify for some form of structural resilience discount. It's always worth asking.

---

Ready to Compare?

Whether you're renewing your policy or shopping for the first time, it pays to compare. CoverClub makes it easy to see how your home insurance quote stacks up against real data from properties just like yours in Dingo Beach and across Queensland. Start your comparison at CoverClub and make sure you're not paying more than you need to for the cover you deserve.