If you own a four-bedroom free standing home in Doreen, VIC 3754, you're living in one of Melbourne's fastest-growing outer northern suburbs — a leafy, family-friendly area that has seen significant residential development over the past two decades. Like any homeowner, keeping your biggest asset properly protected is a priority, and understanding whether you're paying a fair price for that cover is just as important. This article breaks down a real home and contents insurance quote for a property in Doreen, compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value.

---

Is This Quote Fair?

The quote in question comes in at $2,051 per year (or around $202 per month) for combined home and contents cover. This covers a building sum insured of $903,000 and contents valued at $248,000 — a substantial level of protection for a well-appointed family home.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Sitting above the suburb median of $1,769/yr but comfortably within the suburb's interquartile range ($1,385 to $2,224), this premium is neither a standout bargain nor cause for concern. It reflects the specifics of this property — including its size, features, and sum insured — without veering into overpriced territory.

It's worth noting that the building excess is set at $3,000, which is on the higher side. A higher excess typically reduces your annual premium, so if this quote were structured with a lower excess, you'd likely be paying more per year. The contents excess of $600 is more moderate and fairly standard across the market.

---

How Doreen Compares

To put this quote in proper context, let's look at how Doreen stacks up against broader benchmarks. You can explore the full data on our Doreen suburb stats page, Victoria state stats, and national insurance stats.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Doreen (3754) | $1,845/yr | $1,769/yr |

| Victoria (VIC) | $2,921/yr | $2,694/yr |

| Australia (National) | $2,965/yr | $2,716/yr |

| Nillumbik LGA | $3,693/yr | — |

A few things stand out here. First, Doreen premiums are notably lower than both the Victorian and national averages — by a significant margin. The state average is nearly $1,100 more per year than the suburb average, which suggests that Doreen, as a relatively modern residential suburb, carries less risk in the eyes of insurers compared to many other Victorian locations.

Second, the Nillumbik LGA average of $3,693/yr is striking. Nillumbik is a large local government area that encompasses everything from Doreen's newer estates through to bushland communities closer to the Yarra Ranges. Properties in more bush-adjacent parts of the LGA attract significantly higher premiums due to elevated bushfire risk — which pulls the LGA average well above what most Doreen residents will actually pay.

At $2,051/yr, this quote sits above the Doreen suburb average but well below the LGA, state, and national figures — a reasonable outcome given the property's size, features, and level of cover.

---

Property Features That Affect Your Premium

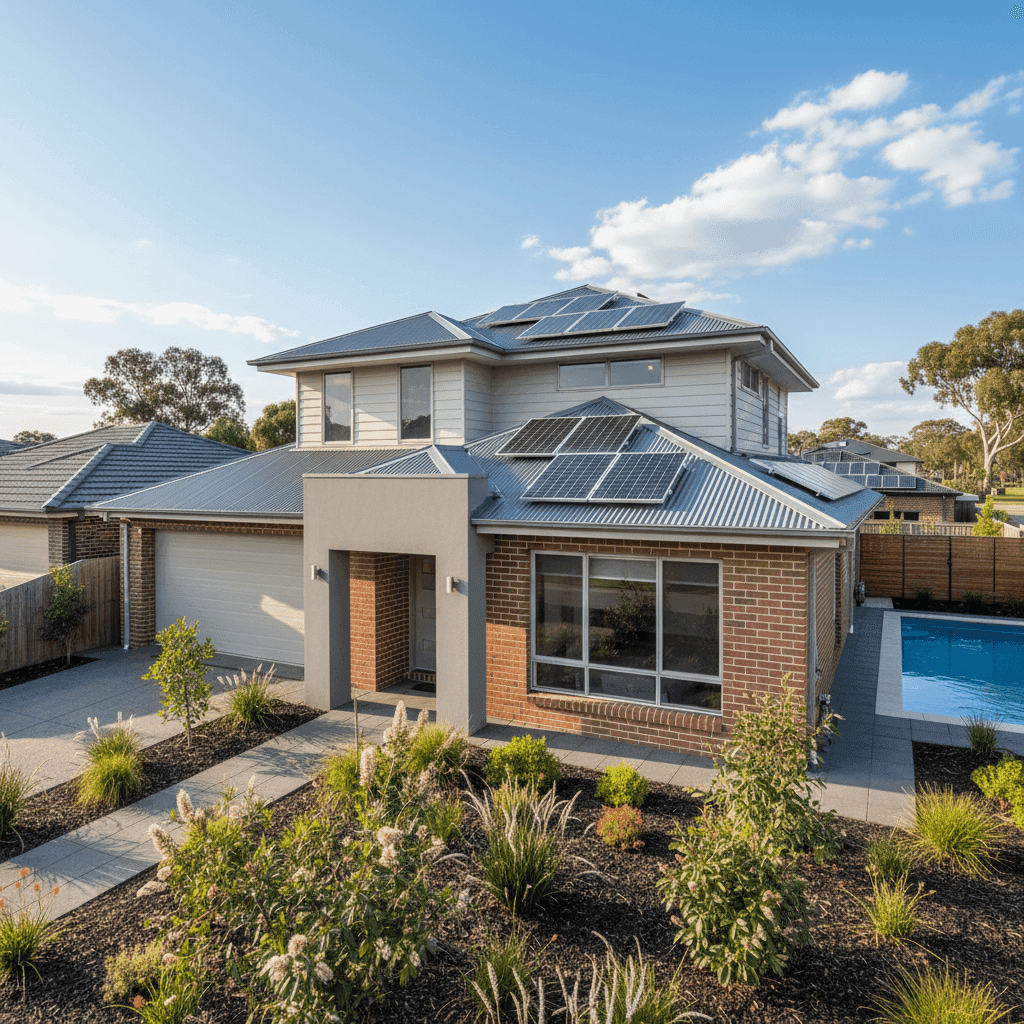

This is a 214 sqm home built in 2010 with several features that insurers consider carefully when pricing a policy.

Brick Veneer Walls & Colorbond Roof Brick veneer is one of the most common construction types in Australian suburban homes and is generally viewed favourably by insurers. It offers solid fire resistance compared to lightweight cladding, and Colorbond steel roofing is durable and low-maintenance. Together, these materials contribute to a more predictable risk profile.

Slab Foundation A concrete slab foundation, common in post-2000 construction, is typically associated with lower subsidence and movement risk than older pier-and-beam or strip footings — a minor but positive factor for insurers.

Timber & Laminate Flooring While stylish and popular, timber and laminate flooring can be more costly to repair or replace after water damage than tiles. This is reflected in contents and building valuations and may contribute marginally to the overall premium.

Swimming Pool A pool adds both value and liability to a property. Insurers factor in the cost of pool surrounds, equipment, and fencing when assessing building replacement costs, which contributes to the higher sum insured.

Solar Panels Solar panels are a fixed part of the building and are generally included in the building sum insured. With a system on the roof, it's important that your building cover adequately accounts for the cost of replacing panels — which can be significant.

Ducted Climate Control Ducted heating and cooling systems are expensive to install and repair. Their inclusion adds to the overall building replacement value, which is part of why a $903,000 sum insured is appropriate for a home of this specification.

No Cyclone Risk Doreen is not in a cyclone-prone area, which removes one of the more significant risk loadings that affect premiums in northern Australia. This helps keep the premium relatively contained.

---

Tips for Homeowners in Doreen

1. Review your building sum insured annually Construction costs in Victoria have risen sharply in recent years. A sum insured of $903,000 for a 214 sqm home with quality fittings is reasonable, but it's worth revisiting this figure each year — or after any renovations — to ensure you're not underinsured. Use a building cost calculator or speak with a quantity surveyor if you're unsure.

2. Consider your excess strategically This quote carries a $3,000 building excess. While a higher excess lowers your premium, it also means a larger out-of-pocket cost at claim time. If cash flow is a concern, it may be worth comparing quotes with a $1,000 or $2,000 excess to find a balance that suits your situation.

3. Don't overlook bushfire preparedness While Doreen's newer estates are not in a high Bushfire Attack Level (BAL) zone, parts of the broader Nillumbik area carry elevated risk. If your property is near grassland or remnant vegetation, check your BAL rating and ensure your policy includes adequate bushfire cover. Maintaining ember guards and clear gutters can also support any claim you need to make.

4. Compare quotes before renewing Insurers frequently adjust their pricing models, and loyalty doesn't always pay. With 115 quotes in our Doreen dataset ranging from $1,385 to over $2,224 per year, there's clear variation in the market. Even if your current quote is fair, it's worth comparing at renewal time to ensure you're not drifting into the upper end of the range without good reason.

---

Find a Better Deal with CoverClub

Whether you're renewing your existing policy or shopping for cover on a new home, CoverClub makes it easy to compare home and contents insurance quotes tailored to your property. Our data-driven approach means you can see exactly how your quote stacks up against real premiums paid by homeowners in your suburb, your state, and across Australia. Get a quote today and make sure you're getting the right cover at the right price.