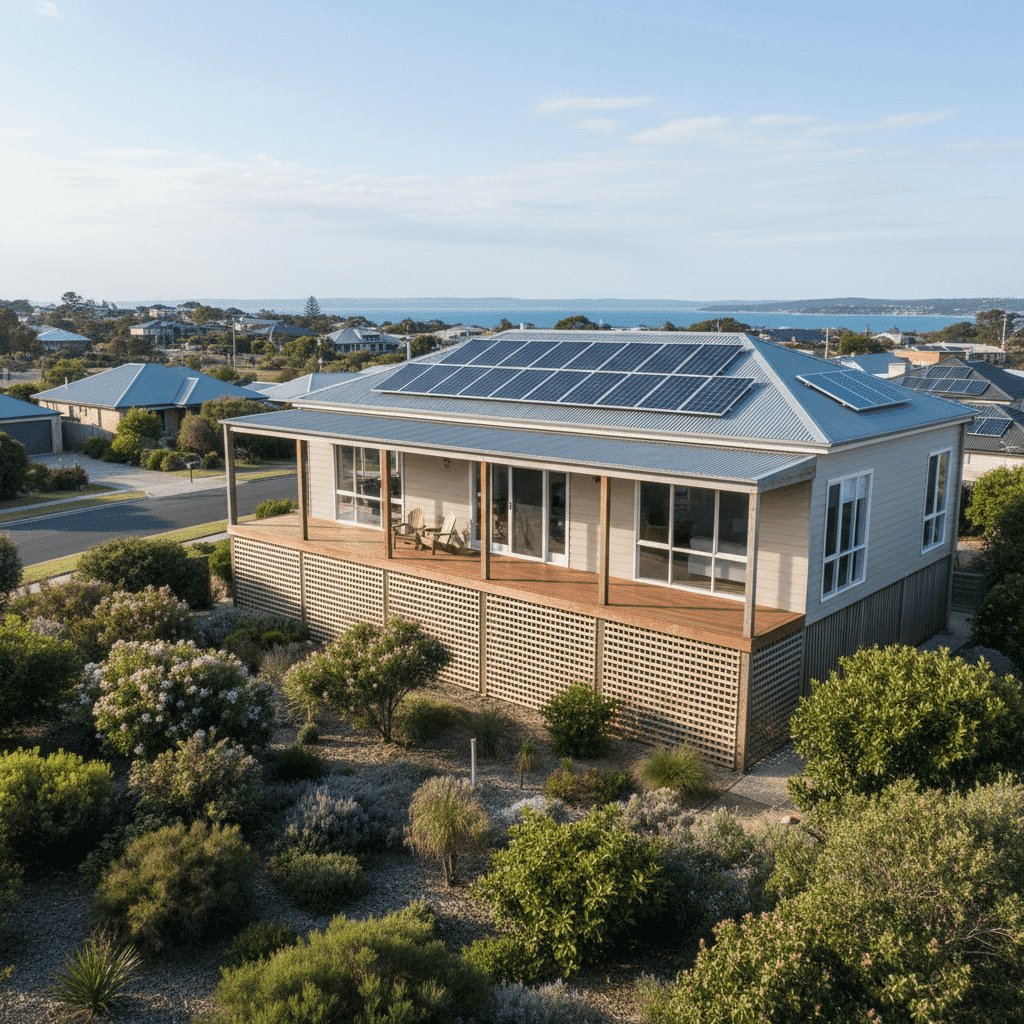

Dromana sits on the western shore of Port Phillip Bay on Victoria's Mornington Peninsula — a sought-after coastal suburb known for its relaxed lifestyle, stunning bay views, and a mix of long-term residents and holiday-home owners. Insuring a free standing home here comes with its own set of considerations, from coastal proximity to the age and construction of the dwelling. In this article, we analyse a real home and contents insurance quote for a four-bedroom property in Dromana and put it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question sits at $3,406 per year (or $326/month) for combined home and contents cover, with a building sum insured of $950,000 and contents valued at $450,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — Above Average.

To understand why, it helps to look at the local data. Based on 87 quotes collected for Dromana (postcode 3936), the suburb average premium is $2,183/yr and the median sits at $2,161/yr. This quote lands well above the 75th percentile for the suburb, which is $2,519/yr — meaning it's pricier than roughly three-quarters of comparable policies in the area.

That said, context matters. The building sum insured of $950,000 is on the higher end, and the combined contents value of $450,000 adds meaningful weight to the premium. A higher insured value naturally attracts a higher cost, so some of the price gap is expected. Even so, the gap between this quote and the suburb median ($1,245/yr difference) is significant enough to warrant shopping around.

---

How Dromana Compares

Zooming out beyond the suburb level paints an interesting picture:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Dromana (3936) | $2,183/yr | $2,161/yr |

| Mornington Peninsula LGA | $2,652/yr | — |

| Victoria (VIC) | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

Dromana actually comes in below the Victorian state average of $3,000/yr and well below the national average of $5,347/yr. The national average is heavily skewed by high-risk areas in Queensland and Western Australia — cyclone-prone regions, flood zones, and bushfire-affected communities — which inflates the figure considerably. The national median of $2,764/yr is a more reliable point of comparison for most Victorian homeowners.

At the state level, Victoria's average of $3,000/yr reflects a broad range of risk profiles, from inner-city Melbourne apartments to rural properties in high bushfire risk zones. Dromana's lower suburb average suggests it's generally considered a moderate-risk area by insurers.

The quote being analysed here exceeds both the suburb average and the Mornington Peninsula LGA average, which reinforces the "Expensive" rating — even if it's not dramatically out of step with the broader Victorian market.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing what insurers charge:

Construction era (1970s) Homes built around 1970 are now over 50 years old. While many have been renovated and well-maintained, insurers view older properties as carrying higher risk of ageing infrastructure — think plumbing, wiring, and structural wear. This can push premiums upward compared to newer builds.

Hardiplank/Hardiflex cladding Fibre cement cladding like Hardiplank is generally viewed favourably by insurers — it's non-combustible, durable, and resistant to rot and pests. This is a positive factor for the premium, particularly in areas with any bushfire or ember exposure risk.

Steel/Colorbond roof A Colorbond roof is another tick in the right column. It's fire-resistant, lightweight, and long-lasting. Insurers typically regard steel roofing more favourably than older materials like terracotta tiles or corrugated iron in poor condition.

Elevated foundation (at least 1 metre) Being elevated by at least one metre can be a double-edged sword. On the positive side, it reduces flood and stormwater inundation risk — important for a coastal suburb like Dromana. On the other hand, elevated homes can be more exposed to wind damage. Overall, the flood mitigation benefit tends to outweigh the wind exposure concern in most insurer assessments.

Solar panels Solar panels are an increasingly common feature but they do add to the replacement cost of the home. If they're not explicitly listed in the building sum insured, there could be a gap in cover. It's worth confirming with your insurer that solar panels are included in your policy.

Ducted climate control Ducted air conditioning is a significant fixed asset. Like solar panels, it contributes to the overall replacement cost of the building and should be factored into your sum insured calculation.

Timber and laminate flooring These materials can be more costly to replace than concrete or basic vinyl — particularly solid timber floors, which are labour-intensive to restore after water or fire damage.

Taken together, the property's features are a mix of risk-positive and cost-adding elements. The high-quality cladding and roof are working in the homeowner's favour, but the age of the home, elevated position, and the value of fixed assets like solar and ducted cooling all contribute to the final figure.

---

Tips for Homeowners in Dromana

1. Review your sum insured carefully A building sum insured of $950,000 is substantial. Make sure this figure reflects the rebuilding cost — not the market value — of your home. Overcooking the sum insured is a common and costly mistake. Use a building cost calculator or get a quantity surveyor's estimate to ensure you're not paying to insure more than you need to.

2. Shop around — seriously With a quote sitting above the 75th percentile for the suburb, there's a real chance a comparable policy is available for less. Compare quotes at CoverClub to see what other insurers are offering for the same level of cover. Even a $500/yr saving compounds significantly over time.

3. Check your contents value $450,000 in contents cover is generous. Walk through your home and consider whether that figure truly reflects your belongings. Many homeowners overestimate contents value, which means they're paying more in premiums than necessary. Equally, underinsurance is a real risk — so aim for accuracy rather than guessing in either direction.

4. Ask about discounts for security and safety features Some insurers offer premium reductions for homes with monitored alarm systems, deadbolts, and smoke detectors. If your Dromana home has any of these, make sure they're declared when you get a quote — they can make a meaningful difference.

---

Ready to Find a Better Deal?

If your current home insurance premium feels steep, you're not alone. The good news is that the market is competitive, and there's often a meaningful gap between what you're paying and what's available elsewhere. Start a free quote comparison at CoverClub and see how your premium stacks up — you might be surprised at the savings on offer. For more localised data on insurance costs in your area, check out the Dromana suburb stats page.