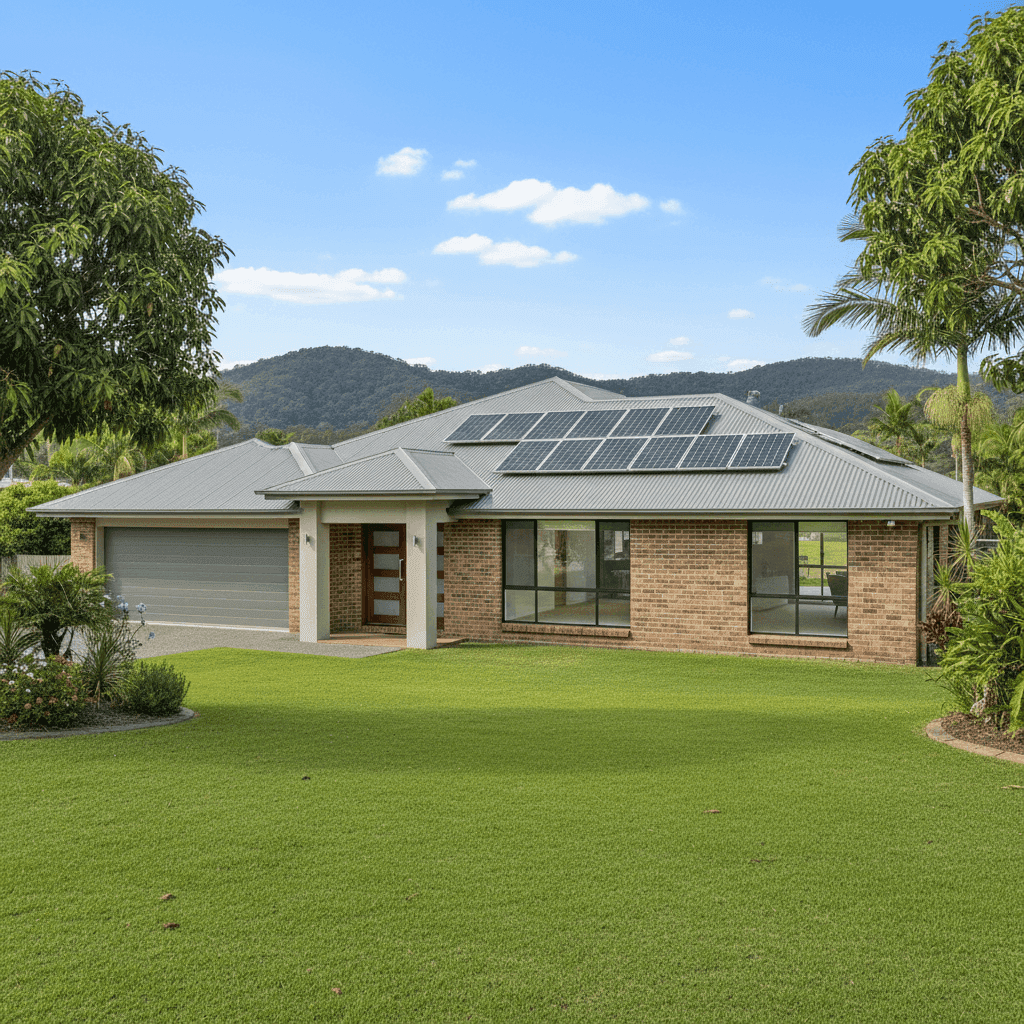

Nestled in the hinterland of the Sunshine Coast, Dulong (QLD 4560) is a quiet, semi-rural suburb known for its lush greenery, acreage properties, and relaxed lifestyle. For owners of free standing homes in the area, understanding what you should be paying for home and contents insurance is just as important as choosing the right policy. In this article, we break down a real insurance quote for a four-bedroom, two-bathroom brick veneer home in Dulong — and put the numbers into context using suburb, state, and national data.

---

Is This Quote Fair?

The quote in question comes in at $3,511 per year (or $330 per month) for combined home and contents cover, with a building sum insured of $859,000 and contents valued at $100,000. Both the building and contents excess are set at $2,000.

Our price rating for this quote is FAIR — Around Average.

That rating holds up well under scrutiny. The quote sits below the suburb average of $4,388 per year and also below the suburb median of $4,158 per year. In fact, at $3,511, this premium falls between the 25th percentile ($3,381/yr) and the median for Dulong — meaning it's comfortably in the lower half of what most homeowners in this postcode are paying. That's a solid outcome, particularly given the relatively high building sum insured.

It's worth noting that the suburb sample for Dulong is based on 11 quotes, so while the data is directionally useful, a larger dataset would give even greater confidence. That said, the positioning of this quote within the local range is encouraging.

---

How Dulong Compares

To appreciate how this quote stacks up, it helps to zoom out and look at the broader picture. You can explore the full data on the Dulong suburb stats page, the Queensland state stats page, and the national stats page.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Dulong (4560) | $4,388/yr | $4,158/yr |

| Sunshine Coast LGA | $7,249/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. Queensland's average premium of $9,129 per year is extraordinarily high — nearly double the national average. This is largely driven by the prevalence of cyclone-prone and flood-affected regions across the state, which push premiums up dramatically in high-risk postcodes. However, the Queensland median of $3,903 tells a more grounded story: most Queensland homeowners who aren't in extreme-risk zones are paying something closer to that figure.

The national average of $5,347 is similarly skewed by high-risk regions, while the national median of $2,764 reflects what a typical Australian homeowner pays. At $3,511, this Dulong quote sits above the national median but well below both the state and national averages — a reasonable position for a well-built home in a relatively low-risk suburb.

The Sunshine Coast LGA average of $7,249 may raise eyebrows, but this figure is pulled up by coastal and flood-prone properties within the broader LGA. Dulong's hinterland location and non-cyclone classification mean it doesn't carry the same risk loading as beachside or low-lying suburbs.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour from an insurance pricing perspective.

Brick veneer construction is generally well-regarded by insurers. It offers solid fire resistance and structural durability, which can help keep premiums lower compared to timber-framed or weatherboard homes.

Steel/Colorbond roofing is another positive. Colorbond is lightweight, durable, and highly resistant to the elements — including the intense summer storms that can affect South East Queensland. Insurers tend to view it favourably compared to older tile roofs, which can be more susceptible to storm damage.

A concrete slab foundation provides stability and reduces the risk of subsidence or pest-related structural damage, both of which can be costly claims. Combined with the 1990 construction year, this property sits in a sweet spot — old enough to have proven structural integrity, but not so old that wear and tear becomes a significant concern.

Timber and laminate flooring can be a consideration in the event of water damage claims, as these materials may require full replacement rather than simple repair. It's worth ensuring your contents and building cover adequately accounts for this.

The presence of solar panels is worth flagging. Most home insurance policies cover solar panels as part of the building, but it's important to confirm this with your insurer — particularly regarding storm damage, inverter failure, or panel theft. With a building sum insured of $859,000, there should be adequate headroom to cover the panels, but always verify the specifics of your policy wording.

Ducted climate control adds value to the property and is generally covered under building insurance, but again, confirm that the system is explicitly included and that the sum insured reflects its replacement cost.

The absence of a pool simplifies the risk profile slightly — pools can add to both the liability and maintenance considerations that insurers factor in.

---

Tips for Homeowners in Dulong

1. Review your building sum insured regularly. At $859,000, the building sum insured here is substantial. Construction costs have risen significantly in recent years across Queensland, so it's worth getting an independent building valuation every two to three years to ensure you're not underinsured. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Confirm solar panel coverage explicitly. Solar systems are a meaningful investment. Before renewing your policy, call your insurer and ask specifically how your panels are covered — including storm damage, accidental breakage, and theft. Not all policies treat them the same way.

3. Don't overlook storm and water damage cover. Even though Dulong is not classified as a cyclone risk area, the Sunshine Coast hinterland does experience heavy rainfall and severe thunderstorms during summer. Make sure your policy includes adequate storm and rainwater ingress cover, and understand any exclusions around gradual water damage.

4. Compare quotes at renewal time. A "fair" rating is a good sign, but the insurance market changes constantly. Premiums can shift significantly from year to year, and loyalty doesn't always pay. Use a comparison tool like CoverClub to benchmark your renewal quote against the market before you commit.

---

Compare Your Own Quote

Whether you're a Dulong local or just exploring your options, CoverClub makes it easy to see how your home insurance premium stacks up. Enter your address at coverclub.com.au to get a personalised comparison and find out if you're paying a fair price — or if there's a better deal waiting for you.