If you own a free standing home in Dunoon, NSW 2480, you're probably wondering whether your home insurance premium is competitive — or whether you're quietly overpaying year after year. This article breaks down a real home and contents insurance quote for a three-bedroom property in Dunoon, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The annual premium for this quote comes in at $3,462 per year (or $332/month), covering both building (sum insured: $372,000) and contents ($50,000), each with a $1,000 excess.

Our price rating for this quote is FAIR — Around Average. That assessment is backed up by the data. The suburb average for Dunoon sits at $3,391/yr, meaning this quote is only about $71 above the local average — a difference of roughly 2%. That's well within normal variation and certainly not a red flag.

What does this mean in practice? You're not getting a bargain, but you're also not being stung. For a 1975-built home with fibro asbestos walls — a construction type that carries additional risk considerations — landing near the suburb average is a reasonable outcome. Insurers price older homes with non-standard materials more conservatively, so a "fair" rating here is genuinely encouraging.

That said, "fair" doesn't mean you can't do better. The suburb's 25th percentile sits at just $1,746/yr, which shows that some homeowners in Dunoon are securing significantly cheaper cover. The difference could come down to lower sum insured values, higher excesses, or simply shopping around more aggressively.

---

How Dunoon Compares

To put this quote in proper context, it helps to zoom out and look at the broader picture. Here's how Dunoon stacks up:

| Benchmark | Premium |

|---|---|

| This Quote | $3,462/yr |

| Dunoon Suburb Average | $3,391/yr |

| Dunoon Suburb Median | $3,098/yr |

| NSW State Average | $9,528/yr |

| NSW State Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

| Ballina LGA Average | $23,241/yr |

A few things stand out immediately. First, the NSW state average of $9,528/yr is dramatically higher than what Dunoon homeowners are paying — but this is largely driven by high-risk coastal and flood-prone areas pulling the average up. The NSW median of $3,770/yr is a far more representative figure, and this quote sits comfortably below that.

Second, the Ballina LGA average of $23,241/yr is eye-catching. Ballina is one of Australia's most flood-affected regions, and the LGA average is heavily skewed by properties in flood zones closer to the coast. Dunoon, sitting inland in the Northern Rivers hinterland, benefits from a more favourable risk profile than many of its LGA neighbours.

Against the national average of $5,347/yr, this quote looks quite reasonable. Even compared to the national median of $2,764/yr — which reflects cheaper properties and lower-risk locations across the country — the Dunoon quote isn't wildly out of step given the property's age and construction.

You can explore more local data on the Dunoon suburb stats page, compare against NSW state benchmarks, or check out national home insurance statistics for a broader perspective.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on what insurers charge. Understanding them can help you have more informed conversations when shopping for cover.

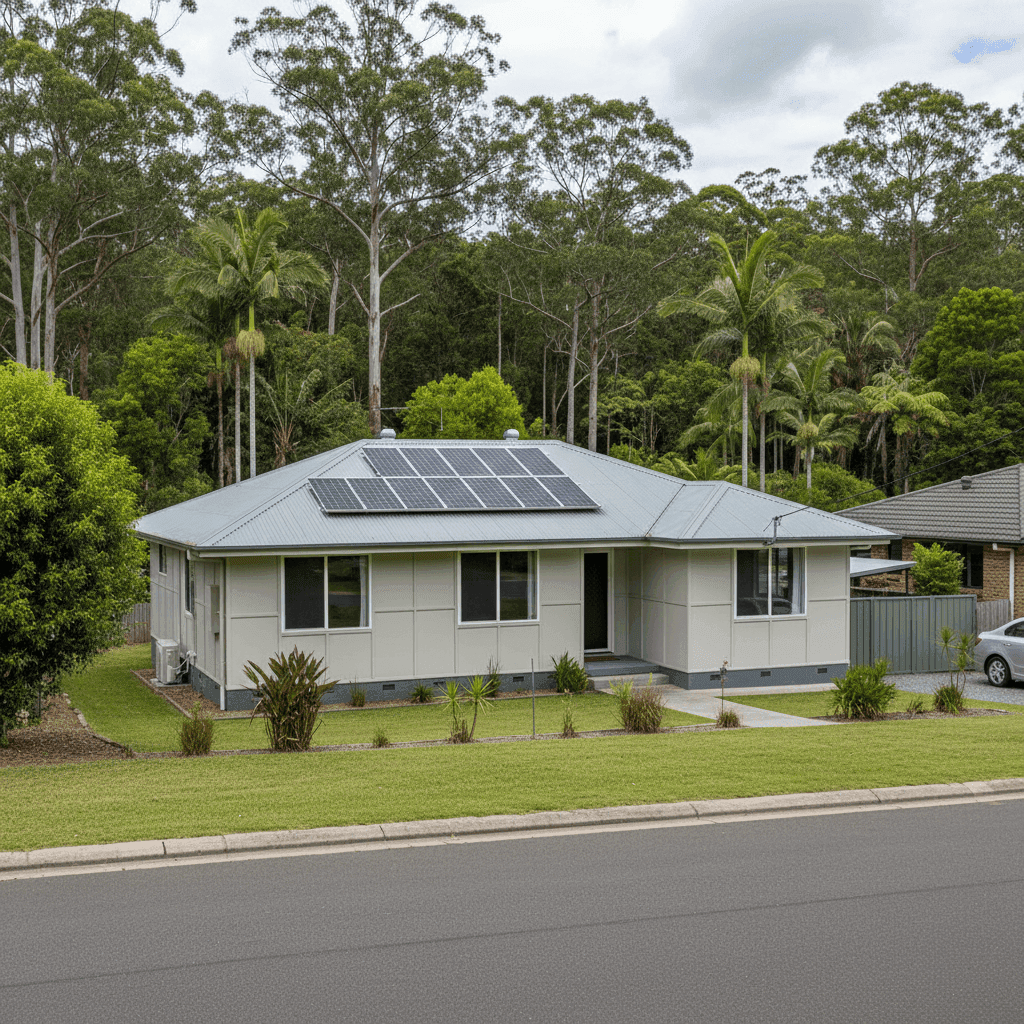

Fibro Asbestos Walls This is arguably the most significant risk factor for this property. Homes built with fibro asbestos — common in Australian construction through the 1950s to late 1970s — are more expensive to insure because repairs or rebuilds must comply with strict asbestos handling regulations. Labour and disposal costs are considerably higher, which is reflected in the rebuild estimate and, by extension, the premium.

Construction Year: 1975 At 50 years old, this home sits in a bracket that insurers treat with caution. Older homes may have ageing plumbing, electrical wiring, and structural elements that increase the likelihood of a claim. Some insurers apply loadings for homes over a certain age, particularly when combined with non-standard wall materials.

Steel/Colorbond Roof This is a genuine positive. Colorbond roofing is durable, fire-resistant, and widely regarded by insurers as a lower-risk roofing material compared to tiles or older iron sheeting. It handles the Northern Rivers' heavy rainfall well and is less susceptible to storm damage.

Slab Foundation A concrete slab foundation is generally viewed favourably by insurers — it's stable, resistant to termite ingress, and less prone to subsidence than some alternatives.

Solar Panels The property has solar panels installed. Most home insurance policies cover solar panels as part of the building sum insured, but it's worth confirming this with your insurer. Some policies have sub-limits or exclusions for solar systems, particularly for mechanical or electrical breakdown.

Ducted Climate Control Ducted air conditioning systems are a fixed building fixture and should be included in the building sum insured. At $372,000, the building cover here appears to account for the full cost of rebuilding a 130 sqm home with these features — though it's always worth reviewing your sum insured annually to ensure it keeps pace with rising construction costs.

---

Tips for Homeowners in Dunoon

1. Review Your Sum Insured Every Year Construction costs in regional NSW have risen sharply over the past few years. A sum insured that was accurate in 2022 may be significantly underinsured today. Use a building cost calculator or speak to a local builder to sense-check whether $372,000 is still a realistic rebuild figure for a 130 sqm home with fibro asbestos walls in the Northern Rivers.

2. Confirm Your Asbestos Cover Not all policies treat asbestos the same way. Some insurers include asbestos removal and disposal costs within the standard rebuild, while others apply sub-limits or exclusions. Before renewing, ask your insurer specifically how they handle asbestos in a total loss scenario — the answer could significantly affect your real-world coverage.

3. Check What's Covered for Your Solar System Solar panels are a meaningful asset. Confirm whether your policy covers them for accidental damage, storm damage, and theft — and whether there's a sub-limit that might leave you underinsured if the system needs replacing.

4. Shop Around at Renewal With 18 quotes sampled in the Dunoon suburb data, there's clearly a competitive market here. The gap between the 25th percentile ($1,746/yr) and the 75th percentile ($4,017/yr) is substantial, which means the insurer you choose — and the excess you select — can make a significant difference to your annual outlay. Don't simply auto-renew; compare at least two or three quotes before committing.

---

Compare Your Home Insurance Today

Whether you're renewing your existing policy or insuring a Dunoon property for the first time, it pays to see what the market looks like before you commit. CoverClub makes it easy to compare home and contents insurance quotes side by side, so you can make a confident, informed decision.