East Hills is a quiet, leafy suburb nestled in Sydney's south-west, sitting within the Canterbury-Bankstown local government area. It's a predominantly residential pocket known for its established homes, generous block sizes, and proximity to the Georges River. For owners of free standing homes in this area, understanding what drives your home insurance premium — and whether you're paying a fair price — can make a meaningful difference to your household budget.

This article breaks down a real home and contents insurance quote for a 4-bedroom, 2-bathroom free standing home in East Hills, and puts the numbers into context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $1,985 per year (or $195/month) for combined home and contents cover, with a building sum insured of $718,000 and contents valued at $100,000. The building excess is $2,000 and the contents excess $1,000.

Based on CoverClub's pricing data, this quote is rated Expensive — above average for the area.

To put that in perspective: the average premium across the small sample of quotes we've recorded for East Hills (postcode 2213) sits at $1,301/year, with a median of just $946/year. The quote here lands well above the suburb's 75th percentile of $1,483/year — meaning it's pricier than at least three-quarters of comparable quotes in the area.

That said, context matters. The building sum insured of $718,000 is a significant figure, and the inclusion of contents cover at $100,000 adds to the overall cost. A higher sum insured naturally attracts a higher premium, so part of what appears expensive may simply reflect appropriate coverage levels rather than an overpriced policy.

Still, the gap between this quote and the suburb median is notable — roughly $1,039/year more. That's money worth investigating.

---

How East Hills Compares

One of the more interesting findings here is how favourably East Hills stacks up against broader benchmarks. While this particular quote is above the local average, East Hills as a suburb is considerably cheaper to insure than most of New South Wales.

| Benchmark | Average Premium |

|---|---|

| East Hills (suburb) | $1,301/yr |

| Canterbury-Bankstown (LGA) | $1,910/yr |

| NSW (state) | $3,801/yr |

| Australia (national) | $2,965/yr |

The NSW state average of $3,801/year is nearly three times the East Hills suburb average — a striking difference. Even the national average of $2,965/year is more than double the local median. This suggests East Hills is a relatively low-risk suburb from an insurer's perspective, benefiting from its distance from coastal storm surge zones, no cyclone risk, and a generally stable built environment.

You can explore detailed pricing data for East Hills and postcode 2213 on the CoverClub suburb stats page.

It's worth noting that the sample size for East Hills is currently five quotes, so the suburb averages should be treated as indicative rather than definitive. As more data comes in, these figures will become more robust.

---

Property Features That Affect Your Premium

Several characteristics of this particular property are worth examining through an insurance lens.

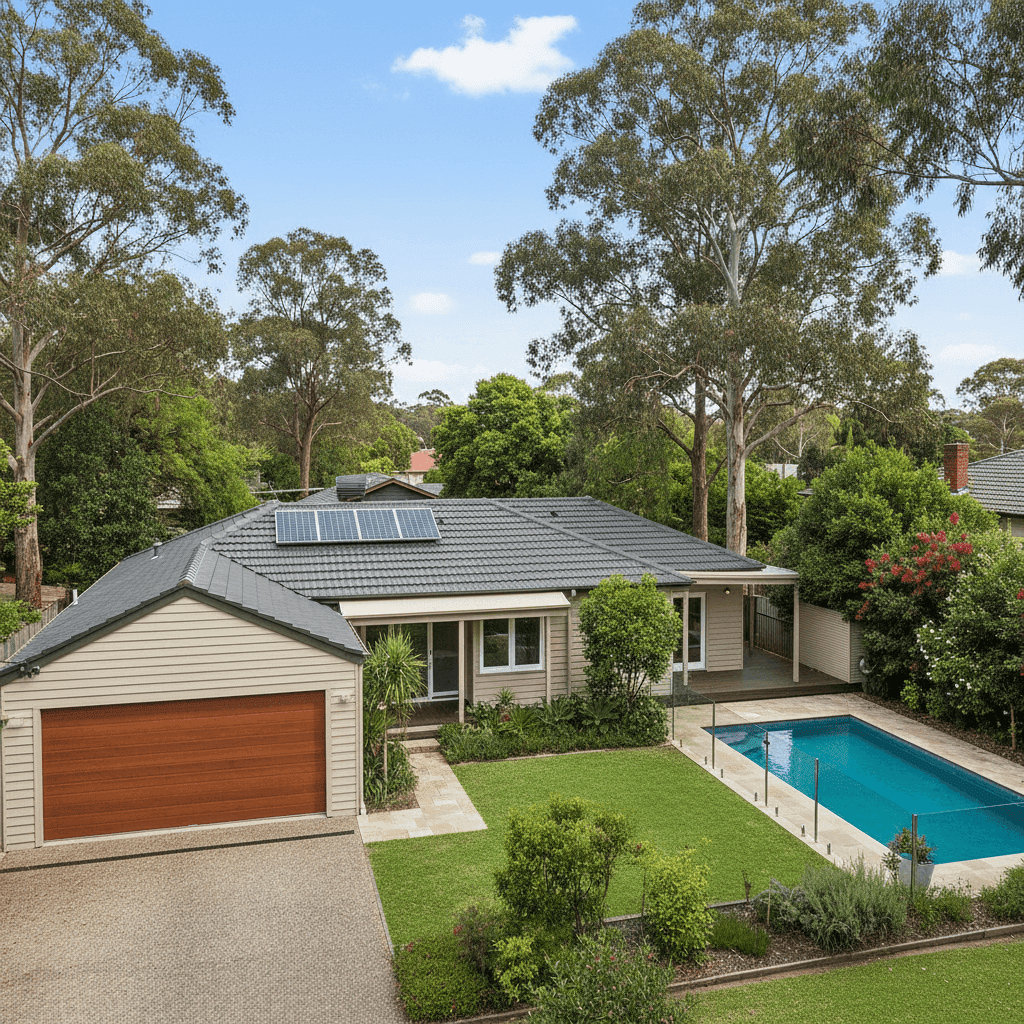

Weatherboard timber walls are one of the most significant risk factors for insurers. Timber is more susceptible to fire spread, rot, and pest damage compared to brick veneer or full brick construction. Homes built with weatherboard cladding typically attract higher premiums, and this is likely contributing meaningfully to the cost of this quote.

Stump foundations are common in older Sydney homes, particularly those built in the 1970s and 80s. While stumps offer good ventilation and can be advantageous in flood-prone areas, they can also be a source of movement and structural concern over time — particularly if timber stumps have deteriorated. Insurers may factor this into their risk assessment.

The 1984 construction year means this home is over 40 years old. Older homes often have ageing electrical wiring, plumbing, and roofing materials that can increase the likelihood of a claim. Some insurers apply age-related loadings to properties of this vintage.

Tiled roof is generally viewed positively by insurers — tiles are durable, fire-resistant, and long-lasting compared to Colorbond or older fibrous cement roofing.

Timber and laminate flooring throughout the home is a standard feature and unlikely to significantly affect the premium on its own.

The swimming pool adds liability exposure to the policy. Pool-related incidents — whether accidental injury or property damage — are a consideration for insurers, and pool ownership can nudge premiums upward.

Solar panels are increasingly common and most insurers now include them under building cover, but they do add to the overall insured value of the property and can be a factor in premium calculations.

---

Tips for Homeowners in East Hills

If you're a homeowner in East Hills reviewing your insurance costs, here are four practical steps worth considering:

- Shop around — seriously. The gap between the cheapest and most expensive quotes in East Hills is substantial. With a suburb median of $946/year and this quote sitting at $1,985/year, there's clearly a wide range of pricing in the market. Using a comparison tool like CoverClub takes just a few minutes and could reveal significantly cheaper options for equivalent cover.

- Review your sum insured carefully. A building sum insured of $718,000 for a 235 sqm home in East Hills is on the higher end. Make sure your sum insured reflects the actual cost to rebuild — not the market value of the land and property. Overinsuring can mean you're paying more than necessary, while underinsuring leaves you exposed. Consider getting a professional building replacement cost assessment.

- Consider your excess settings. A $2,000 building excess is relatively high. Some homeowners opt for a higher excess in exchange for a lower premium, which can be a smart strategy if you're unlikely to make small claims. Conversely, if cash flow is a concern, a lower excess with a slightly higher premium might suit you better.

- Maintain your weatherboard cladding. From an insurance perspective, keeping your timber walls in good condition — painted, sealed, and free from rot or pest damage — reduces the risk of a claim and may support a better premium at renewal. Some insurers also offer discounts for homes with updated electrical systems, so if your wiring is original to 1984, it may be worth investigating a switchboard upgrade.

---

Compare Your Options with CoverClub

Whether you're renewing your existing policy or shopping for cover for the first time, it pays to compare. CoverClub makes it easy to see how your quote stacks up against real data from your suburb, your state, and across Australia. Get a quote today and find out if you're getting a fair deal — or if there's a better option waiting for you.