If you own a free standing home in East Kurrajong, NSW 2758, you've probably wondered whether you're paying a fair price for home and contents insurance — or whether you're leaving money on the table. This article breaks down a real quote for a three-bedroom, two-bathroom brick veneer home in the suburb, compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The annual premium for this quote comes in at $3,965 per year (or $373 per month), covering a building sum insured of $847,000 and contents valued at $189,000. Our price rating for this quote is CHEAP — below average for the area.

To put that in perspective: the suburb average for East Kurrajong sits at $7,243 per year, with a median of $7,044. That means this quote is coming in at roughly 45% below the local average — a significant saving for a homeowner in this postcode.

Even when stacked against the broader NSW state average of $3,801 per year, this premium is still sitting comfortably below the mark. For a property with a relatively high building sum insured of $847,000, that's a strong result.

The building excess is set at $5,000 and the contents excess at $2,000, which are on the higher side. It's worth noting that a higher excess is one of the key reasons a premium can appear more competitive — you're essentially agreeing to cover more of any claim yourself in exchange for lower ongoing costs.

---

How East Kurrajong Compares

Understanding where your suburb sits within the broader insurance landscape helps you gauge whether a quote is genuinely competitive or simply average for a cheaper region.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,965 |

| East Kurrajong Suburb Average | $7,243 |

| East Kurrajong Suburb Median | $7,044 |

| East Kurrajong 25th Percentile | $4,356 |

| LGA (Lithgow) Average | $5,454 |

| NSW State Average | $3,801 |

| NSW State Median | $3,410 |

| National Average | $2,965 |

| National Median | $2,716 |

A few things stand out here. East Kurrajong's suburb average of $7,243 is substantially higher than both the national average of $2,965 and the NSW state average. This suggests that homes in this postcode are generally assessed as higher risk by insurers — likely due to a combination of bushfire exposure, rural-fringe location, and the types of properties in the area.

The fact that this quote lands below the suburb's 25th percentile ($4,356) is particularly telling. It means this premium is cheaper than at least 75% of quotes observed in the area — a genuinely strong result.

It's worth noting that the suburb sample size is six quotes, so the local data should be treated as indicative rather than definitive. That said, the pattern is consistent with what we see across the broader Lithgow LGA, where the average sits at $5,454 per year.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium — both positively and negatively.

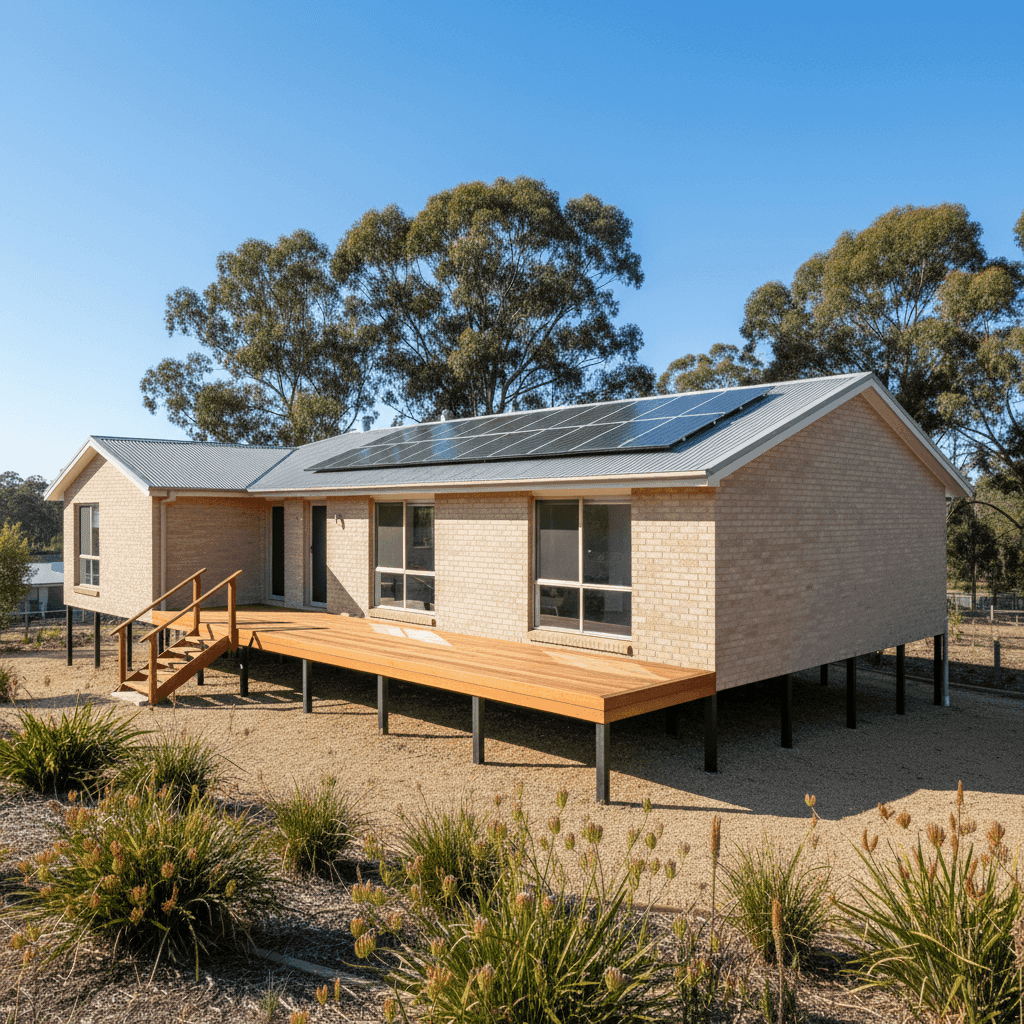

Brick Veneer Walls & Colorbond Roof Brick veneer is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to weatherboard or fibre cement cladding. Paired with a steel Colorbond roof, this combination is considered low-maintenance and resilient — both traits that can work in your favour at renewal time.

Stump Foundation & Timber/Laminate Flooring The home is elevated on stumps by less than one metre, which introduces some nuance. Stump foundations can be more susceptible to subfloor moisture and pest damage over time, and some insurers apply a modest loading to account for this. The timber and laminate flooring is a consideration for contents cover, particularly if water damage is involved.

Solar Panels Solar panels are increasingly common on Australian homes, but they do add complexity to a building insurance policy. Panels need to be adequately covered under the building sum insured, and some insurers have specific conditions around storm or hail damage to solar systems. It's worth confirming your policy explicitly covers the panels — and that the $847,000 building sum insured accounts for their replacement value.

No Pool, No Cyclone Risk The absence of a swimming pool removes a common source of liability and maintenance-related claims. East Kurrajong is also outside designated cyclone risk zones, which keeps premiums more predictable compared to properties in northern Queensland or coastal NT.

Construction Year: 2005 A home built in 2005 benefits from relatively modern building standards, which generally translates to better structural integrity and compliance with contemporary fire and safety codes. This is a positive factor when insurers assess risk.

---

Tips for Homeowners in East Kurrajong

1. Review Your Building Sum Insured Annually Construction costs have risen sharply across NSW in recent years. A sum insured of $847,000 may have been accurate when the policy was first written, but it's worth reassessing whether it would genuinely cover a full rebuild today — including demolition, site clearance, and professional fees. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Understand Your Excess Trade-Off This quote carries a $5,000 building excess and a $2,000 contents excess. While these higher excesses are contributing to the lower premium, make sure you're comfortable covering that amount out of pocket in the event of a claim. If cash flow is a concern, it may be worth comparing quotes with a lower excess to understand the premium difference.

3. Confirm Solar Panel Coverage Given the property has solar panels installed, check your policy's product disclosure statement (PDS) carefully. Some policies treat solar panels as part of the building, others as a separate item, and a few have exclusions or sublimits. Make sure your coverage is explicit and sufficient.

4. Compare at Renewal — Every Year The East Kurrajong suburb data shows a wide spread between the 25th percentile ($4,356) and 75th percentile ($10,091), which tells you there's significant variation in what insurers charge for similar homes in this area. Loyalty doesn't always pay — comparing quotes annually is one of the simplest ways to avoid overpaying.

---

Get a Quote for Your East Kurrajong Home

Whether you're reviewing an existing policy or shopping for cover for the first time, it pays to compare. CoverClub makes it easy to see how your premium stacks up against real data from your suburb, your state, and across Australia. Get a quote today at CoverClub and find out if you're paying a fair price — or if there's a better deal waiting for you.

For more local insurance data, visit the East Kurrajong suburb stats page or explore NSW home insurance benchmarks to see how your area compares.