If you own a free standing home in East Mackay, QLD 4740, you've probably noticed that home insurance doesn't come cheap. This article breaks down a real home and contents insurance quote for a four-bedroom property in the suburb, compares it against local, state, and national benchmarks, and offers practical advice for keeping your premiums as manageable as possible.

---

Is This Quote Fair?

The quote in question comes in at $8,699 per year (or $827/month) for combined home and contents cover, with a building sum insured of $949,000 and contents valued at $50,000. The building excess is $5,000 and the contents excess is $1,000.

Our price rating for this quote is EXPENSIVE — above average for the East Mackay suburb. Compared to the suburb average of $4,939/yr, this quote sits roughly 76% higher than what other East Mackay homeowners are typically paying. It also exceeds the suburb's 75th percentile of $5,813/yr, meaning it's more expensive than at least three-quarters of comparable quotes in the area.

That said, context matters. A higher-than-average sum insured ($949,000 for the building alone) will naturally push premiums upward. Rebuilding a 214 sqm home in regional Queensland isn't cheap, and insurers price accordingly. Still, the gap is significant enough to warrant shopping around.

---

How East Mackay Compares

Understanding where East Mackay sits in the broader insurance landscape helps put this quote in perspective.

| Benchmark | Premium |

|---|---|

| This quote | $8,699/yr |

| East Mackay suburb average | $4,939/yr |

| East Mackay suburb median | $4,881/yr |

| Mackay LGA average | $8,458/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

(Based on 16 quotes sampled in the East Mackay suburb.)

A few things stand out here. While this quote is expensive relative to the suburb average, it's actually slightly below the Queensland state average of $9,129/yr. This tells us that home insurance across QLD is broadly elevated — largely driven by cyclone exposure, flooding risk, and the high cost of rebuilding in regional areas.

Zooming out further, Queensland premiums are dramatically higher than the national median of $2,764/yr, which reflects the disproportionate natural hazard risk that North Queensland homeowners face compared to their southern counterparts.

The Mackay LGA average of $8,458/yr is also telling — it's very close to this quote, suggesting that the broader Mackay region commands consistently high premiums, regardless of the specific suburb.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on what insurers charge. Here's how they break down:

🌀 Cyclone Risk Area

This is arguably the single biggest factor. East Mackay sits within a designated cyclone risk zone, which significantly increases the likelihood of a major claim. Insurers build this risk into their base rates for the region, and it's a primary reason why Mackay-area premiums are so much higher than the national median.

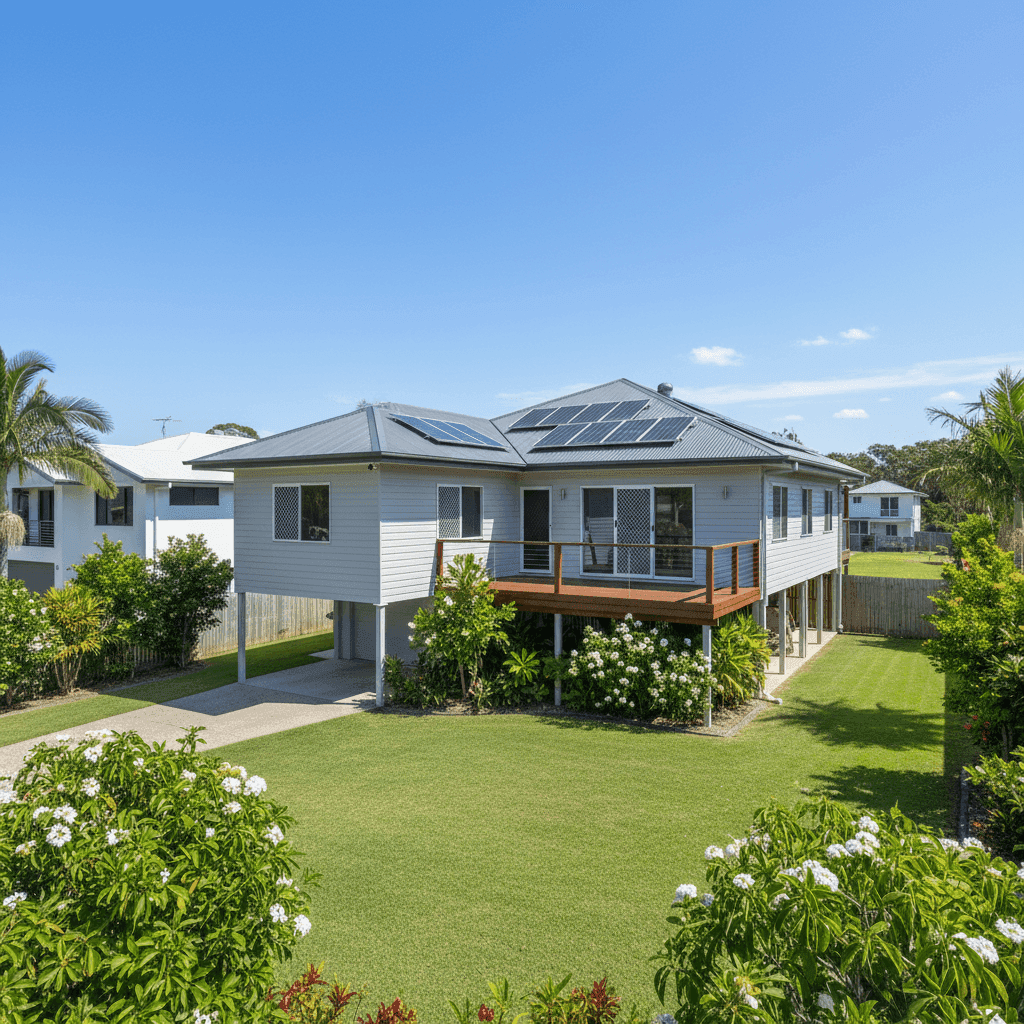

🏠 Construction: Hardiplank/Hardiflex Walls & Colorbond Roof

Fibre cement cladding (Hardiplank/Hardiflex) is generally viewed favourably by insurers — it's durable, fire-resistant, and holds up well in high-wind events. The steel Colorbond roof is similarly regarded as a resilient choice, particularly in cyclone-prone areas. These construction materials may help moderate the premium somewhat compared to older or less robust alternatives.

🏗️ Pole Foundation

The property sits on pole (or stump) foundations, which is common for older Queensland homes. While elevated homes can perform well in flood events, pole foundations can be a variable factor in insurer assessments — some view them as more vulnerable in high-wind scenarios, while others see the elevation as a flood mitigation benefit.

📅 Built in 1980

At over 40 years old, this home falls into an age bracket that can attract higher premiums. Older properties may have outdated electrical wiring, plumbing, or structural elements that increase the risk of certain claims. Keeping up with maintenance and having recent renovation records can help demonstrate the home's condition to insurers.

☀️ Solar Panels

The presence of solar panels adds to the insured value of the property and can slightly increase premiums, as panels themselves represent a significant asset to protect. Ensure your policy explicitly covers solar panels — not all standard policies do by default.

🪵 Timber/Laminate Flooring

Timber flooring in a cyclone and storm-prone region can be susceptible to water damage. This is worth factoring into your contents and building cover, particularly if you're in an area prone to localised flooding or storm surge.

---

Tips for Homeowners in East Mackay

1. Review Your Sum Insured Carefully

A building sum insured of $949,000 is substantial. Make sure this figure reflects the actual cost to rebuild your home (not its market value), including demolition, debris removal, and current construction costs in regional QLD. Overinsuring inflates your premium unnecessarily, while underinsuring leaves you exposed. Use a qualified quantity surveyor or an online rebuild calculator to validate this figure annually.

2. Compare Multiple Quotes

With only 16 quotes sampled in the suburb, the local market data is limited — but the spread between the 25th percentile ($4,154/yr) and this quote ($8,699/yr) is enormous. That gap represents real money. Get a quote through CoverClub to compare multiple insurers side-by-side and find a more competitive rate.

3. Consider Your Excess Strategy

This policy carries a $5,000 building excess — which is quite high. A higher excess generally lowers your annual premium, but it means you'll need to cover more out of pocket in the event of a claim. Assess your financial buffer honestly: if a $5,000 outlay would be a stretch, it may be worth paying a slightly higher premium for a lower excess.

4. Ask About Cyclone Mitigation Discounts

Some insurers offer discounts for homes that have been cyclone-rated or retrofitted to meet modern wind resistance standards. If your home has had any structural upgrades — roof tie-downs, improved window protection, or cyclone-rated shutters — ask your insurer whether these qualify for a premium reduction. The Insurance Council of Australia's Cyclone Testing Station can provide guidance on eligible improvements.

---

Ready to Find a Better Deal?

Whether this quote is the right fit or you're looking for something more competitive, comparing your options is always worthwhile. At CoverClub, we make it easy to see how your premium stacks up and explore alternatives — all in one place.

👉 Compare home insurance quotes in East Mackay today and see if you can do better.

You can also explore detailed premium data for your area on the East Mackay suburb stats page, or browse Queensland-wide insurance trends for broader context.