East St Kilda is one of Melbourne's most sought-after inner-southern suburbs — a leafy, character-rich pocket of the Glen Eira local government area known for its heritage streetscapes, proximity to the bay, and a strong mix of period homes and modern renovations. For owners of a free standing home here, getting the right home and contents insurance at a fair price is an important part of protecting what is likely a significant asset.

This article breaks down a recent home and contents insurance quote for a 5-bedroom, 3-bathroom free standing home in East St Kilda (VIC 3183), and puts the numbers in context so you can judge whether your own premium stacks up.

---

Is This Quote Fair?

The quoted annual premium for this property is $1,656 per year (or approximately $162 per month), covering a building sum insured of $981,000 and contents valued at $50,000. Both the building and contents excess are set at $5,000.

Our pricing analysis rates this quote as CHEAP — below average for this type of property and location. That's a meaningful finding. A below-average premium doesn't necessarily mean reduced cover; it can simply reflect a combination of favourable property characteristics, a competitive insurer, and a location that carries lower-than-typical risk.

To put it plainly: if you received this quote, you're doing well compared to most Victorian homeowners insuring a similar property.

---

How East St Kilda Compares

Understanding where a premium sits relative to broader benchmarks helps you make a genuinely informed decision. Here's how this quote measures up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,656 |

| Glen Eira LGA Average | $1,828 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

The quote comes in $172 below the Glen Eira LGA average, which is already one of the more affordable LGAs in Victoria. Against the Victorian state average of $3,000/yr, this premium is roughly 45% cheaper — a substantial saving on an annual basis.

Zooming out further, the national average sits at $5,347/yr, which reflects the outsized impact of high-risk regions — particularly cyclone-prone areas of Queensland and Northern Australia — on the overall figures. Even against the more representative national median of $2,764, this quote is still notably competitive.

You can explore suburb-specific insurance data for East St Kilda at the CoverClub East St Kilda stats page.

---

Property Features That Affect Your Premium

Insurance underwriters assess dozens of variables when pricing a policy. Several features of this particular property work in the homeowner's favour — and a couple are worth understanding in more detail.

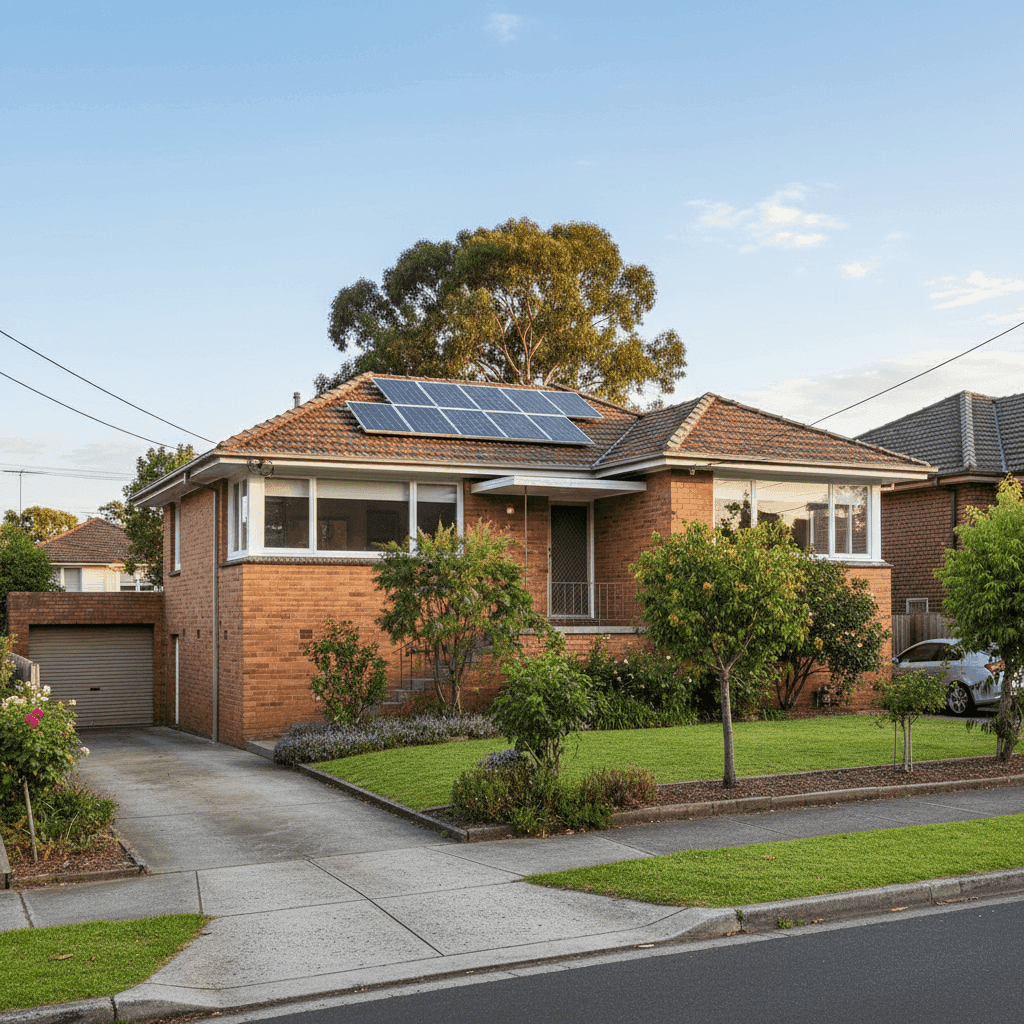

Brick Veneer Walls and Tiled Roof

Brick veneer construction is widely regarded by insurers as a solid, fire-resistant building material. Combined with a tiled roof, this property presents a relatively low risk profile from a structural standpoint. Compared to weatherboard or fibre cement homes — which are more common in older Melbourne suburbs — brick veneer tends to attract more favourable premiums.

Built in 1955

The 1955 construction date is worth noting. Older homes can sometimes attract higher premiums due to ageing plumbing, wiring, or roofing. However, a well-maintained mid-century brick home with a slab foundation is generally considered structurally sound. Insurers may still ask about renovations or upgrades to electrical and plumbing systems, so keeping records of any works completed is advisable.

Slab Foundation

A concrete slab foundation is typically viewed positively by insurers. It reduces the risk of subsidence and eliminates the underfloor moisture issues that can affect homes on stumps or piers — particularly relevant in parts of Melbourne with reactive clay soils.

Timber and Laminate Flooring

Timber and laminate floors add to the contents and building replacement cost but are standard for a home of this era and quality level. The standard fittings rating applied here keeps the premium grounded — high-end or bespoke finishes can push premiums considerably higher.

Solar Panels

This property includes solar panels, which are increasingly common across Melbourne. Solar systems are generally covered under building insurance, but it's worth confirming with your insurer that the panels and inverter are explicitly included in your sum insured. Given the replacement cost of a quality solar system, under-insuring this component could be a costly oversight.

Ducted Climate Control

Ducted heating and cooling systems are a significant fixed asset in any home. Like solar panels, these should be factored into your building sum insured. They don't typically increase premiums dramatically, but they do contribute to the overall replacement cost — which at $981,000 for a 286 sqm home appears appropriately calibrated.

No Pool, No Cyclone Risk

The absence of a swimming pool removes a common liability and maintenance risk factor. And being located in metropolitan Melbourne, this property sits well outside any cyclone risk zone — a major driver of elevated premiums in northern and coastal parts of Australia.

---

Tips for Homeowners in East St Kilda

1. Review your building sum insured annually Construction costs in Melbourne have risen sharply over recent years. A sum insured set even two or three years ago may no longer reflect the true cost of rebuilding your home. Use a building cost calculator or speak with a quantity surveyor to ensure your $981,000 cover remains adequate — particularly for a 286 sqm home with period features.

2. Confirm solar panels and ducted systems are covered Ask your insurer explicitly whether your solar panel system and ducted climate control are included in the building sum insured. Some policies treat these as standard inclusions; others require them to be listed separately. Don't assume — check the Product Disclosure Statement (PDS).

3. Consider your excess carefully Both the building and contents excess on this policy are set at $5,000. A higher excess typically lowers your premium, but it also means a larger out-of-pocket cost at claim time. Make sure the excess level you choose is genuinely affordable if you needed to make a claim tomorrow.

4. Compare at renewal time Even if your current premium is competitive, the insurance market shifts each year. Insurers reprice based on claims data, reinsurance costs, and risk modelling. Setting a reminder to compare quotes 30 days before your renewal date is one of the simplest ways to avoid gradual premium creep.

---

Get a Quote for Your East St Kilda Home

Whether you're a first-time buyer or a long-term resident, it pays to know what the market looks like before you commit to a policy. CoverClub makes it easy to compare home and contents insurance quotes tailored to your property and location. Start your free quote today and see how your premium measures up.