If you own a free standing home in Eatons Hill, QLD 4037, you've probably wondered whether you're paying a fair price for home insurance — or whether there's a better deal waiting. This article breaks down a real home and contents insurance quote for a four-bedroom, brick veneer property in the suburb, and puts the numbers in context using suburb, state, and national data.

---

Is This Quote Fair?

The quote in question comes in at $2,229 per year (or $214/month) for combined home and contents cover, with a building sum insured of $808,000 and contents valued at $152,000. Both the building and contents excesses are set at $1,000.

Our price rating for this quote is FAIR — Around Average, which is a reasonable result for a property of this size and specification. It's not the cheapest on the market, but it's also well within the normal range for the suburb. Homeowners who see a "Fair" rating can generally feel comfortable that they're not being significantly overcharged, though there's always room to shop around and potentially trim costs.

To put this in perspective: the quote sits just $69 below the suburb average of $2,298/yr and $175 below the suburb median of $2,404/yr. That means this particular premium is performing slightly better than what most comparable Eatons Hill properties are paying — a modest but meaningful saving over the life of the policy.

---

How Eatons Hill Compares

Understanding where your suburb sits in the broader insurance landscape is key to making an informed decision. Here's how Eatons Hill's insurance costs stack up:

| Benchmark | Premium |

|---|---|

| This quote | $2,229/yr |

| Suburb average (Eatons Hill) | $2,298/yr |

| Suburb median (Eatons Hill) | $2,404/yr |

| Suburb 25th percentile | $1,414/yr |

| Suburb 75th percentile | $3,074/yr |

| LGA average (Moreton Bay) | $3,435/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

(Based on 42 quotes sampled for the Eatons Hill suburb.)

The contrast between Eatons Hill and the broader Queensland average is striking. The QLD state average of $9,129/yr is heavily skewed by high-risk areas — particularly cyclone-prone coastal and far-north Queensland regions, where premiums can be eye-watering. Eatons Hill, sitting in the Moreton Bay LGA in south-east Queensland, benefits enormously from not being classified as a cyclone risk area, which keeps premiums far more manageable.

Even compared to the national average of $5,347/yr, this quote looks competitive. The national median of $2,764/yr is a more useful comparison point, and at $2,229/yr, this quote comes in $535 below that figure — a solid result.

The suburb's 25th–75th percentile spread ($1,414–$3,074) tells us there's meaningful variation in what Eatons Hill homeowners pay. Those at the lower end likely have smaller homes, lower sums insured, or have actively shopped around. If your current premium sits above the 75th percentile, it's definitely worth getting a fresh comparison.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge. Here's how the key features play out:

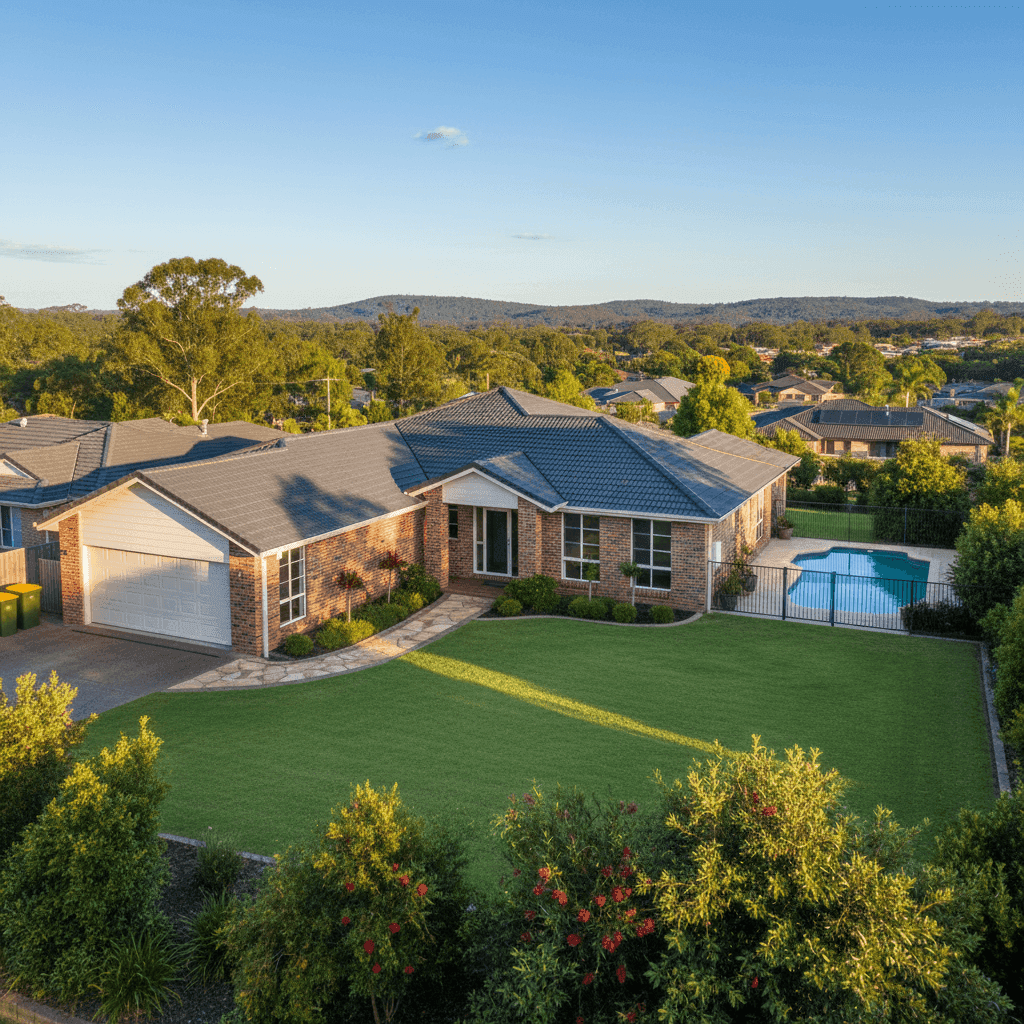

Brick Veneer Walls & Tiled Roof Brick veneer construction is generally viewed favourably by insurers. It's resistant to fire and termites, and holds up well in storms. Combined with a tiled roof — another durable, low-maintenance material — this property sits in a construction category that typically attracts lower risk loadings than, say, weatherboard or Colorbond alternatives.

Slab Foundation A concrete slab foundation is standard for homes of this era and is considered low-risk from an insurer's perspective. There are no subfloor spaces to worry about, reducing the likelihood of certain moisture and pest-related claims.

Built in 1997 At roughly 27 years old, this home is mature but not aged. Properties from the late 1990s generally have modern enough wiring and plumbing to avoid the risk surcharges sometimes applied to older homes, while also having the benefit of solid construction standards from that era.

Swimming Pool The presence of a pool adds a small degree of liability and maintenance risk, which can nudge premiums upward slightly. Pools also need to be factored into the building sum insured, as they form part of the permanent structure.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and contribute to the overall replacement cost of the home. Insurers factor in the cost of replacing these systems when assessing building cover, which can influence the recommended sum insured.

214 sqm Building Size At 214 square metres, this is a comfortably sized family home. The building sum insured of $808,000 translates to roughly $3,776/sqm — a reasonable figure for a brick veneer home in south-east Queensland when accounting for current construction costs, inclusions like the pool and ducted air conditioning, and site-specific factors.

---

Tips for Homeowners in Eatons Hill

1. Review your sum insured regularly Construction costs in south-east Queensland have risen significantly in recent years. If your building sum insured hasn't been updated to reflect current rebuild costs, you could be underinsured — meaning a major claim might not cover the full cost of rebuilding. Use a building cost calculator or speak to a quantity surveyor to verify your figure annually.

2. Bundle home and contents for potential savings This quote already combines home and contents cover, which is often the most cost-effective approach. If you're currently holding separate policies with different insurers, consolidating them could reduce your total premium and simplify your administration.

3. Compare quotes before each renewal Insurers don't always reward loyalty. Premiums can creep up at renewal without a corresponding increase in risk. With 42 quotes sampled in Eatons Hill, there's clearly a wide spread of pricing — shopping around each year is one of the most reliable ways to stay in the lower half of that range.

4. Check your excess settings Both excesses on this policy are set at $1,000. Opting for a higher excess (say, $2,000) can meaningfully reduce your annual premium if you're comfortable covering smaller claims out of pocket. Conversely, if cash flow is a concern, a lower excess may be worth the slightly higher premium.

---

Ready to Compare?

Whether you're renewing soon or just curious about what the market looks like, comparing quotes is always worthwhile. Get a home insurance quote at CoverClub to see how your current premium stacks up — it takes just a few minutes and could save you hundreds each year.