If you own a free standing home in Eschol Park, NSW 2558, you're likely no stranger to the annual ritual of reviewing your home insurance. Sitting within the Campbelltown local government area in Sydney's south-west, Eschol Park is a quiet, established suburb made up largely of brick homes on generous blocks. But when a home insurance quote lands in your inbox, it can be hard to know whether you're getting a fair deal — or paying over the odds. This article breaks down a recent home and contents insurance quote for a five-bedroom property in the area, benchmarks it against local, state and national data, and gives you practical tips to make sure you're not overpaying.

---

Is This Quote Fair?

The quote in question comes to $3,122 per year (or $299/month) for combined home and contents cover, with a building sum insured of $1,025,000 and contents valued at $247,000. Both the building and contents excess are set at $1,000.

Based on our analysis, this quote is rated Expensive — above average for the Eschol Park area.

To put that in perspective: the suburb average premium sits at just $1,439/year, and the median is even lower at $1,265/year. This quote is more than double the local median. Even at the 75th percentile — meaning 75% of comparable quotes in the suburb are cheaper — premiums only reach $1,731/year. So this quote sits well above what most Eschol Park homeowners are paying.

That said, context matters. This is a large, well-appointed home with a high building sum insured ($1,025,000) and a substantial contents value ($247,000). Features like ducted climate control and solar panels also add to the insurable value of the property. The elevated premium isn't necessarily unjustified — but it does signal that shopping around could yield meaningful savings.

---

How Eschol Park Compares

Understanding where Eschol Park sits in the broader insurance landscape helps frame whether your premium is reasonable. You can explore the full local breakdown on the Eschol Park suburb stats page.

| Benchmark | Premium |

|---|---|

| This quote | $3,122/yr |

| Eschol Park suburb average | $1,439/yr |

| Eschol Park suburb median | $1,265/yr |

| Campbelltown LGA average | $1,893/yr |

| NSW average | $9,528/yr |

| NSW median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

(Based on 33 quotes collected for the Eschol Park area.)

Interestingly, Eschol Park is a relatively affordable suburb to insure by both state and national standards. The NSW state average of $9,528/year is heavily skewed by high-risk coastal and flood-prone areas, while the national average of $5,347/year reflects the diversity of risk profiles across Australia — from cyclone-prone Queensland to bushfire-affected regions in Victoria and South Australia.

At $3,122/year, this quote is actually below both the NSW and national averages, which is reassuring. But compared to what neighbours in Eschol Park are typically paying, it's on the higher end — a gap largely explained by the property's size, high sum insured, and additional features.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the insurance premium. Here's how they stack up:

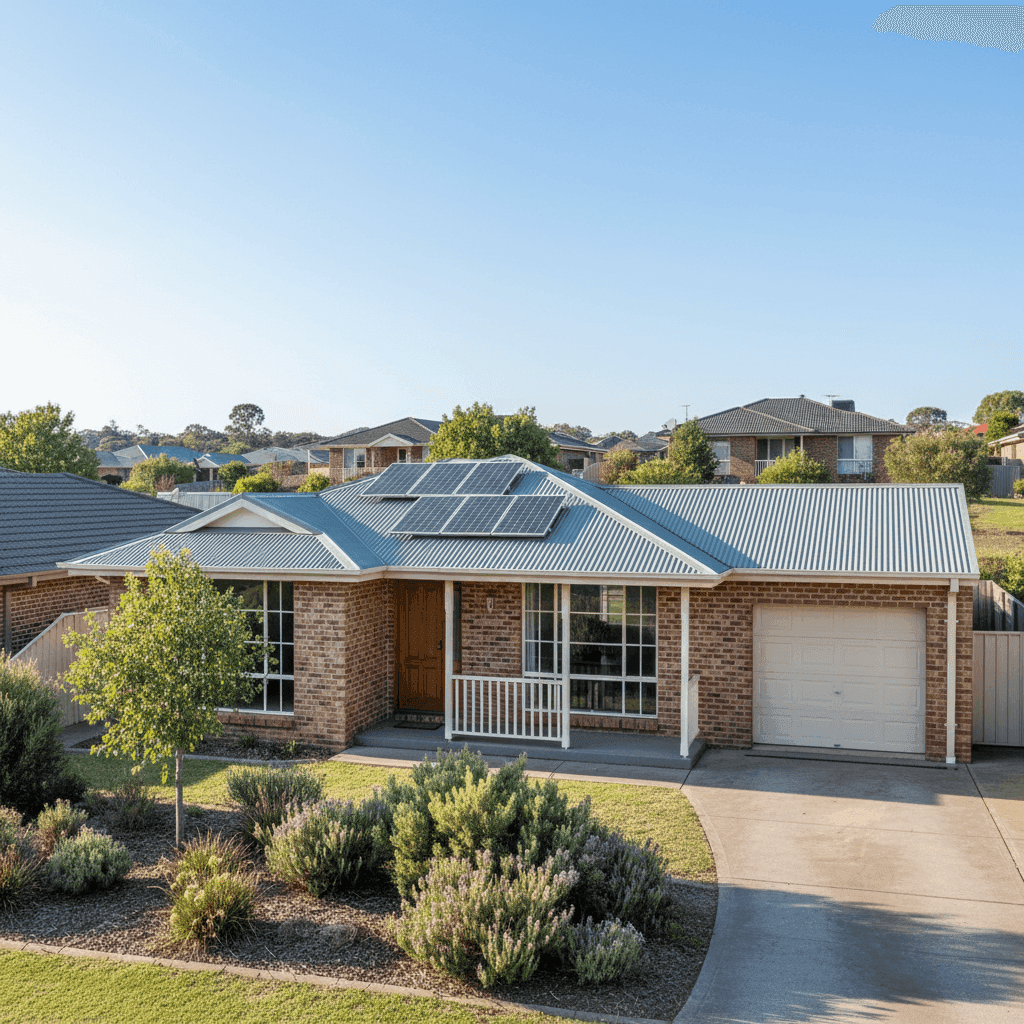

Size and sum insured At 325 sqm, this is a large home by any measure. A building sum insured of $1,025,000 reflects the cost to fully rebuild — not the market value — and for a five-bedroom brick home of this size, that figure is plausible. A higher sum insured means a higher premium, plain and simple.

Brick veneer construction Brick veneer walls are generally viewed favourably by insurers. They offer solid fire resistance and structural durability compared to timber or weatherboard alternatives, which can help moderate premiums.

Steel/Colorbond roof Colorbond roofing is a popular choice across Australian suburbs and is generally considered low-maintenance and resilient. Insurers typically regard it positively, as it holds up well in storms and doesn't carry the fire risk of older tile or timber roofing.

Concrete slab foundation A slab foundation is standard for homes built in the early 2000s and is generally considered stable and low-risk from an insurance perspective, particularly in areas not prone to significant soil movement.

Solar panels Solar panels add value to the property but also add to the insurable sum. Depending on the policy, panels may be covered under building insurance — and their replacement cost can be substantial. This is worth confirming with your insurer.

Ducted climate control Ducted air conditioning systems are expensive to repair or replace and are typically included in the building sum insured. Their presence in this property is a legitimate contributor to the higher premium.

No pool, no cyclone risk zone The absence of a swimming pool removes one common source of liability claims, and Eschol Park's location outside cyclone risk zones means the property avoids the significant premium loading that affects homes in northern Queensland and parts of WA.

---

Tips for Homeowners in Eschol Park

1. Review your building sum insured carefully A sum insured of $1,025,000 for a 325 sqm home works out to roughly $3,154/sqm — which is on the higher end for a standard-finish property. It's worth getting an independent building cost estimate to ensure you're not over-insured. While being underinsured is a serious risk, over-insuring means you're paying more than necessary.

2. Compare quotes from multiple insurers The gap between this quote and the Eschol Park suburb median is significant. Use a comparison platform like CoverClub to see what multiple insurers would charge for the same level of cover. Even modest savings of $500–$800/year add up over time.

3. Consider your excess settings Both the building and contents excess are set at $1,000. Opting for a higher excess — say $2,000 — can meaningfully reduce your annual premium. Just make sure you're comfortable covering that amount out of pocket in the event of a claim.

4. Confirm solar panel coverage With solar panels on the roof, it's essential to check how your policy treats them. Some insurers cover panels as part of the building; others require a separate endorsement. Make sure your policy documents are clear on this point so you're not caught short after a hailstorm or storm event.

---

Get a Better Deal on Home Insurance

Whether you're renewing your policy or comparing for the first time, it pays to shop around. The difference between the cheapest and most expensive quotes in Eschol Park can be hundreds of dollars a year — for equivalent levels of cover. Head to CoverClub to compare home and contents insurance quotes tailored to your property and see if you can do better than $3,122/year.