If you own a free standing home in Euleilah, QLD 4674, you're likely aware that finding the right building insurance at a fair price takes a bit of research. Euleilah is a small rural locality in the Bundaberg Region of Queensland — an area where insurance premiums can vary significantly depending on property characteristics, local risk factors, and the insurer's own pricing models. In this article, we analyse a recent building-only insurance quote for a 3-bedroom, 2-bathroom home in Euleilah and unpack what's driving the price — and whether it represents genuine value.

---

Is This Quote Fair?

The quote in question comes in at $2,218 per year (or $217/month) for building-only cover on a free standing home with a sum insured of $600,000 and a building excess of $2,000. Our price rating for this quote is CHEAP — below average — which is excellent news for the homeowner.

To put that in context: Queensland is one of the most expensive states in Australia for home insurance, largely due to the elevated risk of extreme weather events including flooding, storms, and hail. A below-average premium in this environment is a meaningful saving. The $2,000 building excess is on the higher side, which does contribute to the lower annual premium — but for homeowners who can absorb that upfront cost in the event of a claim, this trade-off often makes financial sense.

Overall, this quote represents strong value for a Queensland property, and is well worth benchmarking against other insurers to ensure it remains competitive at renewal time.

---

How Euleilah Compares

Let's look at how this premium stacks up against the broader market. While there isn't enough localised data to provide a suburb-level average for Euleilah specifically, we can draw meaningful comparisons at the LGA, state, and national level. You can explore the latest figures on the Euleilah suburb stats page as more data becomes available.

| Benchmark | Average Premium |

|---|---|

| This Quote | $2,218/yr |

| Bundaberg LGA Average | $3,464/yr |

| QLD State Average | $4,547/yr |

| QLD State Median | $3,931/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

The numbers tell a compelling story. This quote sits:

- $1,246 below the Bundaberg LGA average

- $2,329 below the Queensland state average

- $747 below the national average

- $498 below the national median

Queensland premiums are consistently the highest in the country — the QLD state average of $4,547/yr is more than 53% above the national average of $2,965/yr. Against that backdrop, securing a premium under $2,300 for a $600,000 sum insured is a genuinely strong outcome. Homeowners in the Bundaberg Region should take note: not all properties in this LGA will attract this level of pricing, and the specifics of your home matter enormously.

---

Property Features That Affect Your Premium

Several characteristics of this particular property are likely contributing to its favourable premium. Here's what stands out:

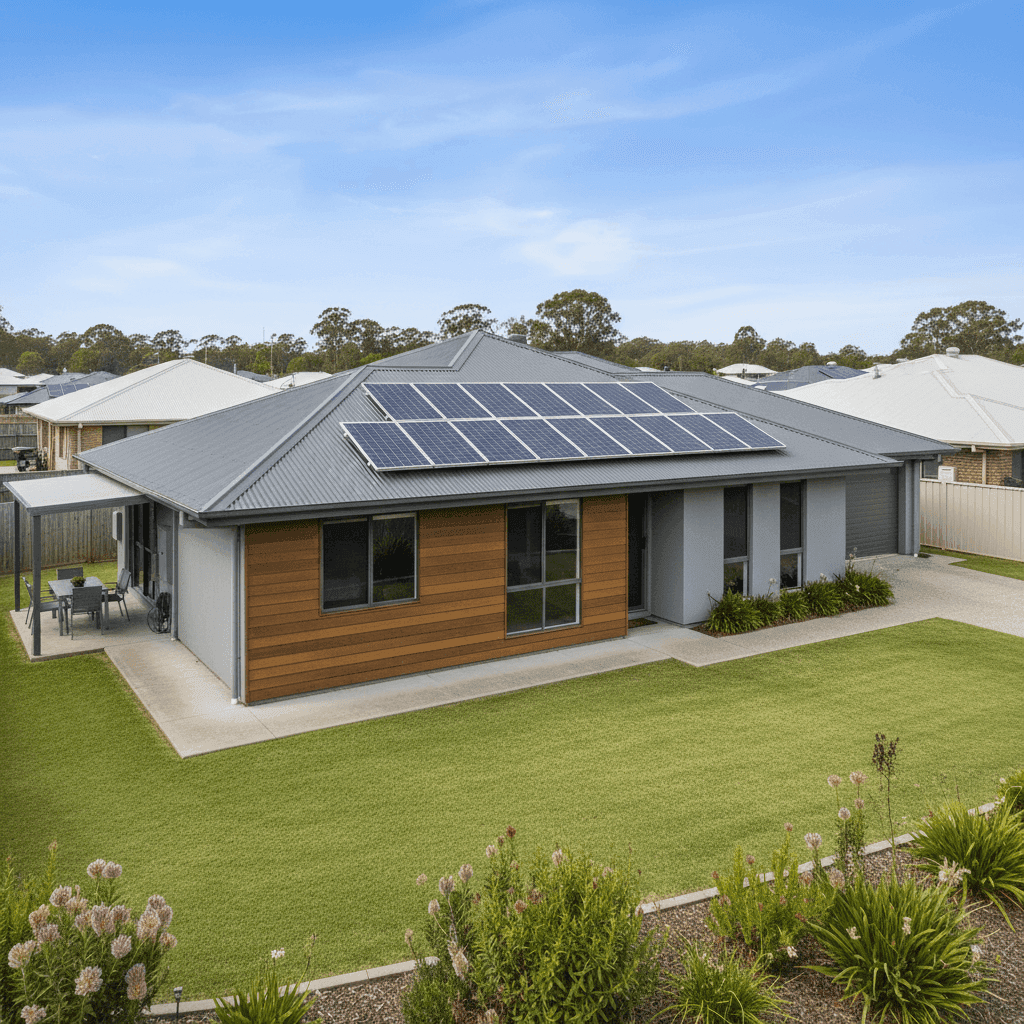

Steel/Colorbond Roof

Colorbond roofing is widely regarded by insurers as a lower-risk roofing material compared to older tile or fibro alternatives. It's durable, resistant to corrosion, and performs well in high-wind and storm conditions — all factors that reduce the likelihood of a claim.

Slab Foundation

A concrete slab foundation is generally considered low-risk from an insurance perspective. It offers structural stability and is less susceptible to certain types of subsidence or pest-related damage compared to raised timber stumps or piers.

1995 Construction Year

At around 30 years old, this home is relatively modern in the context of Queensland's housing stock. Homes built from the mid-1990s onward typically comply with more rigorous building codes, which can positively influence premium pricing.

Solar Panels

The presence of solar panels adds to the overall replacement value of the property and is factored into the sum insured. Insurers treat solar panels differently — some include them automatically under building cover, while others may require a specific endorsement. It's worth confirming with your insurer exactly how solar panels are covered under your policy.

No Cyclone Risk

Euleilah is not classified as a cyclone risk area, which is a significant factor in keeping premiums down. Properties in northern Queensland or coastal cyclone zones can attract substantial loading on their premiums. Being outside this zone is a meaningful advantage.

Vinyl Flooring and Standard Fittings

Vinyl flooring and standard-quality fittings are practical choices that keep replacement costs — and therefore the sum insured — at a manageable level. High-end finishes such as marble benchtops or custom joinery can push up rebuild costs considerably.

---

Tips for Homeowners in Euleilah

Even with a competitive quote in hand, there are always steps you can take to protect your home and potentially reduce your premium further.

1. Review your sum insured annually Construction costs have risen sharply across Queensland in recent years. A $600,000 sum insured may be appropriate today, but it's worth reassessing each year to ensure it accurately reflects the cost to rebuild your home from scratch — not its market value. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Consider your excess carefully This policy carries a $2,000 building excess. A higher excess typically lowers your annual premium, but make sure you have that amount readily accessible in the event of a claim. If cash flow is a concern, it may be worth comparing quotes with a lower excess to find the right balance.

3. Confirm solar panel coverage With solar panels on the roof, take a moment to read your policy wording carefully. Check whether your panels are covered for accidental damage, storm damage, and electrical faults — and whether there's a separate sub-limit that applies. If in doubt, ask your insurer directly.

4. Compare at renewal time Insurance loyalty rarely pays. Insurers frequently offer their best rates to new customers, meaning your premium can creep up at renewal without a corresponding increase in risk. Set a reminder to compare quotes at least 30 days before your policy renews — it takes only a few minutes and can save hundreds of dollars.

---

Ready to Compare Home Insurance in Euleilah?

Whether you're assessing your current policy or shopping for the first time, CoverClub makes it easy to see how your quote stacks up. Get a home insurance quote today and find out if you're paying a fair price for your property in Euleilah. With real data from thousands of Australian properties, you'll be able to compare with confidence.