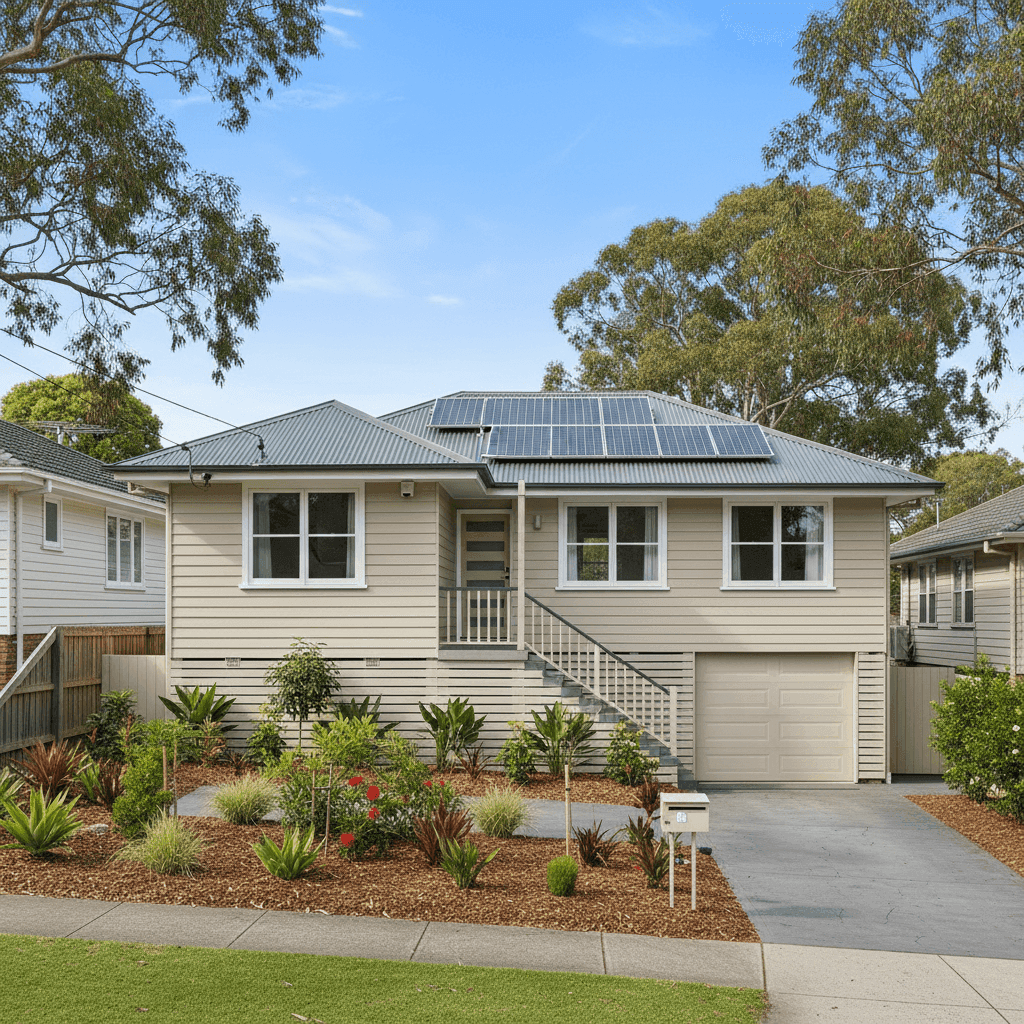

Everton Park is a well-established suburb in Brisbane's north-west, known for its leafy streets, post-war character homes, and strong community feel. If you own a free standing home here — particularly one of the many weatherboard properties built in the 1950s — understanding what you should be paying for home and contents insurance is an important part of protecting one of your biggest assets. This article breaks down a real quote for a 4-bedroom, 2-bathroom home in Everton Park (postcode 4053) and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question covers both building and contents for a 4-bedroom weatherboard home, with a building sum insured of $651,000 and contents valued at $100,000. The annual premium comes in at $1,485 per year (or around $155 per month).

Our price rating for this quote is CHEAP — below average for the suburb. That's a meaningful distinction. Based on 23 quotes collected for Everton Park, the suburb average sits at $2,567 per year and the median at $2,535. This quote lands well below the 25th percentile of $1,931 — meaning it's cheaper than at least 75% of comparable quotes in the area.

In practical terms, a homeowner securing this premium is saving roughly $1,082 per year compared to the suburb average. Over five years, that's more than $5,000 in savings — money that could go toward upgrades, an emergency fund, or simply staying ahead of rising living costs.

That said, it's worth noting the building excess is $4,000 — which is on the higher side. A lower excess typically results in a higher premium, so part of the reason this quote is so competitive may be that the policyholder has accepted more out-of-pocket cost in the event of a claim. The contents excess is a more standard $1,000.

---

How Everton Park Compares

To truly appreciate this quote, it helps to zoom out and look at the broader pricing landscape.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,485 |

| Everton Park Suburb Average | $2,567 |

| Everton Park Suburb Median | $2,535 |

| Everton Park 25th Percentile | $1,931 |

| Moreton Bay LGA Average | $3,435 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

The Queensland state average of $9,129 is dramatically higher than what Everton Park homeowners typically pay. This is largely driven by high-risk areas in Far North Queensland — cyclone-prone regions like Cairns and Townsville — which pull the state average up significantly. The state median of $3,903 is a more representative figure for most Queenslanders, and even that is nearly three times the cost of this particular quote.

Compared to the national average of $5,347, this quote represents exceptional value. Even the national median of $2,764 is nearly double what's been quoted here. Everton Park, sitting in Brisbane's suburban middle ring, benefits from relatively low natural hazard risk compared to coastal or flood-prone areas — and that's clearly reflected in local premiums.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers assess and price the risk.

Weatherboard timber construction is one of the most significant factors. Older weatherboard homes — especially those built around 1952 — are more susceptible to fire, termite damage, and general wear compared to brick veneer or double-brick construction. Insurers typically apply a loading to these properties, though the degree varies between providers.

The Colorbond steel roof is a positive from an insurance perspective. Steel roofing is durable, low-maintenance, and performs well in storms compared to terracotta or concrete tiles, which can crack or dislodge. This may help moderate the premium despite the timber walls.

Solar panels are present on this property. While they add value and sustainability, they can slightly increase the cost to rebuild or repair a roof following storm or hail damage, and some insurers factor this into their pricing. It's worth confirming with your insurer that the panels are covered under the building policy and understanding any sub-limits that may apply.

A concrete slab foundation is generally viewed favourably by insurers, as it's more resistant to subsidence and moisture-related issues compared to older stumped or suspended timber floors.

Timber and laminate flooring throughout the home adds to the replacement value of contents and internal finishes — which is reflected in the $651,000 building sum insured and $100,000 contents cover.

The absence of a pool and ducted air conditioning keeps the insurable risk (and replacement cost) lower than comparable properties with those features, which likely contributes to the competitive premium.

---

Tips for Homeowners in Everton Park

1. Review your sum insured annually Construction costs in South-East Queensland have risen sharply in recent years. A building sum insured that was adequate two years ago may no longer cover a full rebuild. Use a building cost calculator or speak with a local builder to make sure your $651,000 cover still reflects current replacement costs — especially for a weatherboard home with timber flooring and period features.

2. Understand your excess before you claim A $4,000 building excess is manageable for major events like storm damage or fire, but it makes small claims uneconomical. Factor this into your emergency fund planning. If cash flow is tight, it may be worth comparing quotes with a lower excess to find a balance that suits your situation.

3. Confirm solar panel coverage Ask your insurer specifically how your solar panels are covered. Some policies include them automatically as part of the building; others treat them as optional extras or apply sub-limits. Given the cost of replacing a modern solar system, this is a detail worth clarifying in writing.

4. Keep records of your contents With $100,000 in contents cover, it's important to have an up-to-date home inventory. Take photos or video of valuable items, keep receipts where possible, and store copies securely off-site or in the cloud. This makes the claims process significantly smoother if the worst happens.

---

Compare Your Options with CoverClub

Whether you're renewing your existing policy or shopping around for the first time, it pays to see what's available in the market. Get a quote through CoverClub to compare home and contents insurance options for your Everton Park property — and find out if you're getting a deal as good as this one. You can also explore detailed suburb-level insurance data for Everton Park to benchmark your own premium.